1) Barclays admitted to rigging the LIBOR rate from 2005-2009 by submitting false rates that were inflated or deflated to benefit trading positions or project an image of financial strength.

2) Traders at Barclays regularly requested specific LIBOR submissions from the individuals responsible for submitting rates to benefit their trading positions.

3) This rate-rigging involved multiple currencies and desks at Barclays and occurred on a daily basis for several years before being uncovered.

![any means –– electronic, mechanical, photocopying, recording,

or otherwise –– without the permission of the

Stanford Graduate School of Business. Every effort has been

made to respect copyright and to contact copyright

holders as appropriate. If you are a copyright holder and have

concerns, please contact the Case Writing Office at

[email protected] or write to Case Writing Office, Stanford

Graduate School of Business, Knight Management

Center, 655 Knight Way, Stanford University, Stanford, CA

94305-5015.

BARCLAYS AND THE LIBOR:

ANATOMY OF A SCANDAL

Culture is difficult to define, I think it's even more difficult to

mandate—but for me the evidence of

culture is how people behave when no one is watching.

1

-Bob Diamond, (former) Barclays CEO

INTRODUCTION](https://image.slidesharecdn.com/caseeth-03date110713shei-220922045802-a6def14e/85/CASE-ETH-03-DATE-110713-Shei-2-320.jpg)

![4

1

“Today Business Lecture” delivered in 2011, quoted in Fixing

LIBOR: some preliminary findings, Paragraph 111,

http://www.publications.parliament.uk/pa/cm201213/cmselect/c

mtreasy/481/48103.htm (September 19, 2013)

2

In 2012, the number of banks on the Libor Panel was increased

to 18.

3

House of Commons Treasury Committee, Fixing LIBOR: some

preliminary findings, Paragraph 7

http://www.publications.parliament.uk/pa/cm201213/cmselect/c

mtreasy/481/48103.htm (September 19, 2013).

4

This included a $200 million civil penalty levied by the U.S.

Commodity Futures Trading Commission; a $160

million penalty from the U.S. Department of Justice; and a

£59.5 million fine by the U.K. Financial Services

For the exclusive use of R. Ahmed, 2022.

This document is authorized for use only by Rashik Ahmed in

FIN 9858 Summer 2022 taught by RHONDA HALPERN, CUNY

- Baruch College from Jun 2022 to Jul 2022.

mailto:[email protected]

http://www.publications.parliament.uk/pa/cm201213/cmselect/c

mtreasy/481/48103.htm](https://image.slidesharecdn.com/caseeth-03date110713shei-220922045802-a6def14e/85/CASE-ETH-03-DATE-110713-Shei-4-320.jpg)

