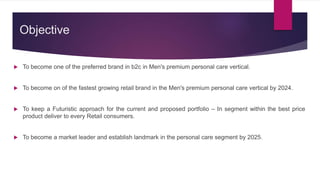

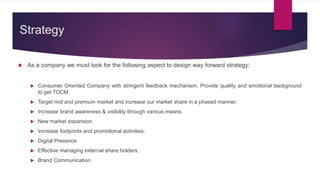

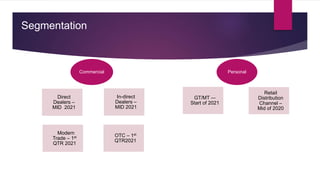

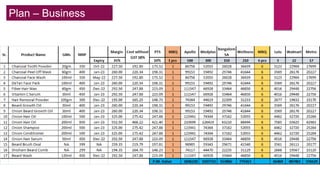

The document discusses strategies for a men's personal care brand to become a preferred and fast-growing brand in its category by 2024. It aims to have a futuristic product portfolio at competitive prices. Key strategies include becoming a consumer-oriented company, targeting mid to premium markets, increasing brand awareness, expanding into new markets, boosting footprints and promotions, strengthening digital presence, and effective communications. The brand looks to enter modern trade, OTC, and commercial channels in the first quarter of 2021 while onboarding indirect and direct dealers in mid-2021.

![[Team3] brand And 0marketing](https://cdn.slidesharecdn.com/ss_thumbnails/team3brandnmarketing1-181010030327-thumbnail.jpg?width=640&height=640&fit=bounds)