Ceic data talk

•

0 likes•225 views

#CEIC #Indonesia Data Talk - Households Wary of Further Debts - Read more: http://bit.ly/1TQ53Ou

Recommended

More Related Content

Similar to Ceic data talk

Similar to Ceic data talk (20)

Recently uploaded

Recently uploaded (20)

Ceic data talk

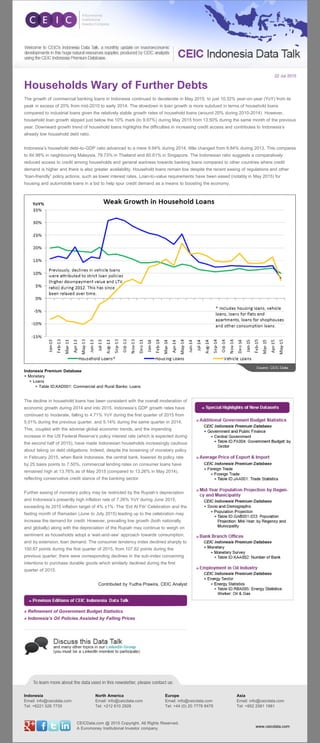

- 1. 22 Jul 2015 Households Wary of Further Debts The growth of commercial banking loans in Indonesia continued to decelerate in May 2015, to just 10.32% year-on-year (YoY) from its peak in excess of 20% from mid-2010 to early 2014. The slowdown in loan growth is more subdued in terms of household loans compared to industrial loans given the relatively stable growth rates of household loans (around 20% during 2010-2014). However, household loan growth slipped just below the 10% mark (to 9.97%) during May 2015 from 13.50% during the same month of the previous year. Downward growth trend of household loans highlights the difficulties in increasing credit access and contributes to Indonesia’s already low household debt ratio. Indonesia’s household debt-to-GDP ratio advanced to a mere 9.94% during 2014, little changed from 9.84% during 2013. This compares to 84.98% in neighbouring Malaysia, 79.73% in Thailand and 60.61% in Singapore. The Indonesian ratio suggests a comparatively reduced access to credit among households and general wariness towards banking loans compared to other countries where credit demand is higher and there is also greater availability. Household loans remain low despite the recent easing of regulations and other “loan-friendly” policy actions, such as lower interest rates. Loan-to-value requirements have been eased (notably in May 2015) for housing and automobile loans in a bid to help spur credit demand as a means to boosting the economy. Indonesia Premium Database + Monetary + Loans + Table ID.KAD001: Commercial and Rural Banks: Loans The decline in household loans has been consistent with the overall moderation of economic growth during 2014 and into 2015. Indonesia’s GDP growth rates have continued to moderate, falling to 4.71% YoY during the first quarter of 2015 from 5.01% during the previous quarter, and 5.14% during the same quarter in 2014. This, coupled with the adverse global economic trends, and the impending increase in the US Federal Reserve’s policy interest rate (which is expected during the second half of 2015), have made Indonesian households increasingly cautious about taking on debt obligations. Indeed, despite the loosening of monetary policy in February 2015, when Bank Indonesia, the central bank, lowered its policy rate by 25 basis points to 7.50%, commercial lending rates on consumer loans have remained high at 13.76% as of May 2015 (compared to 13.26% in May 2014), reflecting conservative credit stance of the banking sector. Further easing of monetary policy may be restricted by the Rupiah’s depreciation and Indonesia’s presently high inflation rate of 7.26% YoY during June 2015, exceeding its 2015 inflation target of 4% ±1%. The ‘Eid Al Fitr’ Celebration and the fasting month of Ramadan (June to July 2015) leading up to the celebration may increase the demand for credit. However, prevailing low growth (both nationally and globally) along with the depreciation of the Rupiah may continue to weigh on sentiment as households adopt a ‘wait-and-see’ approach towards consumption, and by extension, loan demand. The consumer tendency index declined sharply to 100.87 points during the first quarter of 2015, from 107.62 points during the previous quarter; there were corresponding declines in the sub-index concerning intentions to purchase durable goods which similarly declined during the first quarter of 2015. Contributed by Yudha Prawira, CEIC Analyst » Refinement of Government Budget Statistics » Indonesia’s Oil Policies Assisted by Falling Prices Indonesia Email: info@ceicdata.com Tel: +6221 526 7735 North America Email: info@ceicdata.com Tel: +212 610 2928 Europe Email: info@ceicdata.com Tel: +44 (0) 20 7779 8479 Asia Email: info@ceicdata.com Tel: +852 2581 1981 CEICData.com @ 2015 Copyright. All Rights Reserved. A Euromoney Institutional Investor company. www.ceicdata.com