Download as PDF, PPTX

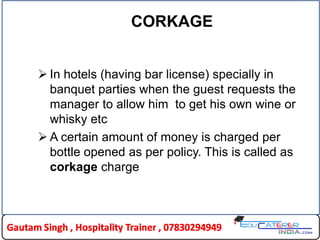

The document outlines various aspects of bar planning, including design, layout, equipment, and licensing regulations. It discusses the setup of front, back, and under bar areas, detailing their functions and essential items needed for effective operations. Additionally, the document touches on beverage costs, pricing methods, and corkage charges for customer-supplied drinks.