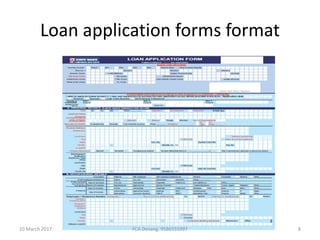

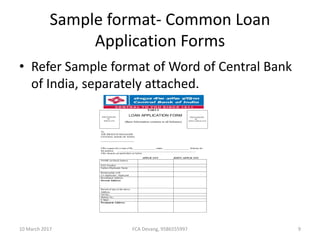

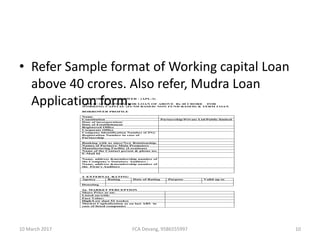

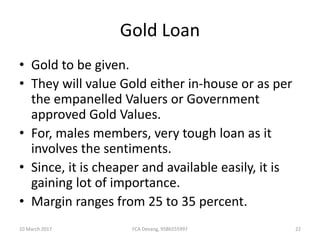

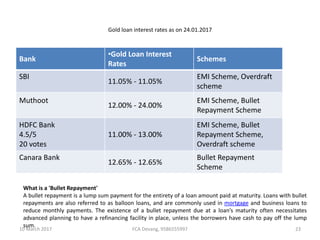

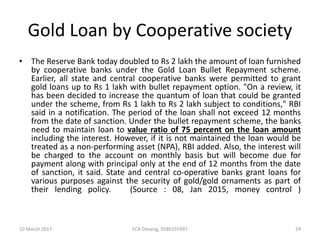

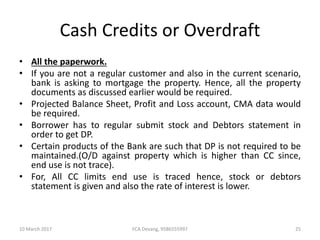

This document provides an overview of the documentation required by banks for different types of loans. It begins with an introduction to the loan process and then discusses the basic documents required for all loan types, such as the loan application form, KYC documents, and CIBIL report. It then examines specific additional documents needed for various loan categories, such as housing loans, gold loans, cash credit/overdraft facilities, and car loans. Examples of loan application formats and a sample CIBIL report are also included for reference. The document aims to educate borrowers on the paperwork involved in securing different types of loans from banks.