This document provides an overview of various legal topics related to banking and the legal environment in Bangladesh, including:

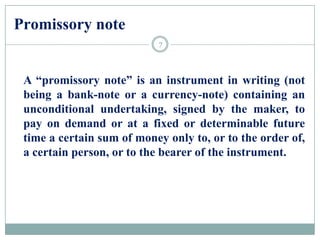

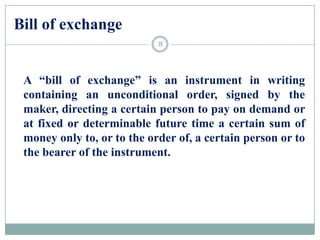

1. It discusses several laws governing financial instruments, such as the Negotiable Instruments Act 1881, which defines promissory notes, bills of exchange, cheques, and demand drafts. It also covers the Money Laundering Prevention Act and Anti-Terrorism Act.

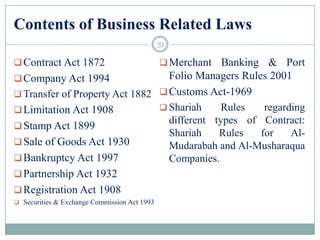

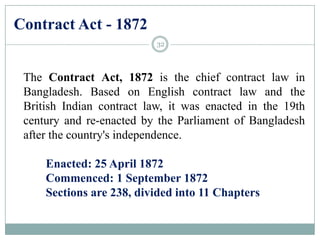

2. It then covers various business related laws in Bangladesh, including the Contract Act 1872, Companies Act 1994, Transfer of Property Act 1882, and others.

3. It also provides details on key concepts around cheques, negotiable instruments, and money laundering prevention in the banking sector in Bangladesh according to local