Ayesha Noor the student of BBA(Hons) and i have done diploma in commerce and i have done diploma in information technology

1.

Financial Management refersto the planning, organizing, directing, and controlling of financial

resources in an organization or individual’s life to achieve their financial goals. It involves

decisions related to investments, financing, dividends, and managing resources efficiently. A

strong financial management system helps organizations and individuals use their financial

resources wisely, ensuring that they meet short-term and long-term goals.

Here's a deeper look at key areas within financial management, along with some practical

examples:

1. Investment Decisions (Capital Budgeting)

Definition: Investment decisions involve determining which projects or assets a company

should invest in, in order to maximize returns. It includes evaluating potential

investments, deciding which ones to pursue, and allocating funds accordingly.

Key Concepts:

o Net Present Value (NPV): The difference between the present value of cash

inflows and outflows over a period of time. A positive NPV indicates a good

investment.

o Internal Rate of Return (IRR): The discount rate at which the NPV of all cash

flows from a project equals zero. It helps in evaluating the profitability of an

investment.

Example: Imagine a company that wants to decide between two projects:

o Project A has an expected return of $500,000, and its NPV is $100,000.

o Project B has an expected return of $450,000, and its NPV is $120,000. The

company would likely invest in Project B, as it provides a higher return relative

to its cost.

2. Financing Decisions (Capital Structure)

Definition: Financing decisions concern how a company raises capital to fund its

operations and investments. These decisions revolve around the mix of debt and equity

used by a company to finance its activities.

Key Concepts:

o Debt Financing: Borrowing money, usually in the form of loans or bonds.

o Equity Financing: Raising capital by issuing shares of stock.

o Optimal Capital Structure: The balance between debt and equity that minimizes

the cost of capital and maximizes shareholder value.

Example: A company might face a choice between issuing new stock or borrowing

money through bonds to raise $1 million for an expansion project.

o Debt Option: Issue bonds with an interest rate of 5%, but the company will have

to repay principal and interest.

o Equity Option: Issue 100,000 new shares at $10 per share. While there is no

repayment obligation, the company will dilute the ownership of current

shareholders. The company’s financial manager would need to calculate which

option minimizes costs and risk while maximizing shareholder value.

2.

3. Dividend Decisions

Definition: Dividend decisions are concerned with how much of a company's earnings

should be distributed to shareholders as dividends and how much should be retained for

reinvestment.

Key Concepts:

o Dividend Payout Ratio: The proportion of earnings paid out as dividends.

o Retention Ratio: The proportion of earnings retained in the business.

o Stable Dividends: Companies may aim for a stable or gradually increasing

dividend to maintain investor confidence.

Example: A company earns $10 million in profit and decides that 40% will be paid as

dividends ($4 million), while 60% ($6 million) will be retained to fund growth initiatives

such as expansion or R&D.

4. Working Capital Management

Definition: Working capital management involves managing short-term assets and

liabilities to ensure that a company has enough liquidity to meet its day-to-day

operational needs.

Key Concepts:

o Current Assets: Cash, accounts receivable, and inventory.

o Current Liabilities: Short-term debts, accounts payable, and accrued expenses.

o Cash Conversion Cycle: The time it takes for a company to convert its

investments in inventory and accounts receivable into cash.

Example: A retail company needs to ensure that it has enough inventory on hand to meet

demand, while also managing accounts payable and receivable efficiently. If the

company has $2 million in accounts receivable and $1.5 million in accounts payable,

managing the timing of collections and payments is critical to maintaining liquidity.

5. Risk Management

Definition: Risk management in financial management involves identifying, analyzing,

and mitigating the financial risks that a company may face. These risks may include

market risk, credit risk, operational risk, and others.

Key Concepts:

o Hedging: Using financial instruments like options or futures to offset potential

losses.

o Diversification: Spreading investments across different assets or markets to

reduce risk.

Example: A company in the oil industry might use futures contracts to lock in oil prices

to protect itself from future price fluctuations. Alternatively, it might diversify its

investment portfolio to include stocks, bonds, and international assets to reduce exposure

to a single market.

6. Financial Reporting and Analysis

3.

Definition: Financialreporting involves preparing and analyzing financial statements,

which provide insights into a company's financial performance. Key reports include the

Income Statement, Balance Sheet, and Cash Flow Statement.

Key Concepts:

o Profitability Ratios: Measures like Return on Equity (ROE), Return on Assets

(ROA), and profit margin.

o Liquidity Ratios: Measures like the current ratio and quick ratio to determine if

the company can meet its short-term obligations.

o Leverage Ratios: Measures of a company’s debt levels, such as the debt-to-

equity ratio.

Example: A company may analyze its Return on Assets (ROA) to determine how

efficiently it is using its assets to generate profit. If the ROA is 5%, it means the company

is generating $0.05 in profit for every dollar of assets.

Summary

In financial management, these areas (investment decisions, financing decisions, dividend

decisions, working capital management, risk management, and financial reporting) all work

together to ensure that resources are effectively utilized to achieve the financial goals of an

organization or individual. By making informed decisions, companies can maximize their value,

reduce risk, and maintain a healthy financial position.

If you’d like to go deeper into any of these topics, feel free to ask!

Business Finance and Management is a broad and complex field that involves managing a

company’s financial resources, making investment and funding decisions, and ensuring the

efficient operation of financial activities to achieve organizational goals. It's concerned with

obtaining, allocating, and using financial resources to ensure that the business can meet its

objectives and grow.

Here, we’ll explore business finance and management in depth, covering the major aspects and

providing real-world examples:

1. Financial Management

4.

Financial management isabout overseeing and managing a company’s financial activities,

including investments, budgeting, and cash flow management. It aims to maximize shareholder

wealth and ensure the company has enough capital to function effectively.

Key Elements:

Investment Decisions (Capital Budgeting): Deciding where and how to allocate financial

resources for the company's long-term growth.

Financing Decisions (Capital Structure): Determining how to finance investments,

whether through debt, equity, or internal cash flows.

Dividend Decisions: Deciding how much profit should be distributed to shareholders

versus retained for reinvestment.

Example:

A company like Tesla may need to decide whether to use its retained earnings or issue new

equity to fund its next major research project. If it issues equity, it risks diluting current

shareholders, but if it uses debt financing, it incurs interest expenses.

2. Capital Budgeting and Investment Decisions

Capital budgeting refers to the process of evaluating and selecting long-term investment

opportunities that are expected to generate returns over time. This is essential for the company’s

growth and sustainability.

Methods Used:

Net Present Value (NPV): Calculates the difference between the present value of cash

inflows and outflows. A project with a positive NPV is typically considered a good

investment.

Internal Rate of Return (IRR): The discount rate that makes the NPV of a project zero.

If the IRR exceeds the company's required return, the project is acceptable.

Payback Period: Measures how long it takes for an investment to recover its initial cost.

Profitability Index: A ratio that compares the present value of future cash inflows to the

initial investment.

Example:

A company is evaluating two projects:

Project A: Requires an initial investment of $1 million and is expected to generate

$300,000 per year for 5 years. The NPV is $500,000.

Project B: Requires an initial investment of $1.5 million and generates $400,000

annually for 5 years. The NPV is $450,000.

Based on NPV, the company would choose Project A because it provides a higher return

for a lower initial investment.

5.

3. Working CapitalManagement

Working capital management involves managing the short-term assets and liabilities of the

business to ensure it has enough liquidity to meet its operational needs.

Components of Working Capital:

Current Assets: Cash, accounts receivable, inventory.

Current Liabilities: Accounts payable, short-term debt.

Key Ratios:

Current Ratio = Current Assets ÷ Current Liabilities. This ratio indicates if the business

can pay its short-term debts.

Quick Ratio = (Current Assets - Inventory) ÷ Current Liabilities. This is a more stringent

test of liquidity.

Cash Conversion Cycle: Measures how long it takes for a company to convert its

investments in inventory and receivables into cash.

Example:

A retail business may keep a large inventory of products. If the inventory turnover ratio is low, it

could indicate that products are sitting unsold for a long time, tying up cash. Effective working

capital management would involve reducing excess inventory or improving the collection of

receivables to improve cash flow.

4. Financing Decisions (Capital Structure)

Financing decisions involve determining the optimal mix of debt (loans, bonds) and equity

(stocks, retained earnings) for the company. The goal is to minimize the cost of capital and

maximize shareholder wealth.

