Download as PDF, PPTX

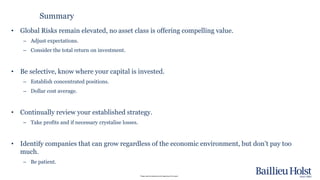

The Baillieu Holst post-election seminar held on July 21, 2016, provided an economic overview and market update, emphasizing the importance of tailored investment advice and the implications of recent superannuation changes. Key issues discussed included the effects of political uncertainty on financial markets and potential slowdowns in growth and productivity in developed economies. Attendees were advised to seek professional advice before making investment decisions, especially in light of the evolving economic landscape and regulatory changes.