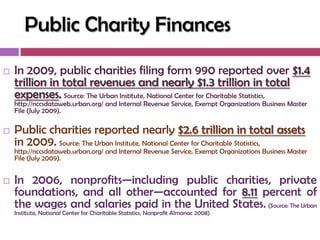

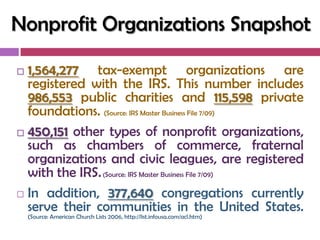

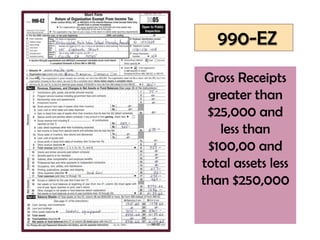

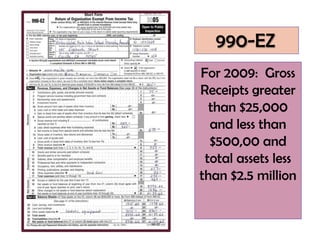

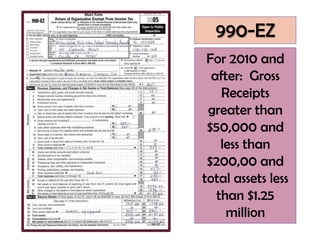

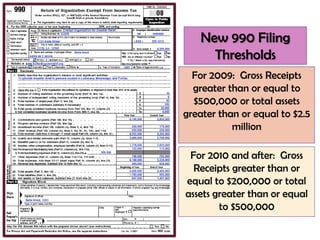

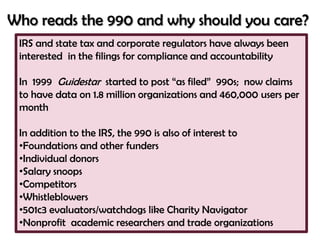

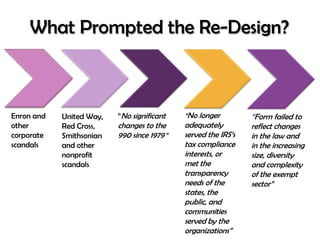

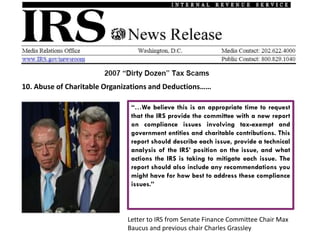

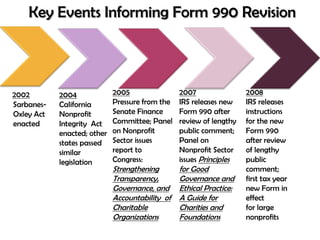

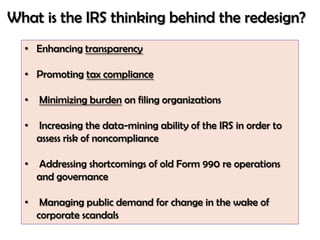

The document provides an overview of nonprofit board governance and regulations. It discusses trends in the nonprofit sector including increasing expectations for transparency and accountability. It also summarizes key nonprofit finance statistics and outlines reporting requirements for tax-exempt organizations to the IRS including thresholds for Form 990, 990-EZ, and 990-N filing. The IRS redesigned Form 990 in 2008 to better reflect the size and complexity of the nonprofit sector and enhance transparency for regulators and the public.