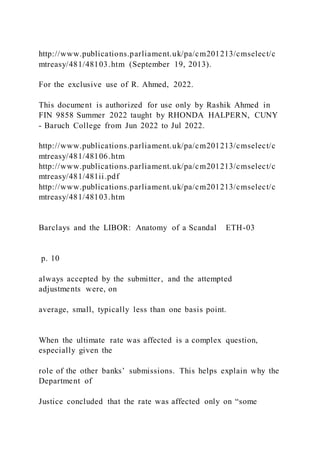

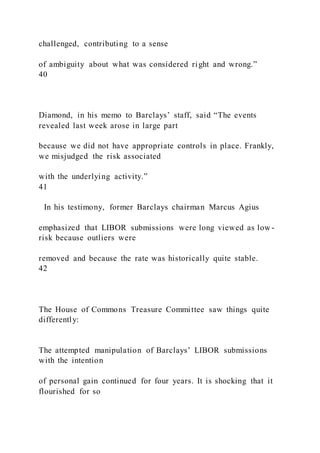

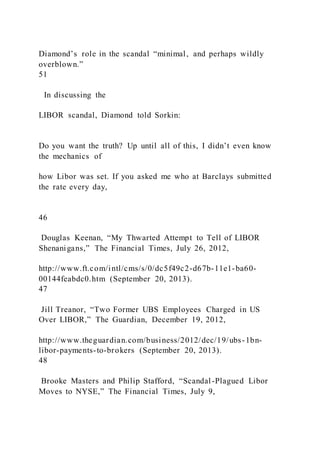

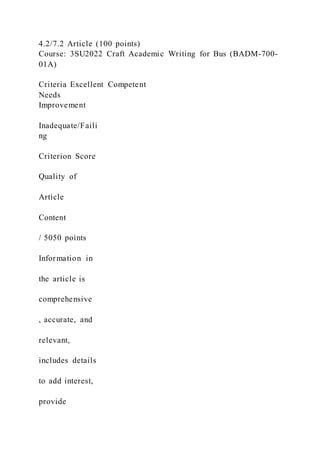

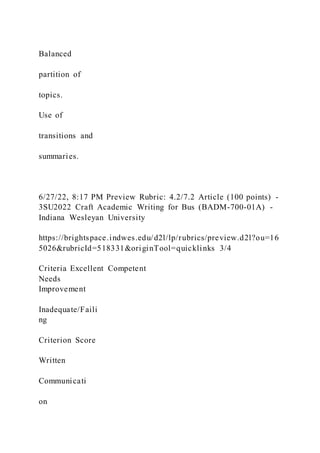

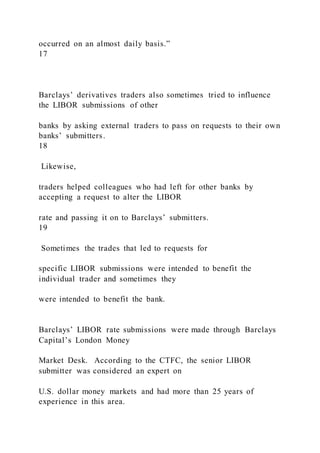

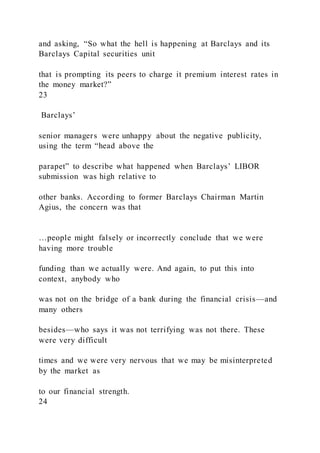

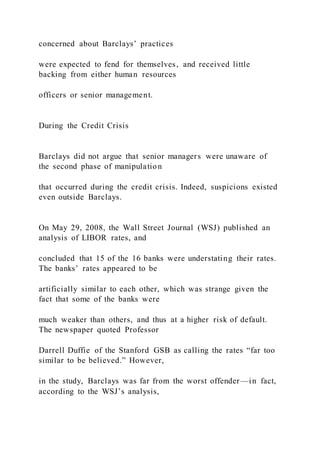

![exchange took place

between a trader and submitter:

22

Trader C: “The big day [has] arrived… My NYK are screaming

at me about an

unchanged 3m libor. As always, any help wd be greatly

appreciated. What do you

think you’ll go for 3m?

Submitter: “I am going 90 altho 91 is what I should be posting”.

Trader C: “[…] when I retire and write a book about this

business your name will

be written in golden letters […]”.

Submitter: “I would prefer this [to] not be in any book!”

The Second Phase: Appearing Strong During the Crisis

20

House of Commons Treasury Committee, Fixing LIBOR: some

preliminary findings, Section 32

http://www.publications.parliament.uk/pa/cm201213/cmselect/c

mtreasy/481/48103.htm (September 19, 2013).](https://image.slidesharecdn.com/caseeth-03date110713shei-220922045802-a6def14e/85/CASE-ETH-03-DATE-110713-Shei-21-320.jpg)

