Downloaded 28 times

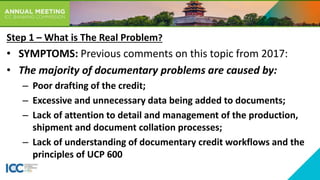

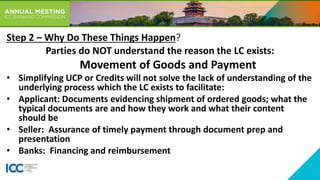

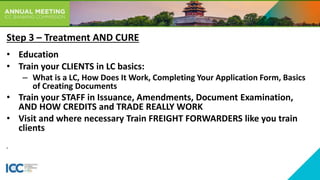

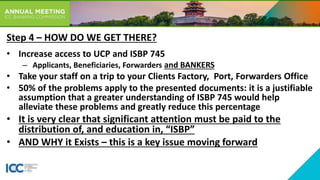

The document discusses the challenges and controversies surrounding documentary credit practices, highlighting issues such as poor document drafting, excessive data, and a lack of understanding of credit workflows. It emphasizes the need for better education and training for clients and staff to improve the handling of letters of credit (LC). Proposed solutions include increasing access to the UCP and ISBP 745, as well as improving communication and training among all parties involved in the documentary credit process.