Downloaded 40 times

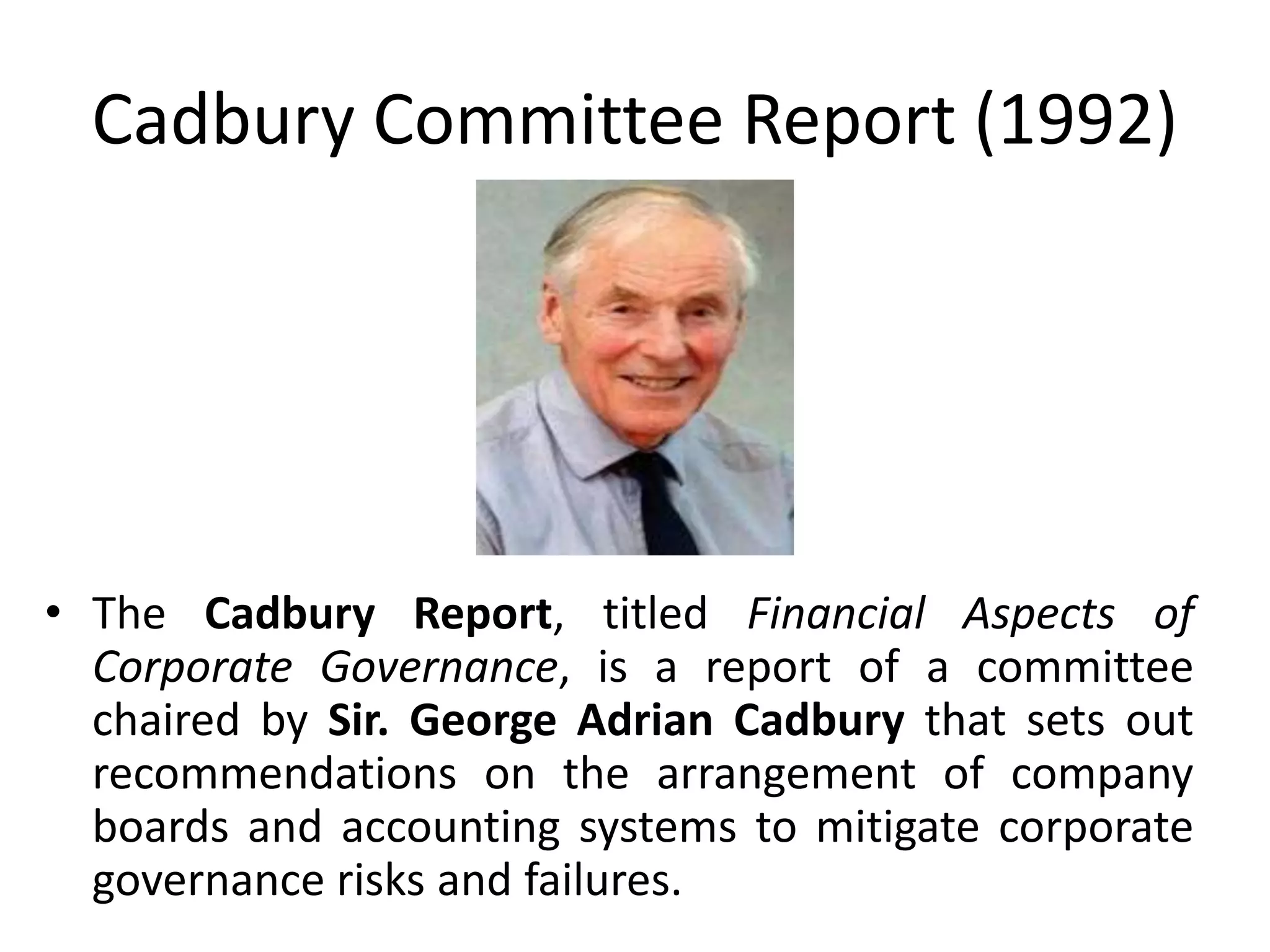

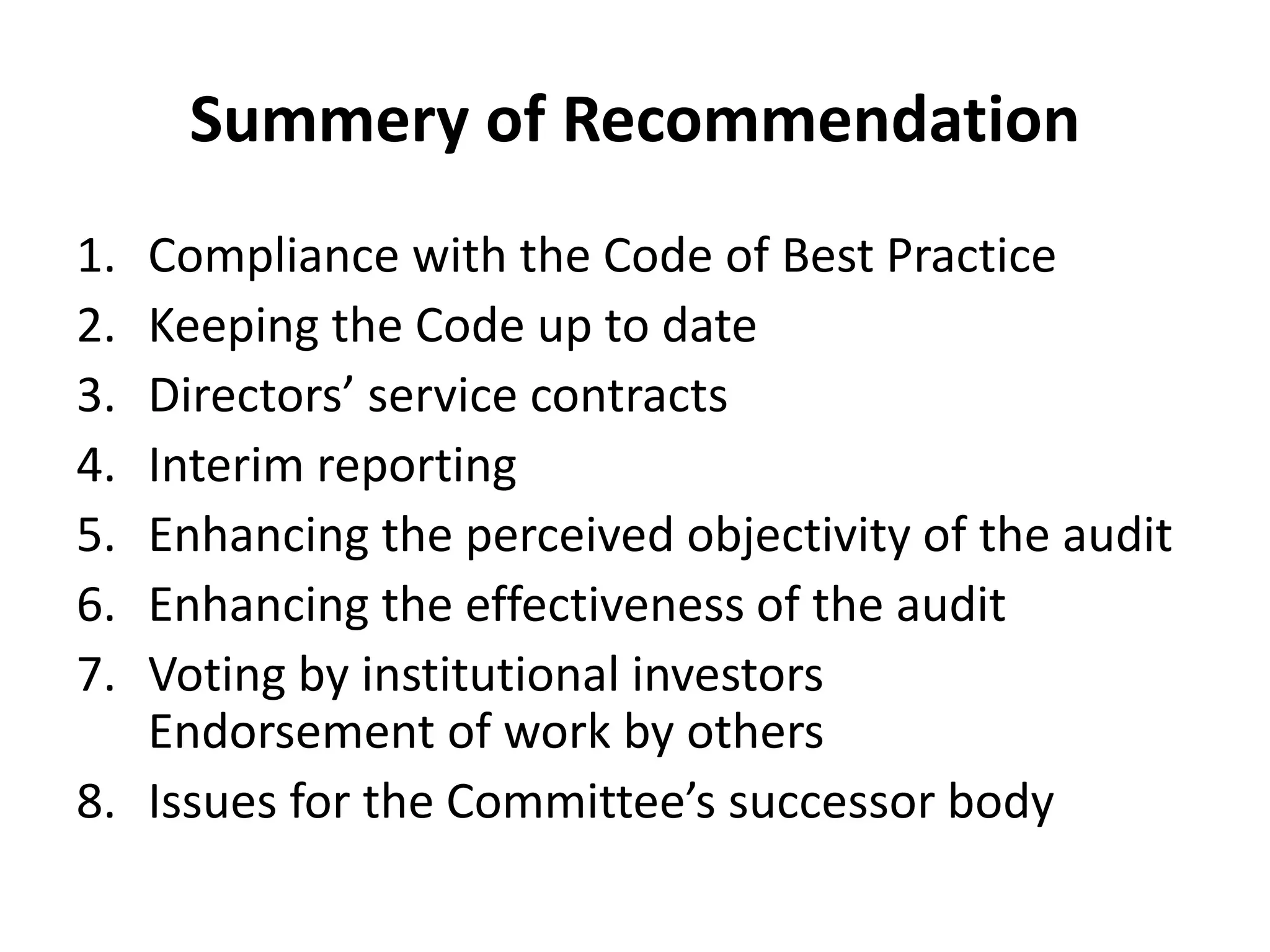

The document summarizes the key recommendations from the Cadbury Committee Report on corporate governance. It recommends that companies establish codes of best practice and standards of conduct. It emphasizes the roles and responsibilities of boards of directors, non-executive directors, executive directors, audit committees, and shareholders. It aims to strengthen accountability, transparency and integrity in financial reporting.