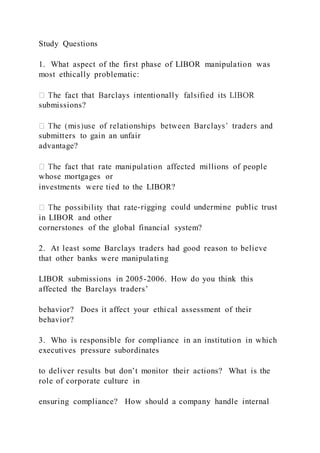

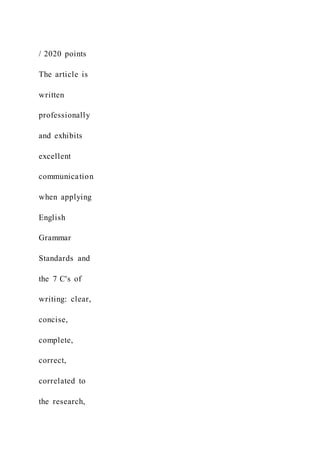

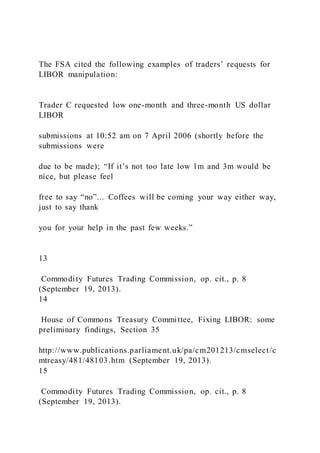

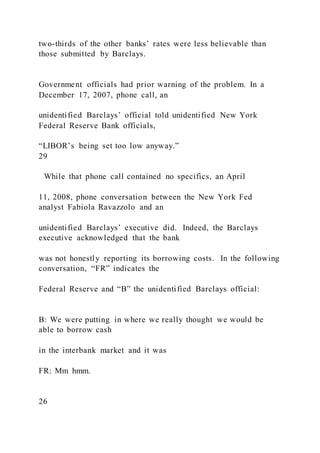

![For the exclusive use of R. Ahmed, 2022.

This document is authorized for use only by Rashik Ahmed in

FIN 9858 Summer 2022 taught by RHONDA HALPERN, CUNY

- Baruch College from Jun 2022 to Jul 2022.

http://www.newyorkfed.org/newsevents/news/markets/2012/libo

r/April_11_2008_transcript.pdf

http://www.publications.parliament.uk/pa/cm201213/cmselect/c

mtreasy/481/48103.htm

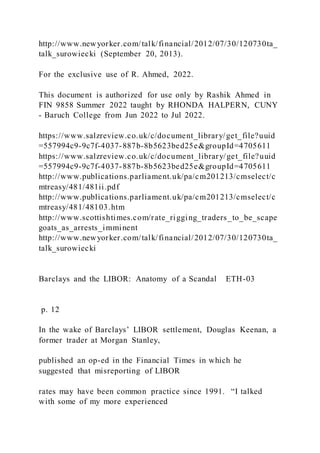

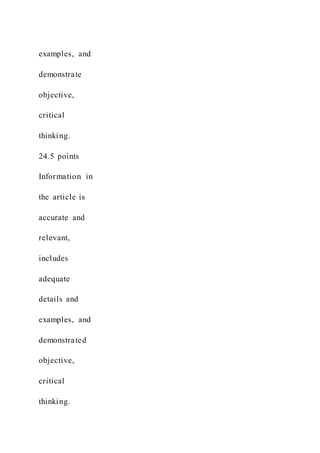

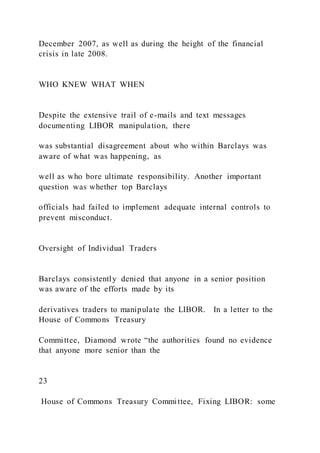

Barclays and the LIBOR: Anatomy of a Scandal ETH-03

p. 9

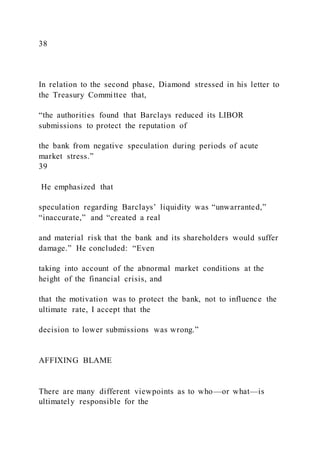

Further to our last call, Mr. Tucker reiterated that he had

received calls from a

number of senior figures within Whitehall [i.e., the government]

to question why

Barclays was always toward the top end of the Libor pricing… I

asked if he could

relay the reality, that not all banks were providing quotes at the

levels that

represented real transactions, his response “oh, that would be

worse…”

Mr. Tucker stated the level of calls he was receiving from

Whitehall were ‘senior’](https://image.slidesharecdn.com/caseeth-03date110713shei-220922045802-a6def14e/85/CASE-ETH-03-DATE-110713-Shei-35-320.jpg)