Key Concepts:

Debt Financing: Borrowing funds that need to be repaid, often with interest. It can be in

the form of loans, bonds, or other debt instruments.

Equity Financing: Raising capital by issuing shares to investors, diluting ownership but

not incurring debt.

Optimal Capital Structure: The mix of debt and equity that minimizes the cost of

capital and maximizes the value of the firm.

Example:

Apple Inc. is a good example of how capital structure can evolve over time. Apple once relied

6.

heavily on debtto finance its operations, but as the company grew and became more profitable, it

shifted toward using more equity financing. This allowed them to preserve financial flexibility

while still returning value to shareholders.

5. Financial Reporting and Analysis

Business finance involves preparing accurate financial reports and analyzing the company's

financial health. The three primary financial statements are:

Income Statement: Shows the company’s revenues, costs, and profits over a period.

Balance Sheet: Provides a snapshot of the company’s assets, liabilities, and equity at a

point in time.

Cash Flow Statement: Shows the inflow and outflow of cash, indicating the company's

liquidity and ability to meet its short-term obligations.

Key Ratios for Analysis:

Profitability Ratios (e.g., ROE, ROA, Gross Margin).

Liquidity Ratios (e.g., Current Ratio, Quick Ratio).

Solvency Ratios (e.g., Debt-to-Equity Ratio, Interest Coverage Ratio).

Example:

Consider Amazon. By analyzing its financial statements, Amazon’s management can assess its

profitability (through metrics like gross margin) and liquidity (through the current ratio). In

2020, despite massive growth, Amazon focused on improving cash flow and minimizing debt,

ensuring it had enough liquidity to handle disruptions like the COVID-19 pandemic.

6. Risk Management

Managing financial risks involves identifying potential risks, assessing their impact, and

developing strategies to minimize or avoid them. These risks can include market risk, credit risk,

liquidity risk, operational risk, etc.

Techniques for Managing Financial Risk:

Hedging: Using financial instruments like futures, options, or swaps to mitigate potential

losses from changes in market conditions.

Diversification: Spreading investments across different assets or markets to reduce

exposure to any one risk.

Insurance: Purchasing policies to protect the business against potential losses, such as

property damage, liability claims, or cyber risks.

7.

Example:

Airlines often facefuel price fluctuations, so they might use fuel hedging to lock in fuel prices

for a period to reduce the uncertainty of operating costs. A company like Southwest Airlines is

well known for using hedging strategies to stabilize its fuel costs, especially when oil prices are

volatile.

7. Strategic Financial Management

Strategic financial management focuses on aligning the company’s financial management with

its broader strategic goals. This can involve mergers and acquisitions (M&A), expansion

strategies, and other large-scale initiatives.

Example:

Google’s acquisition of YouTube in 2006 for $1.65 billion is a prime example of a strategic

financial decision. Google recognized the growing power of video content and wanted to ensure

it had a platform to compete with emerging competitors. From a financial perspective, this

acquisition was a long-term investment that paid off by greatly expanding Google’s market share

in digital advertising.

Conclusion

Business Finance and Management plays a pivotal role in ensuring that a company’s financial

resources are used effectively to generate profit, minimize risk, and drive growth. By making

informed decisions about investments, financing, risk management, and reporting, businesses can

remain competitive and achieve long-term success.

Real-world companies like Tesla, Apple, Amazon, and Google offer practical examples of how

financial management practices are applied to drive growth, manage risk, and deliver value to

shareholders. Effective financial management provides businesses with the tools and insights

they need to make sound financial decisions that align with their strategic objectives.

Let me know if you'd like to dive deeper into any of these areas!

Forms of Business Organization refer to the legal structures under which a business can

operate. Each structure has its own set of rules, advantages, and disadvantages, and the choice of

8.

business form dependson various factors, such as the type of business, the level of liability, the

desired tax treatment, and the goals of the owners.

Let’s explore the main forms of business organization in-depth, along with examples:

1. Sole Proprietorship

Definition: A sole proprietorship is the simplest and most common form of business

organization. It is owned and operated by a single individual who has complete control

over all aspects of the business. The owner is responsible for all profits, losses, and

liabilities.

Key Features:

o Ownership: One individual owns and controls the business.

o Liability: The owner has unlimited personal liability for all business debts and

obligations.

o Taxation: Profits are taxed as personal income, avoiding double taxation.

o Management: The owner makes all decisions.

o Continuity: The business ends if the owner dies or decides to close it.

Advantages:

o Easy to set up and dissolve.

o Full control over decision-making.

o No corporate taxation; all income is reported on the owner’s personal tax return.

Disadvantages:

o Unlimited personal liability for business debts.

o Limited ability to raise capital or expand.

o May be harder to attract high-level talent or investors.

Example:

A local freelance graphic designer or plumber running a one-person business would

typically operate as a sole proprietorship. The owner handles all clients, finances, and

business decisions independently, without sharing profits or losses with anyone else.

2. Partnership

Definition: A partnership is a business structure where two or more individuals (or

entities) share ownership and the responsibilities of running a business. There are two

main types of partnerships: general partnerships and limited partnerships.

Key Features:

o Ownership: Two or more partners share ownership of the business.

o Liability: In a general partnership, all partners share equal responsibility for the

business's debts. In a limited partnership, one or more partners have limited

liability, while others have unlimited liability.

o Taxation: Profits and losses are passed through to the partners and taxed on their

personal returns (avoiding corporate taxation).

9.

o Management: Managementis shared among the partners, unless otherwise

specified in the partnership agreement.

o Continuity: The partnership may dissolve if one partner dies or withdraws, unless

a continuity agreement is in place.

Advantages:

o Easier to raise capital compared to a sole proprietorship.

o Shared responsibilities and resources among partners.

o Tax benefits due to pass-through taxation.

Disadvantages:

o Unlimited liability for general partners.

o Potential for conflict between partners.

o Partners may be personally liable for the actions of others.

Example:

Ben & Jerry's was originally a partnership between Ben Cohen and Jerry Greenfield,

who started a small ice cream shop together. They shared the profits, responsibilities, and

risks involved in the business, until they sold to Unilever.

3. Limited Liability Company (LLC)

Definition: A Limited Liability Company (LLC) is a hybrid business structure that

combines the limited liability features of a corporation with the tax efficiencies and

operational flexibility of a partnership.

Key Features:

o Ownership: Owners of an LLC are called members.

o Liability: Members have limited liability, meaning their personal assets are

protected from business debts and legal actions.

o Taxation: LLCs typically benefit from pass-through taxation where profits and

losses are reported on members' personal tax returns. However, LLCs can choose

to be taxed as a corporation.

o Management: An LLC can be managed by its members (member-managed) or

by designated managers (manager-managed).

o Continuity: An LLC can continue to exist even if a member leaves or dies.

Advantages:

o Limited liability protection for owners.

o Flexible management structure.

o Pass-through taxation.

o Fewer formalities compared to a corporation.

Disadvantages:

o Can be more expensive and complex to form than a sole proprietorship or

partnership.

o Some states impose additional taxes or fees on LLCs.

Example:

A small business like a local tech startup or consulting firm might choose to form an

LLC to take advantage of limited liability protection and pass-through taxation. For

10.

instance, Etsy, ane-commerce platform, initially operated as an LLC before expanding

into a corporation.

4. Corporation (C-Corp and S-Corp)

Definition: A corporation is a legal entity that is separate and distinct from its owners,

providing limited liability to shareholders. The corporation can enter into contracts, own

property, sue, and be sued in its own name.

Key Features:

o Ownership: Owned by shareholders who hold stock in the company.

o Liability: Shareholders have limited liability; they are not personally responsible

for the corporation's debts or legal issues.

o Taxation:

C-Corp: The corporation is taxed separately from its owners. The

corporation’s profits are taxed at the corporate rate, and dividends paid to

shareholders are taxed again on the individual level (double taxation).

S-Corp: An S-Corp is a special tax status that allows income, deductions,

and credits to be passed through to shareholders for federal tax purposes,

avoiding double taxation.

o Management: Managed by a board of directors who make major decisions, and

executives (e.g., CEO) who handle daily operations.

o Continuity: A corporation exists independently of the owners and can continue

indefinitely.

Advantages:

o Limited liability protection for shareholders.

o Ability to raise capital by issuing stock.

o Continuity of existence regardless of changes in ownership.

Disadvantages:

o Double taxation for C-Corporations.

o Expensive and time-consuming to set up and maintain (with more regulations).

o More complex management and governance structure.

