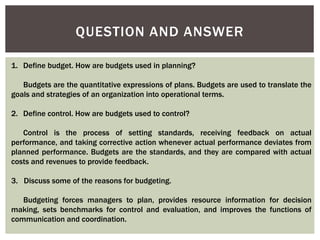

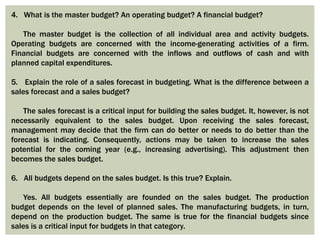

This document summarizes key points from a lecture on budgeting for planning and control. It addresses common questions about budgets, including definitions of different types of budgets like master budgets, operating budgets, and financial budgets. It discusses how budgets are used for planning by translating goals into quantitative plans, and for control by setting standards and providing feedback. Specific topics covered include the roles of sales forecasts and budgets, how budgets in different areas depend on the sales budget, and factors to consider when individual managers in charge of areas like sales or production are perceived to have optimistic or pessimistic tendencies. The document also contrasts traditional static master budgets with more flexible and activity-based budgets.