Download as PDF, PPTX

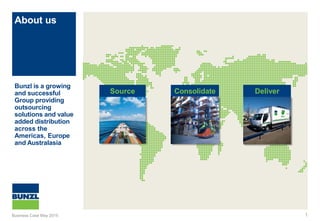

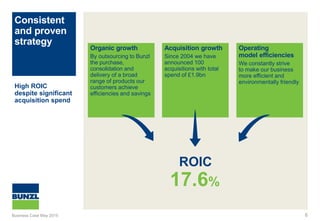

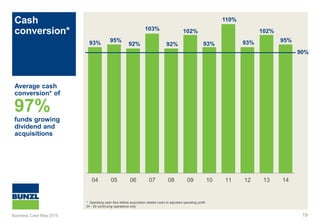

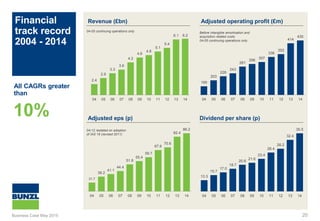

Bunzl is a business-to-business distribution company that provides outsourced procurement and logistics services across Europe, North America, and Australasia. It distributes a wide range of consumable products to various end markets such as foodservice, grocery, cleaning/hygiene, retail, safety, and healthcare. Bunzl has a decentralized operating model, sources products globally at low costs, and pursues acquisitions for geographic and market expansion. Over the past decade, the company has grown organically and through acquisitions, achieving average annual revenue and profit growth of over 10% and consistently strong cash conversion and returns on capital.