Example:

Apple Inc. is a prominent example of a corporation. As a publicly traded company,

Apple has millions of shareholders, and its stock is traded on the stock market. The

company is managed by a board of directors and a team of executives.

5. Cooperative (Co-op)

Definition: A cooperative is a business owned and operated by a group of individuals for

their mutual benefit. Co-ops are typically formed to meet the common needs of their

members, such as reducing costs, sharing resources, or accessing services.

Key Features:

11.

o Ownership: Co-opsare owned and controlled by their members, who may be

customers, workers, or producers.

o Liability: Members have limited liability, similar to an LLC.

o Taxation: Co-ops enjoy tax advantages, especially in agricultural or consumer

co-ops, since profits are typically returned to the members.

o Management: Managed democratically, with each member having a vote in

decision-making, regardless of their contribution.

o Continuity: Like corporations, co-ops can continue even if members leave or die.

Advantages:

o Collective ownership and control.

o Often have tax benefits.

o Focused on member benefits rather than maximizing profits.

Disadvantages:

o Decision-making can be slow and cumbersome due to democratic structure.

o May face challenges in raising capital.

Example:

Ocean Spray is an agricultural cooperative owned by cranberry farmers. The cooperative

allows farmers to pool their resources, improve production efficiency, and share in the

profits generated from selling cranberry products.

Conclusion

Each form of business organization offers distinct advantages and challenges based on the

nature of the business, the desired level of liability protection, and the tax implications. Here’s a

quick summary:

Sole Proprietorship: Best for small businesses where the owner wants full control and

responsibility.

Partnership: Suitable for two or more individuals who want to share control, profits, and

risks.

LLC: Offers flexibility with limited liability, ideal for small to medium-sized businesses.

Corporation: Best for businesses looking to raise capital through stock issuance and

protect owners from liability.

Cooperative: Great for organizations formed to meet the collective needs of members,

often in industries like agriculture or retail.

Each business form has its own set of rules that dictate how it operates, and the choice of

structure should align with the business’s goals, size, and future plans. Let me know if you'd like

more details on any specific form or examples!

The goals of business finance are central to how a company operates, grows, and maximizes

value. These goals guide decisions about investments, capital structure, and resource allocation

12.

to achieve long-termfinancial stability and success. Understanding the key financial goals can

help a business align its strategies and ensure it remains financially healthy while achieving its

broader objectives.

Let’s explore the key goals of business finance in-depth, along with examples:

1. Maximizing Shareholder Wealth

Definition: The primary goal of business finance for most companies, especially publicly

traded ones, is to maximize the wealth of shareholders. This typically involves increasing

the value of the company’s stock and providing returns through dividends and capital

appreciation.

Key Concepts:

o Stock Price Appreciation: A company’s success and profitability are reflected in

its stock price. When the company performs well, the stock price typically rises,

benefiting shareholders.

o Dividends: Many companies pay dividends to shareholders as a portion of their

profits, which contributes to the overall wealth of the shareholders.

Why It’s Important: Maximizing shareholder wealth aligns with the goal of creating

value for investors, who provide capital to the company. It also attracts more investors,

which can lead to increased capital and opportunities for growth.

Example:

Apple Inc. is a prime example of maximizing shareholder wealth. Over the years, Apple

has focused on increasing its stock price and regularly returning profits to shareholders

through dividends and share buybacks. As a result, the company's stock has experienced

significant appreciation, creating immense value for its shareholders.

2. Profit Maximization

Definition: Profit maximization is the goal of generating the highest possible profit for

the business, which directly impacts the financial success of the company. It focuses on

the balance between revenue and costs.

Key Concepts:

o Revenue Generation: Increasing sales or creating new revenue streams.

o Cost Control: Reducing operating costs, overhead, and inefficiencies to

maximize profit.

Why It’s Important: Profit maximization is fundamental for any business because it

provides the financial resources needed to reinvest in the company, pay shareholders, and

sustain growth. However, it’s important to note that this goal should be balanced with

other factors like risk and sustainability.

Example:

Amazon has focused on profit maximization by scaling its e-commerce operations

13.

globally. The companyfocuses on increasing its revenue through product sales while also

managing its costs, such as optimizing supply chain operations and using technology to

reduce labor expenses. Amazon’s profitability has allowed it to reinvest in new ventures,

expanding into cloud computing (AWS), which has become a massive source of revenue.

3. Ensuring Liquidity (Solvency)

Definition: Liquidity refers to the ability of a business to meet its short-term financial

obligations as they come due. Solvency refers to the long-term financial stability of a

business—its ability to meet all financial obligations, both short-term and long-term.

Key Concepts:

o Current Ratio: A liquidity ratio that measures the ability of a business to cover

its short-term liabilities with its short-term assets. A ratio of 2:1 is often

considered healthy.

o Quick Ratio: A more stringent measure of liquidity, excluding inventory from

current assets. It helps assess a company’s ability to meet short-term obligations

without selling inventory.

o Cash Flow Management: Ensuring the company has sufficient cash flow to meet

obligations, pay employees, suppliers, and maintain operations.

Why It’s Important: Without adequate liquidity, a company could struggle to pay its

bills, employees, or creditors, leading to operational disruptions or even bankruptcy.

Solvency is also crucial for maintaining investor confidence and creditworthiness.

Example:

Tesla in its earlier years faced liquidity challenges as it needed significant capital to fund

its operations and expansion. The company had to secure financing from investors to stay

afloat. Over time, by focusing on growing its revenues, Tesla improved its cash flow and

liquidity, helping it to become solvent and continue its mission of scaling production.

4. Risk Management

Definition: Risk management in business finance involves identifying, analyzing, and

managing the financial risks a company faces. Risks can include market risk, operational

risk, credit risk, or external factors like economic downturns or regulatory changes.

Key Concepts:

o Hedging: Financial instruments like options and futures can be used to offset or

minimize risks, particularly in areas like commodity prices, interest rates, and

foreign exchange rates.

o Diversification: Spreading investments across various assets, industries, or

geographic areas to reduce the impact of risk.

o Insurance: Purchasing insurance policies to protect against specific risks, such as

property damage or liability claims.

14.

Why It’sImportant: Effective risk management helps protect the business from

unforeseen events and reduces the likelihood of financial distress. Companies that

manage risk well are often more resilient in the face of challenges and better able to

thrive in volatile markets.

Example:

Southwest Airlines is known for its hedging strategy to manage the risk of volatile fuel

prices. By locking in fuel prices ahead of time using financial instruments, Southwest

minimized the impact of sudden increases in fuel costs, allowing it to maintain

profitability even during times of rising oil prices.

5. Capital Structure Optimization

Definition: Capital structure refers to the mix of debt and equity financing a company

uses to fund its operations and growth. The goal is to find the optimal balance that

minimizes the cost of capital while maintaining enough flexibility and liquidity.

Key Concepts:

o Debt Financing: Borrowing money through loans or issuing bonds. Debt often

comes with fixed interest costs, but it can be tax-deductible and leverage a

company's growth.

o Equity Financing: Raising capital by issuing shares of stock. Equity financing

doesn’t require repayment, but it dilutes ownership and may limit control.

o Cost of Capital: The overall cost of financing, including the cost of debt and

equity. The goal is to minimize this cost to maximize value.

Why It’s Important: An optimal capital structure helps the company maximize its value

by reducing financing costs and minimizing risks. The structure impacts everything from

financial stability to the company’s ability to invest in future growth opportunities.

Example:

Microsoft has historically maintained a strong balance between debt and equity, using a

mix of retained earnings, equity issuance, and some debt financing. This allowed

Microsoft to invest heavily in product development and acquisitions, while maintaining a

relatively low debt load to avoid excessive financial risk.

6. Sustainability and Corporate Social Responsibility (CSR)

Definition: Increasingly, businesses are aligning their financial goals with sustainability

and corporate social responsibility. This involves making decisions that support

environmental and social goals while maintaining profitability.

Key Concepts:

o Environmental Sustainability: Ensuring that business practices do not harm the

environment and that resources are used efficiently.

o Social Responsibility: Acting in ways that benefit society, including fair labor

practices, philanthropy, and community development.

15.

o Triple BottomLine (TBL): A framework that evaluates a company’s social,

environmental, and financial performance.

