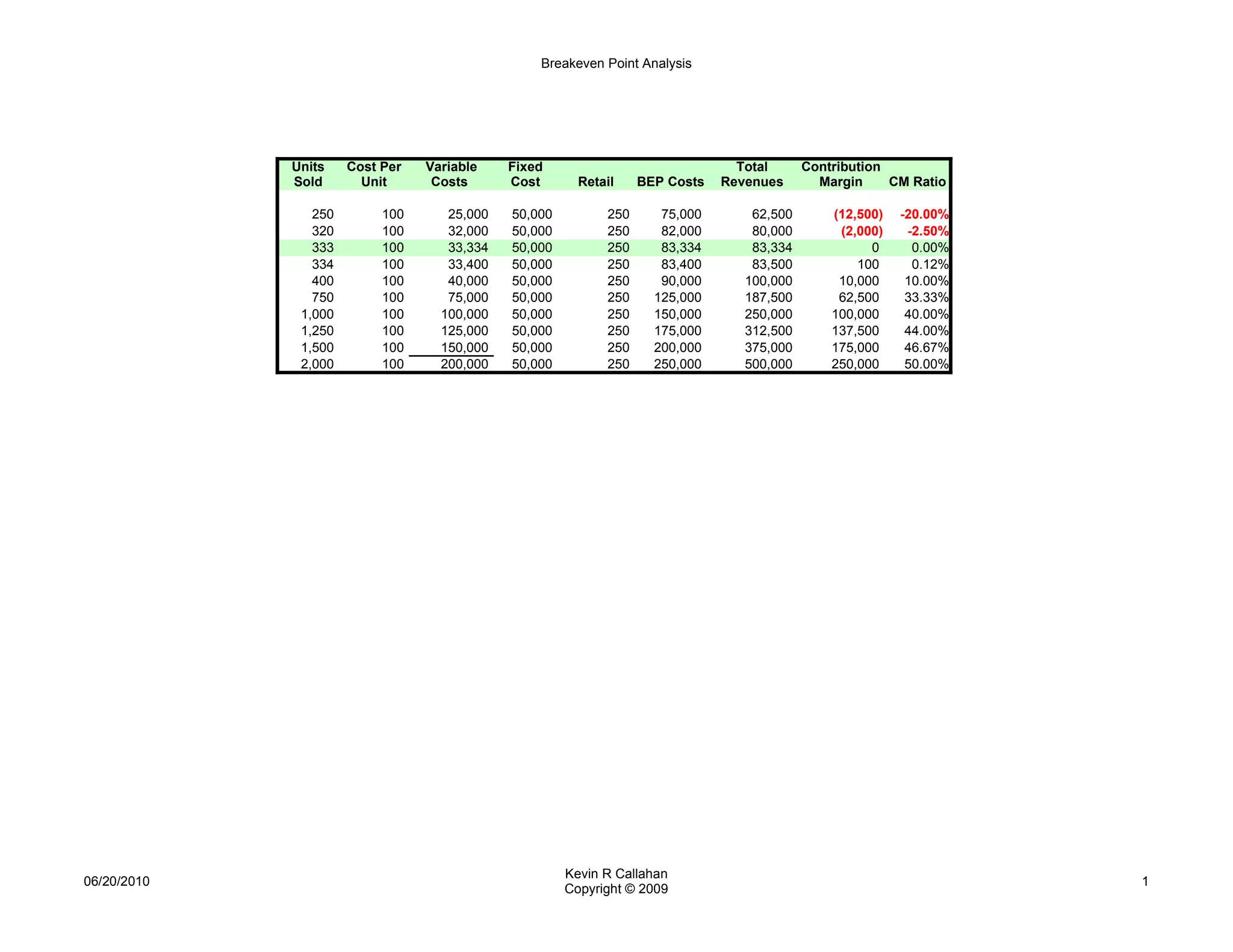

This document presents a breakeven point analysis showing the units sold, costs, revenues, and contribution margin at different production levels. The breakeven point is reached at 333 units, where total revenues equal total costs. Above this point, the company begins to cover its fixed costs and make a profit.