Download to read offline

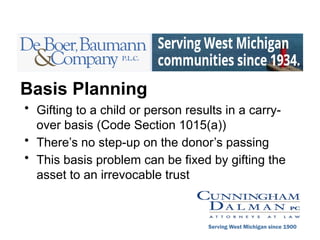

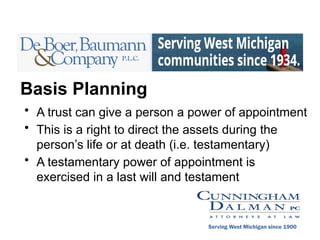

This presentation discusses gift planning with irrevocable trusts and how the trusts can be structured so the assets still get a step-up in basis. The trusts grant a power of appointment and allow for this step-up on the power holder's passing.

![A New Product Line Irs Supermarket[1]](https://cdn.slidesharecdn.com/ss_thumbnails/anewproductlineirssupermarket1-100310144627-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)