Why It’s Important: Companies that embrace sustainability and CSR tend to have a

positive brand image, attract socially-conscious consumers, and maintain long-term

viability by adapting to societal and environmental challenges.

Example:

Patagonia is an excellent example of a company that integrates sustainability with its

financial goals. The company invests in eco-friendly production practices, promotes fair

labor practices, and donates a portion of its profits to environmental causes. Patagonia’s

commitment to sustainability has bolstered its brand and attracted a loyal customer base.

Conclusion

In business finance, the primary goals are interlinked but distinct. The most important goals

include:

1. Maximizing Shareholder Wealth – Achieving higher stock prices and providing returns

to shareholders.

2. Profit Maximization – Ensuring the business is generating the highest possible profit.

3. Ensuring Liquidity and Solvency – Ensuring the company can meet short-term and

long-term obligations.

4. Risk Management – Identifying and mitigating potential financial risks.

5. Capital Structure Optimization – Balancing debt and equity financing to minimize cost

and risk.

6. Sustainability and CSR – Integrating social and environmental goals with financial

objectives.

Each of these goals plays a vital role in the financial health and long-term success of the

company. By balancing profitability, risk, and long-term value creation, businesses can achieve

their financial objectives and thrive in a competitive environment.

If you'd like more details on any of these goals, or specific examples, feel free to ask!

Agency Problem: In-Depth Explanation

The agency problem arises from the conflicts of interest that can occur when one party (the principal)

delegates decision-making authority to another party (the agent). In the context of business, this

16.

situation typically involvesshareholders (principals) hiring managers (agents) to run the company on

their behalf. While the principal and agent ideally have aligned interests, differences in their objectives,

risk preferences, and incentives can create agency conflicts.

Key Concepts:

Principal: The person or entity that owns the resources or assets and delegates authority. In a

corporation, shareholders are the principals, as they own the company.

Agent: The individual or group hired by the principal to manage or operate the business. In a

corporation, the managers or executives are the agents.

Agency Cost: The costs that arise from resolving conflicts between principals and agents. These

costs can include monitoring costs, bonding costs, and the residual loss from not perfectly

aligning the interests of the two parties.

Why Does the Agency Problem Occur?

1. Divergent Objectives:

o Shareholders (Principals): Typically, the goal of shareholders is to maximize the value of

the company over the long term, reflected in the stock price and overall profitability.

Their interests are tied to the performance of the company.

o Managers (Agents): Managers may have goals that differ from shareholders’ interests,

such as increasing their own compensation, securing job stability, or pursuing personal

career goals, even at the cost of the company’s long-term performance.

2. Information Asymmetry:

o Asymmetry of Information: Managers often have more information about the day-to-

day operations of the business than shareholders. This gives managers the ability to

make decisions without fully revealing the information to the principals.

o Hidden Actions and Hidden Information: Managers might act in ways that are beneficial

to them (e.g., pursuing projects with short-term gains) rather than focusing on

maximizing shareholder wealth in the long run.

3. Moral Hazard:

o The agent may take actions that benefit themselves but harm the principal. For

instance, managers may take excessive risks with the company’s resources because they

don’t bear the full consequences of failure (since they don’t typically lose personal

wealth if the business fails).

4. Lack of Effective Monitoring:

o Shareholders cannot always monitor every decision made by managers due to costs and

practical limitations. Therefore, agents might exploit this by acting in ways that are not

in the best interest of the principal.

Types of Agency Problems

17.

1. Ownership vs.Control:

o In large corporations, the owners (shareholders) do not usually manage the business

themselves. Instead, they hire professional managers to do so. This creates a conflict

because managers may act in their own interest rather than the shareholders' best

interest.

o Example: A publicly traded company has many shareholders (owners) but a

management team running the company. The management might engage in actions

that improve their position (e.g., increasing personal perks, such as luxury office spaces

or higher salaries), even if these actions don’t align with the goal of maximizing

shareholder wealth.

2. Shareholders vs. Debt Holders:

o Shareholders typically prefer high-risk, high-reward strategies, as they benefit from

higher returns. Debt holders (creditors), however, prefer more conservative strategies

because they want to ensure their loans are repaid without risk.

o Example: A company that is highly leveraged (with significant debt) might make riskier

investments, which could benefit shareholders if the investments succeed, but

jeopardize the debt holders' capital if they fail.

Examples of the Agency Problem in Practice

Example 1: CEO Compensation and Performance

One of the classic examples of an agency problem is executive compensation. Managers might push for

higher salaries, stock options, or bonuses that are not directly tied to long-term performance. They

might receive lucrative compensation packages that provide immediate rewards even if their actions

don’t lead to long-term value creation for shareholders.

Example:

The 2008 Financial Crisis highlighted the agency problem within financial institutions. CEOs of

investment banks, such as Lehman Brothers and Merrill Lynch, received large bonuses tied to

short-term performance measures, even though their risky investment strategies led to long-

term financial instability. This incentivized managers to take excessive risks, knowing that they

could profit from short-term gains while externalizing the risks onto shareholders and creditors.

Example 2: Managers' Overinvestment in Pet Projects

Managers may pursue personal projects or investments that benefit them (such as expanding their

empire or securing more control) but do not necessarily increase shareholder value. This behavior is

sometimes referred to as empire building, where managers prefer to expand the company, even if

those expansions don’t yield good returns for the shareholders.

Example:

A diversified conglomerate might overexpand into unrelated businesses simply to increase its

size, which gives the CEO more prestige and control over a larger company. Shareholders,

18.

however, may seelittle to no return on this investment, especially if the new ventures are not

strategically aligned with the company’s core competencies.

Example 3: Risk Aversion vs. Risk Taking

The agency problem also manifests in differences in risk preferences between the principal and the

agent. Shareholders are generally willing to accept higher risks for higher potential returns, while

managers may avoid risky but potentially rewarding investments to preserve their positions and

minimize personal risk.

Example:

In tech startups, the founders (principals) might want to take on higher-risk, high-reward

strategies to grow quickly. However, the hired managers might avoid these strategies because

they fear the potential failure and its personal consequences (loss of their job or reputation). As

a result, managers may opt for safer, slower growth, even if it means lower potential returns for

shareholders.

Example 4: The "Golden Parachute"

Another example of the agency problem occurs when executives negotiate golden parachutes—

lucrative severance packages—before taking on risky roles. Even if their actions harm the company’s

shareholders, the executive is assured of a substantial financial safety net if they are fired.

Example:

Richard Fuld, the CEO of Lehman Brothers, had a golden parachute worth $22 million, despite

the firm’s collapse due to risky financial strategies. In this case, the CEO’s compensation package

was misaligned with the firm’s long-term interests, and his departure did not affect his financial

standing, even though shareholders lost billions.

How to Mitigate the Agency Problem

Businesses employ several strategies to align the interests of principals and agents, which can help

reduce the negative effects of the agency problem.

1. Performance-Based Compensation: Linking managerial compensation to company performance

is one way to align the interests of managers and shareholders. For example, stock options,

bonuses based on profit or revenue targets, and long-term incentive plans can incentivize

managers to act in the best interests of shareholders.

o Example:

Google (Alphabet) uses performance-based compensation, providing stock options that

vest over several years. This encourages managers to focus on long-term shareholder

value, as they benefit from stock price appreciation over time.

2. Monitoring and Governance: Establishing strong corporate governance, including independent

boards of directors, can help monitor management and ensure that decisions are made in the

19.

best interest ofshareholders. Regular audits, transparent reporting, and shareholder meetings

are tools to improve oversight.

o Example:

Apple Inc. has a well-established system of governance that includes an independent

board and rigorous financial reporting to ensure that management’s actions align with

shareholder interests.

3. Legal and Regulatory Mechanisms: Governments can implement laws and regulations that

protect shareholders and ensure proper accountability. Securities regulations, such as the

Sarbanes-Oxley Act (2002), require companies to improve financial transparency, prevent fraud,

and better align managerial incentives with shareholder interests.

4. Corporate Social Responsibility (CSR): In some cases, aligning corporate social responsibility

(CSR) goals with shareholder goals can help mitigate the agency problem. If managers believe

that long-term corporate reputation and sustainable growth are important, they may act in

ways that promote long-term value rather than short-term gains.

Conclusion

The agency problem is a fundamental issue in business finance that occurs when there is a conflict of

interest between the owners (shareholders) and those hired to manage the company (managers). This

misalignment can lead to inefficiencies, riskier business practices, and decisions that do not optimize the

company’s value for shareholders. However, various mechanisms like performance-based

compensation, effective governance, and legal regulations can help reduce the negative effects of

agency conflicts.

