Download to read offline

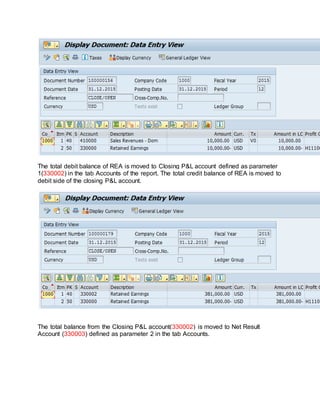

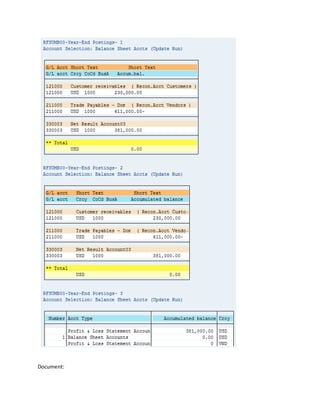

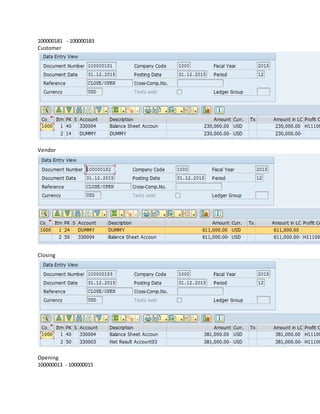

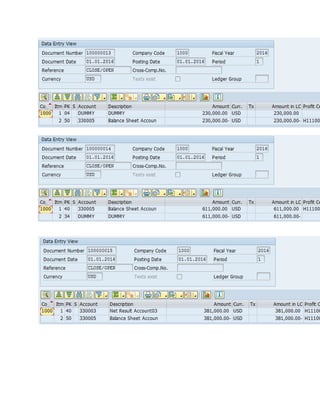

Closing balances of revenue and expense accounts are moved to a retained earnings account during the fiscal year-end closing process. The debit and credit balances of the retained earnings account are then moved to a closing profit and loss account. Finally, the balance of the closing profit and loss account is transferred to a net result account to zero it out for the new fiscal year.