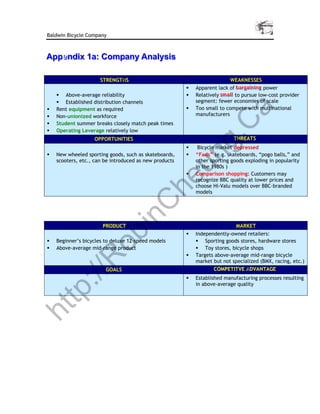

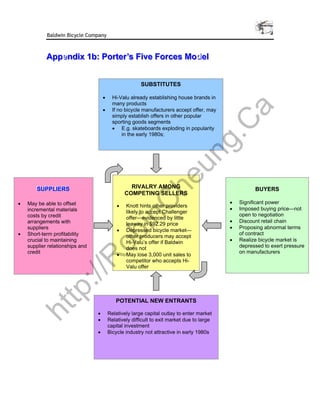

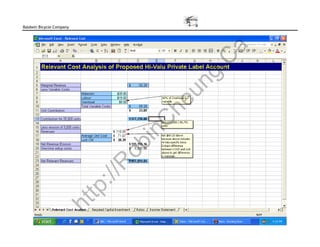

The document presents an analysis of Baldwin Bicycle Company's (BBC) proposal from Hi-Valu to produce a low-cost Challenger bicycle line under a private-label agreement. The proposal could yield substantial incremental revenues but deviates from standard practices and poses significant financial risks due to unfavorable payment terms and BBC's already high debt-equity ratio. Recommendations suggest pursuing short-term agreements or distribution partnerships to mitigate risks while considering a potential restructuring of operations.