If you'd like to dive deeper into any specific aspect of the agency problem or its solutions, feel free to

ask!

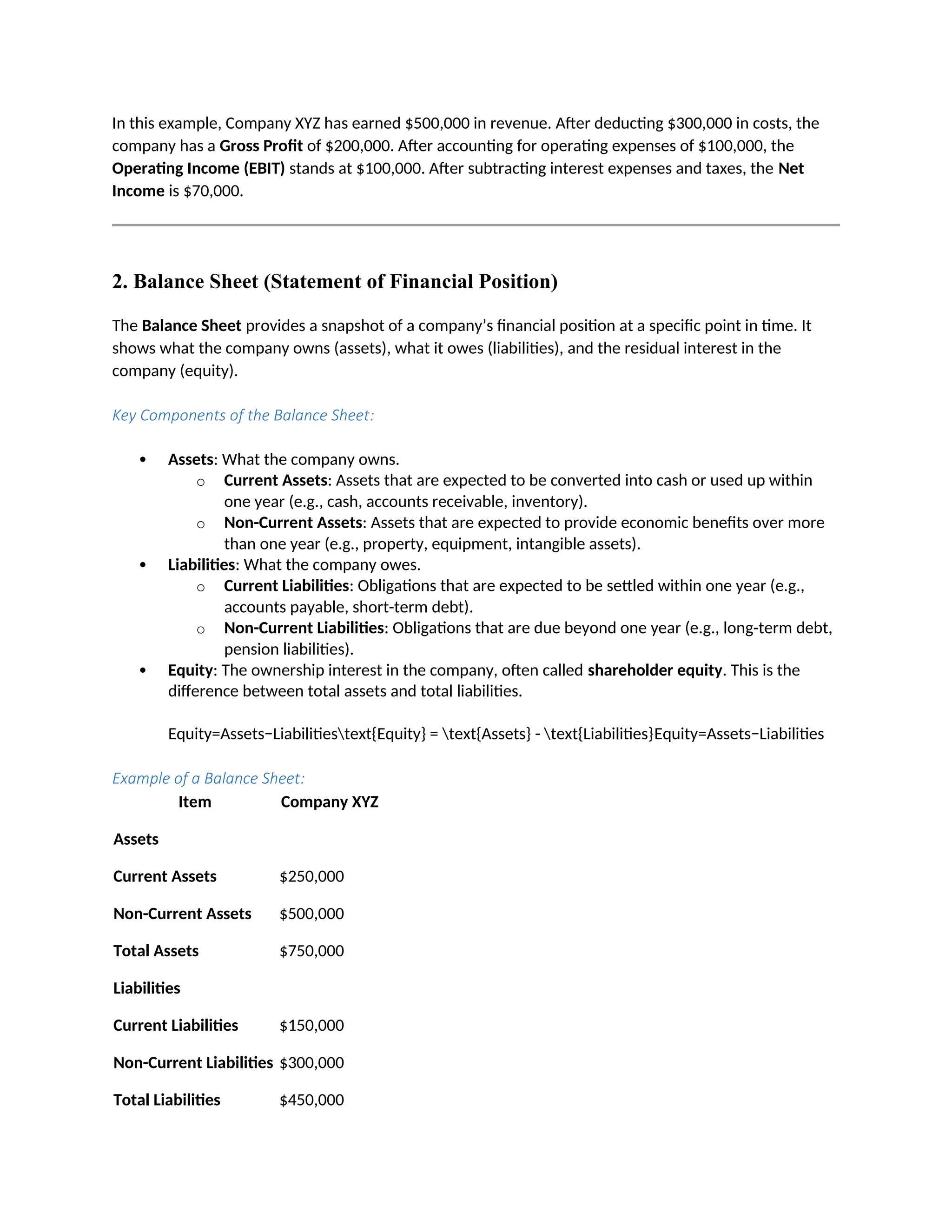

Balance Sheet: In-Depth Explanation

A balance sheet is one of the core financial statements used by businesses to provide a snapshot of their

financial position at a specific point in time. It is sometimes called a statement of financial position

because it provides a detailed summary of a company’s assets, liabilities, and shareholders' equity,

which together must balance according to the accounting equation:

Assets = Liabilities + Shareholders' Equity

20.

This equation isat the heart of the balance sheet, reflecting that everything a company owns (assets) is

financed either by borrowing money (liabilities) or by shareholders' investments (equity). The balance

sheet helps stakeholders like investors, creditors, and management understand the company’s financial

health, liquidity, and capital structure.

Components of the Balance Sheet

A typical balance sheet is divided into three main sections: Assets, Liabilities, and Shareholders' Equity.

Each of these categories is then broken down into subcategories to give more detail about the

company's financial structure.

1. Assets

Assets are everything a company owns or controls that has economic value and can be used to generate

future cash flows. Assets are generally classified into two main categories: current assets and non-

current assets.

a. Current Assets

Current assets are assets that are expected to be converted into cash, sold, or consumed within one

year or within the company's normal operating cycle, whichever is longer. These are considered the

most liquid assets because they can be used in the short term to pay for ongoing expenses or

obligations.

Examples of Current Assets:

o Cash and Cash Equivalents: Money available in bank accounts or short-term

investments.

o Accounts Receivable: Money owed to the company by customers for goods or services

provided on credit.

o Inventory: Goods or raw materials that the company intends to sell or use in its

operations within a year.

o Prepaid Expenses: Payments made for services or goods to be received in the future,

like insurance premiums or rent.

b. Non-Current Assets (Long-Term Assets)

Non-current assets are those that the company expects to hold for more than one year. These assets are

generally less liquid than current assets but are essential for the company's long-term growth and

operations.

Examples of Non-Current Assets:

o Property, Plant, and Equipment (PPE): Tangible assets like buildings, machinery, and

land used in operations. These assets are typically depreciated over time.

21.

o Intangible Assets:Non-physical assets such as patents, trademarks, goodwill, and

intellectual property. These assets are amortized over their useful lives.

o Investments: Long-term investments in other companies or financial assets that the

company plans to hold for more than one year.

2. Liabilities

Liabilities represent a company’s financial obligations or debts—amounts owed to creditors that must

be paid back in the future. Liabilities are similarly divided into current liabilities and non-current

liabilities.

a. Current Liabilities

Current liabilities are obligations the company must settle within one year or within its operating cycle,

whichever is longer.

Examples of Current Liabilities:

o Accounts Payable: Amounts the company owes to suppliers for goods or services

purchased on credit.

o Short-Term Debt: Loans or borrowings that are due within one year.

o Accrued Expenses: Expenses that have been incurred but not yet paid, such as wages,

taxes, or interest expenses.

o Unearned Revenue: Payments received from customers for goods or services that have

not yet been delivered.

b. Non-Current Liabilities

Non-current liabilities, also known as long-term liabilities, are obligations that the company does not

need to settle within the next year or operating cycle. These are usually paid back over a longer period,

often more than one year.

Examples of Non-Current Liabilities:

o Long-Term Debt: Loans or bonds payable after one year, such as bank loans or bonds

issued by the company.

o Deferred Tax Liabilities: Taxes owed that are deferred to be paid in the future, usually

due to timing differences between accounting and tax treatments.

o Pension Liabilities: Amounts owed under pension plans or retirement obligations.

3. Shareholders' Equity

Shareholders’ equity (also known as owner’s equity or net worth) represents the residual value of the

company’s assets after all liabilities have been paid. It reflects the ownership interest in the company.

Examples of Shareholders' Equity:

o Common Stock: The value of shares issued to shareholders, representing ownership in

the company.

22.

o Retained Earnings:The portion of the company’s profit that is not paid out as dividends

but is reinvested into the business.

o Additional Paid-In Capital: Money paid by investors above the par value of the stock

when shares are issued.

o Treasury Stock: The company’s own shares that have been repurchased from

shareholders but are not retired. This reduces equity.

o Other Comprehensive Income: Income that is not recognized in the income statement,

such as foreign currency translation adjustments or gains/losses on available-for-sale

securities.

The Basic Accounting Equation

The accounting equation is the foundation of the balance sheet:

Assets=Liabilities+Shareholders’ Equitytext{Assets} = text{Liabilities} + text{Shareholders'

Equity}Assets=Liabilities+Shareholders’ Equity

This equation must always be in balance because any increase in assets must be financed either through

borrowing (liabilities) or through the owners’ contributions (equity). The balance sheet reflects this

fundamental principle by listing assets on one side and liabilities and equity on the other side.

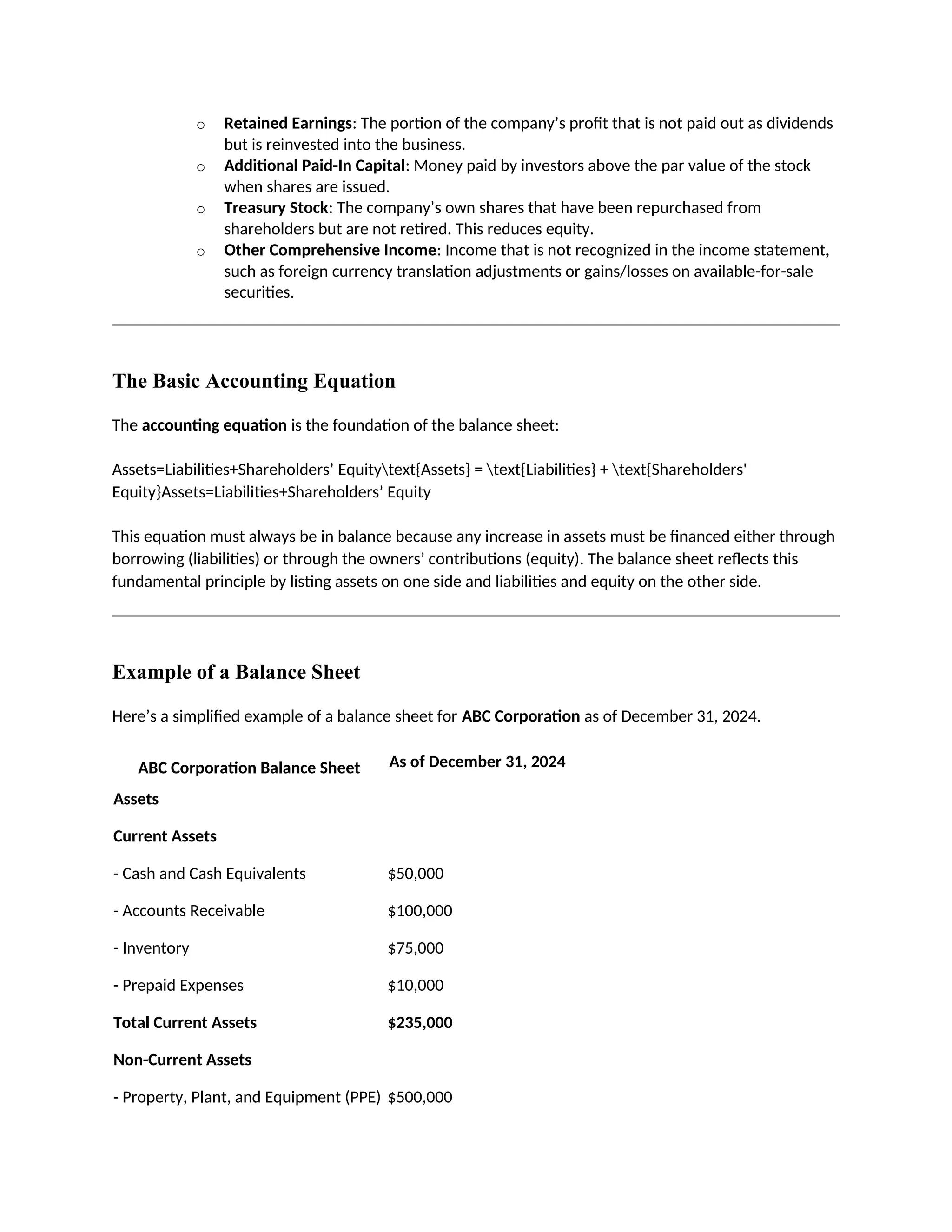

Example of a Balance Sheet

Here’s a simplified example of a balance sheet for ABC Corporation as of December 31, 2024.

ABC Corporation Balance Sheet As of December 31, 2024

Assets

Current Assets

- Cash and Cash Equivalents $50,000

- Accounts Receivable $100,000

- Inventory $75,000

- Prepaid Expenses $10,000

Total Current Assets $235,000

Non-Current Assets

- Property, Plant, and Equipment (PPE) $500,000

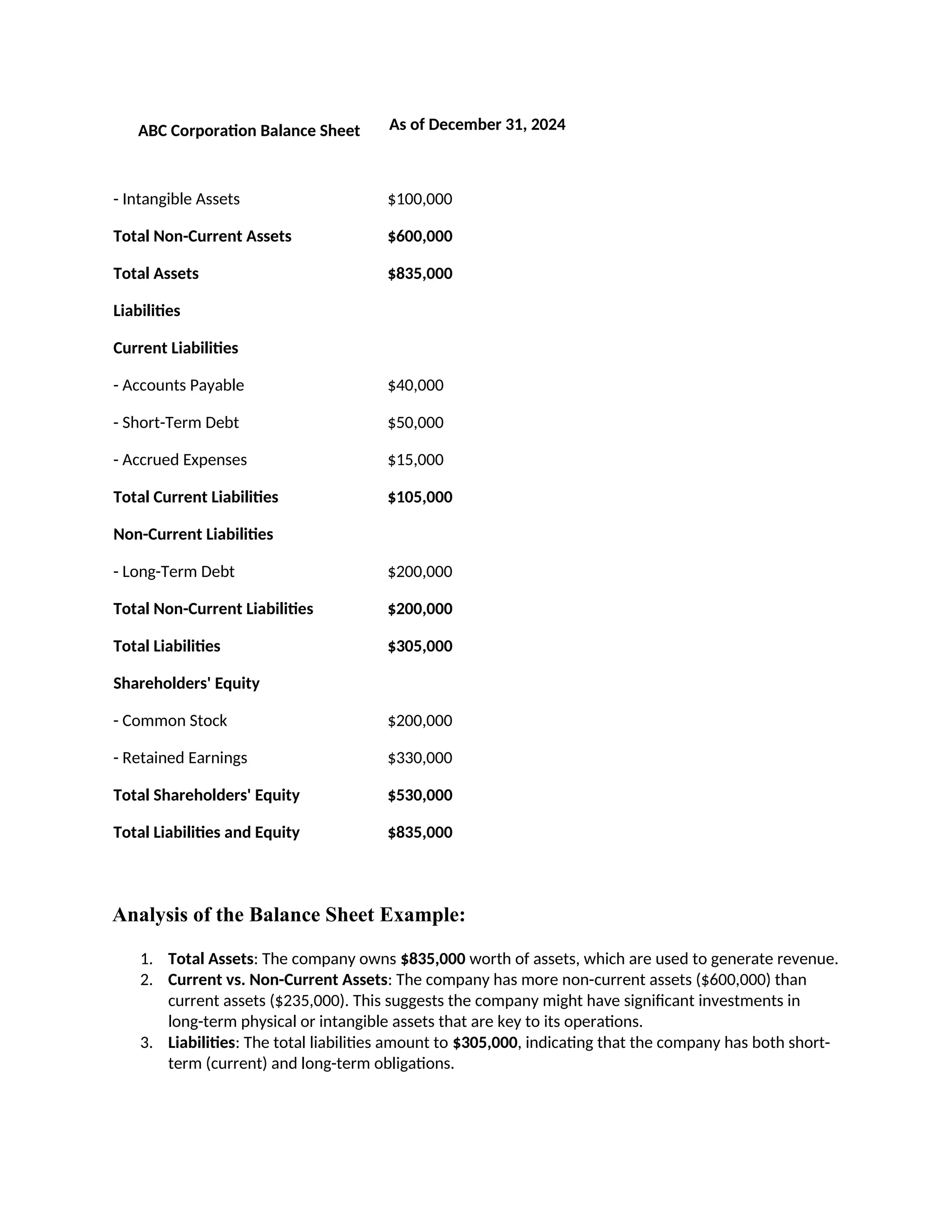

23.

ABC Corporation BalanceSheet As of December 31, 2024

- Intangible Assets $100,000

Total Non-Current Assets $600,000

Total Assets $835,000

Liabilities

Current Liabilities

- Accounts Payable $40,000

- Short-Term Debt $50,000

- Accrued Expenses $15,000

Total Current Liabilities $105,000

Non-Current Liabilities

- Long-Term Debt $200,000

Total Non-Current Liabilities $200,000

Total Liabilities $305,000

Shareholders' Equity

- Common Stock $200,000

- Retained Earnings $330,000

Total Shareholders' Equity $530,000

Total Liabilities and Equity $835,000

Analysis of the Balance Sheet Example:

1. Total Assets: The company owns $835,000 worth of assets, which are used to generate revenue.

2. Current vs. Non-Current Assets: The company has more non-current assets ($600,000) than

current assets ($235,000). This suggests the company might have significant investments in

long-term physical or intangible assets that are key to its operations.

3. Liabilities: The total liabilities amount to $305,000, indicating that the company has both short-

term (current) and long-term obligations.

24.

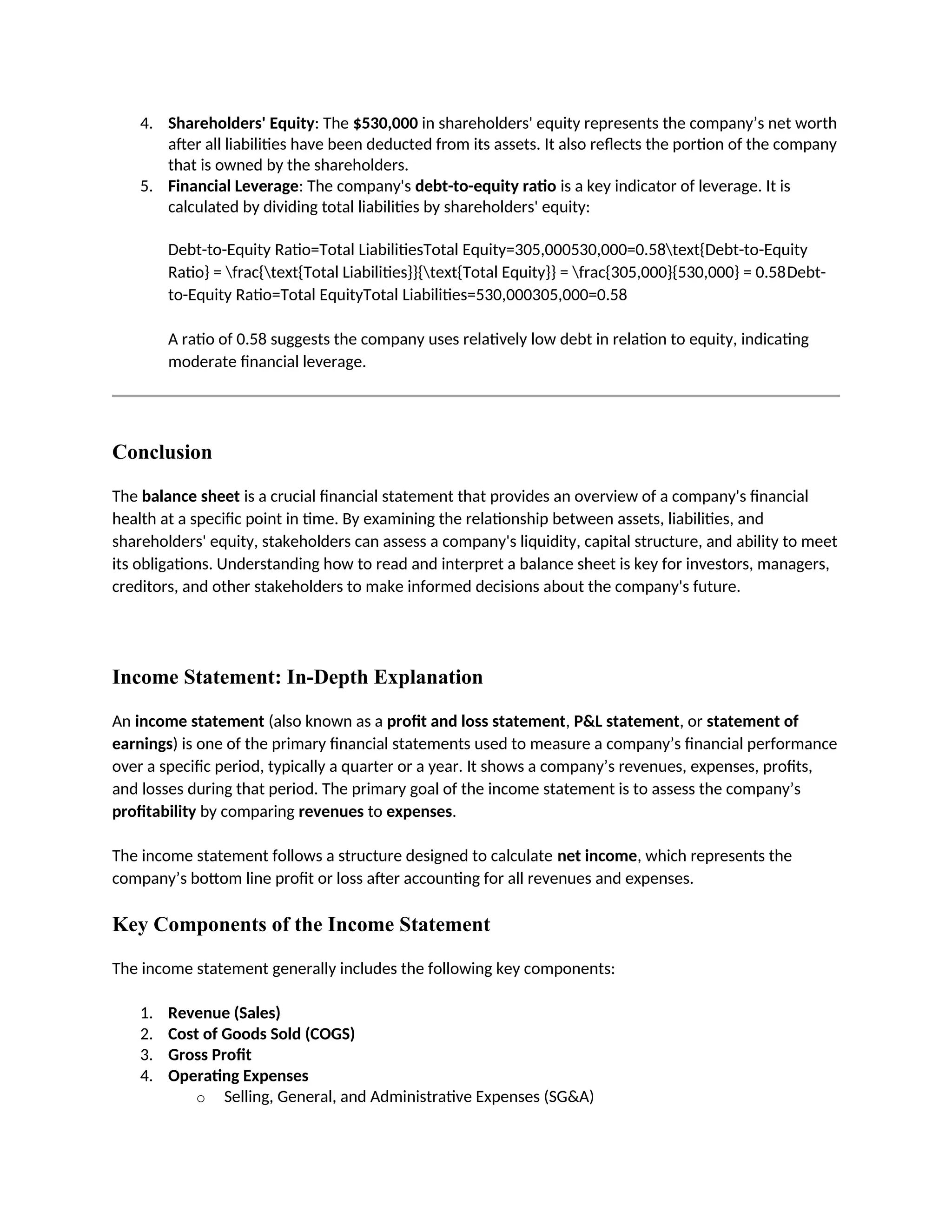

4. Shareholders' Equity:The $530,000 in shareholders' equity represents the company’s net worth

after all liabilities have been deducted from its assets. It also reflects the portion of the company

that is owned by the shareholders.

5. Financial Leverage: The company's debt-to-equity ratio is a key indicator of leverage. It is

calculated by dividing total liabilities by shareholders' equity:

Debt-to-Equity Ratio=Total LiabilitiesTotal Equity=305,000530,000=0.58text{Debt-to-Equity

Ratio} = frac{text{Total Liabilities}}{text{Total Equity}} = frac{305,000}{530,000} = 0.58Debt-

to-Equity Ratio=Total EquityTotal Liabilities=530,000305,000=0.58

A ratio of 0.58 suggests the company uses relatively low debt in relation to equity, indicating

moderate financial leverage.

Conclusion

The balance sheet is a crucial financial statement that provides an overview of a company's financial

health at a specific point in time. By examining the relationship between assets, liabilities, and

shareholders' equity, stakeholders can assess a company's liquidity, capital structure, and ability to meet

its obligations. Understanding how to read and interpret a balance sheet is key for investors, managers,

creditors, and other stakeholders to make informed decisions about the company's future.

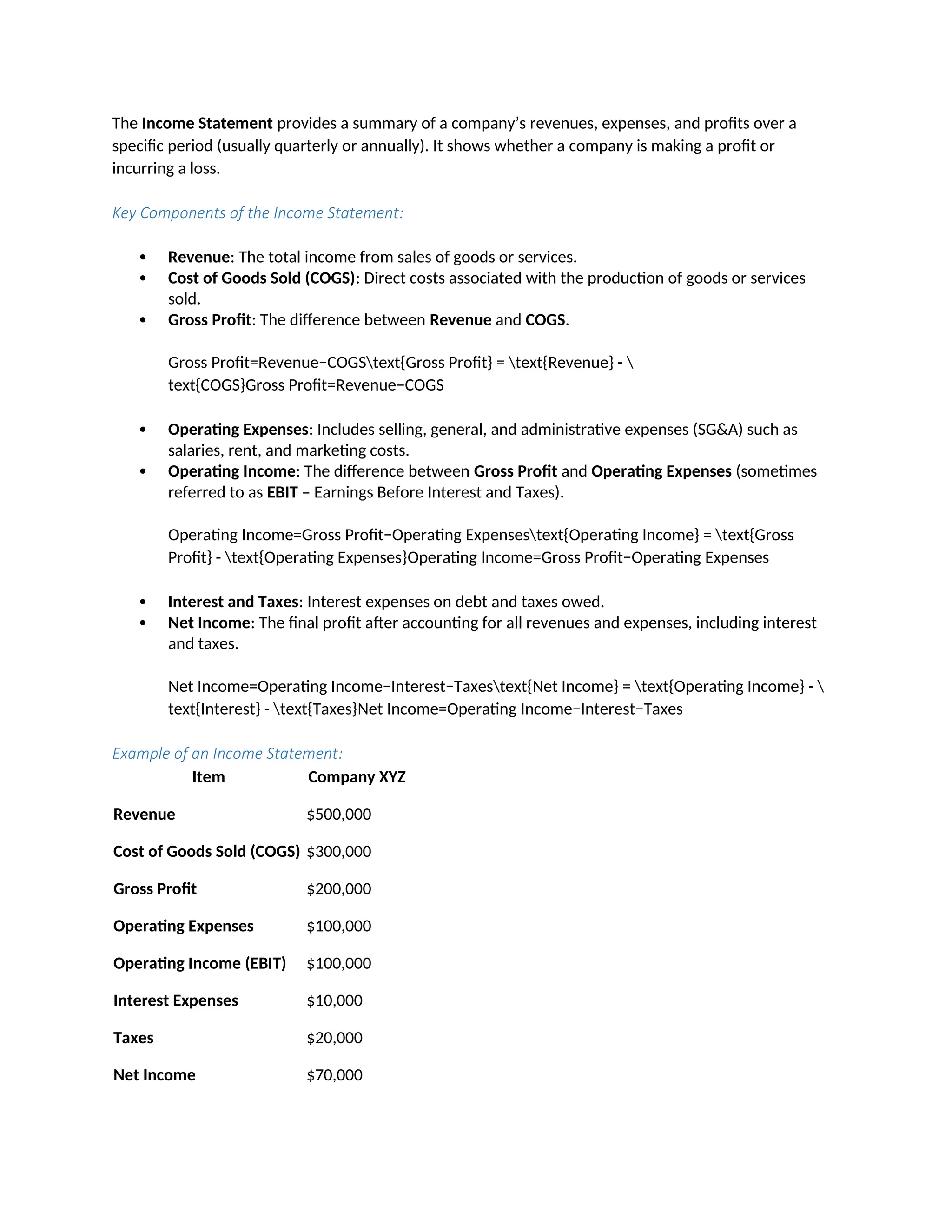

Income Statement: In-Depth Explanation

An income statement (also known as a profit and loss statement, P&L statement, or statement of

earnings) is one of the primary financial statements used to measure a company’s financial performance

over a specific period, typically a quarter or a year. It shows a company’s revenues, expenses, profits,

and losses during that period. The primary goal of the income statement is to assess the company’s

profitability by comparing revenues to expenses.

The income statement follows a structure designed to calculate net income, which represents the

company’s bottom line profit or loss after accounting for all revenues and expenses.

Key Components of the Income Statement

The income statement generally includes the following key components:

1. Revenue (Sales)

2. Cost of Goods Sold (COGS)

3. Gross Profit

4. Operating Expenses

o Selling, General, and Administrative Expenses (SG&A)

25.

o Depreciation andAmortization

5. Operating Income (EBIT)

6. Non-Operating Items

o Interest Expense

o Other Income and Expenses

7. Income Before Taxes

8. Income Tax Expense

9. Net Income (Net Profit or Loss)

Structure of the Income Statement

The structure of the income statement follows a simple formula:

Revenue−Cost of Goods Sold (COGS)=Gross Profittext{Revenue} - text{Cost of Goods Sold (COGS)} =

text{Gross Profit}Revenue−Cost of Goods Sold (COGS)=Gross Profit

Gross Profit−Operating Expenses=Operating Income (EBIT)text{Gross Profit} - text{Operating Expenses}

= text{Operating Income (EBIT)}Gross Profit−Operating Expenses=Operating Income (EBIT)

Operating Income (EBIT)−Non-Operating Expenses=Income Before Taxestext{Operating Income (EBIT)} -

text{Non-Operating Expenses} = text{Income Before Taxes}Operating Income (EBIT)−Non-

Operating Expenses=Income Before Taxes Income Before Taxes−Income Tax Expense=Net Income

text{Income Before Taxes} - text{Income Tax Expense} = text{Net

Income}Income Before Taxes−Income Tax Expense=Net Income

1. Revenue (Sales)

Revenue is the total income generated by the sale of goods or services during the period. It is the

starting point of the income statement and reflects the company’s ability to sell its products or services.

Example:

ABC Corp. sells computers. If they sell 10,000 units at $500 each, their revenue for the period is:

Revenue=10,000×500=5,000,000text{Revenue} = 10,000 times 500 =

5,000,000Revenue=10,000×500=5,000,000

Revenue includes all sales, regardless of whether cash has been received (credit sales are also

included).

2. Cost of Goods Sold (COGS)

COGS refers to the direct costs attributable to the production of the goods sold or services provided by

the company. This includes materials, labor, and overhead directly tied to the production process.

Example:

In the case of ABC Corp., the cost to manufacture each computer is $300. If they sold 10,000

units, the total COGS is:

26.

COGS=10,000×300=3,000,000text{COGS} = 10,000times 300 =

3,000,000COGS=10,000×300=3,000,000

3. Gross Profit

Gross profit is the difference between revenue and the cost of goods sold. It measures how efficiently a

company uses its resources (materials and labor) to produce goods or services.

Formula:

Gross Profit=Revenue−COGStext{Gross Profit} = text{Revenue} -

text{COGS}Gross Profit=Revenue−COGS

Example:

Continuing with ABC Corp.:

Gross Profit=5,000,000−3,000,000=2,000,000text{Gross Profit} = 5,000,000 - 3,000,000 =

2,000,000Gross Profit=5,000,000−3,000,000=2,000,000

Gross profit reflects the core profitability of the company’s primary business activities.

4. Operating Expenses (OPEX)

Operating expenses are the costs required to run the company on a day-to-day basis. These include

selling, general, and administrative expenses (SG&A), which cover salaries, rent, utilities, marketing,

and other non-production-related expenses.

Depreciation and amortization are also included in operating expenses, as they reflect the allocation of

the cost of tangible and intangible assets over time.

Example:

ABC Corp. has the following operating expenses:

o SG&A: $700,000

o Depreciation: $100,000 Total operating expenses = $800,000

5. Operating Income (EBIT)

Operating income, also called EBIT (Earnings Before Interest and Taxes), represents the company’s

profit generated from its core operations before accounting for interest and taxes.

Formula:

Operating Income (EBIT)=Gross Profit−Operating Expensestext{Operating Income (EBIT)} =

text{Gross Profit} - text{Operating

Expenses}Operating Income (EBIT)=Gross Profit−Operating Expenses

27.

Example:

For ABCCorp.:

Operating Income (EBIT)=2,000,000−800,000=1,200,000text{Operating Income (EBIT)} =

2,000,000 - 800,000 = 1,200,000Operating Income (EBIT)=2,000,000−800,000=1,200,000

Operating income is a key measure of a company’s profitability from its regular business

activities.

6. Non-Operating Items

Non-operating items are revenues or expenses that are not directly tied to the core business operations.

These include interest income or expense, gains or losses on asset sales, and other extraordinary items.

Interest Expense:

This is the cost of borrowing money. If a company has debt, it needs to pay interest on that debt, which

reduces its overall profitability.

Other Income/Expenses:

This category includes things like gains or losses on investments, currency fluctuations, or one-time

events.

Example:

ABC Corp. pays $50,000 in interest on its loans and receives $10,000 in interest income from

investments. The net non-operating income/expense would be:

Net Non-Operating Income=10,000−50,000=−40,000text{Net Non-Operating Income} = 10,000

- 50,000 = -40,000Net Non-Operating Income=10,000−50,000=−40,000

This shows a net expense from non-operating activities.

7. Income Before Taxes

Income before taxes is calculated as operating income plus any non-operating income or minus non-

operating expenses.

Formula:

Income Before Taxes=Operating Income (EBIT)+Non-Operating Income/Expensetext{Income

Before Taxes} = text{Operating Income (EBIT)} + text{Non-Operating

Income/Expense}Income Before Taxes=Operating Income (EBIT)+Non-Operating Income/

Expense

28.

Example:

For ABCCorp.:

Income Before Taxes=1,200,000−40,000=1,160,000text{Income Before Taxes} = 1,200,000 -

40,000 = 1,160,000Income Before Taxes=1,200,000−40,000=1,160,000

This figure is important as it represents the company’s earnings before it has to pay taxes.

8. Income Tax Expense

This represents the taxes that the company is required to pay based on its taxable income. The tax rate

varies by jurisdiction and the company’s taxable profits.

Example:

If ABC Corp. is subject to a 30% income tax rate, the tax expense would be:

Income Tax Expense=1,160,000×0.30=348,000text{Income Tax Expense} = 1,160,000 times

0.30 = 348,000Income Tax Expense=1,160,000×0.30=348,000

9. Net Income (Net Profit or Loss)

Finally, net income represents the company’s final profit or loss after all expenses, including taxes, have

been deducted from total revenues. It is often referred to as the bottom line of the income statement,

as it reflects the overall profitability of the company.

Formula:

Net Income=Income Before Taxes−Income Tax Expensetext{Net Income} = text{Income Before

Taxes} - text{Income Tax Expense}Net Income=Income Before Taxes−Income Tax Expense

Example:

For ABC Corp.:

Net Income=1,160,000−348,000=812,000text{Net Income} = 1,160,000 - 348,000 =

812,000Net Income=1,160,000−348,000=812,000

Net income is a key measure of the company’s profitability and is used by investors, creditors,

and management to evaluate financial performance.

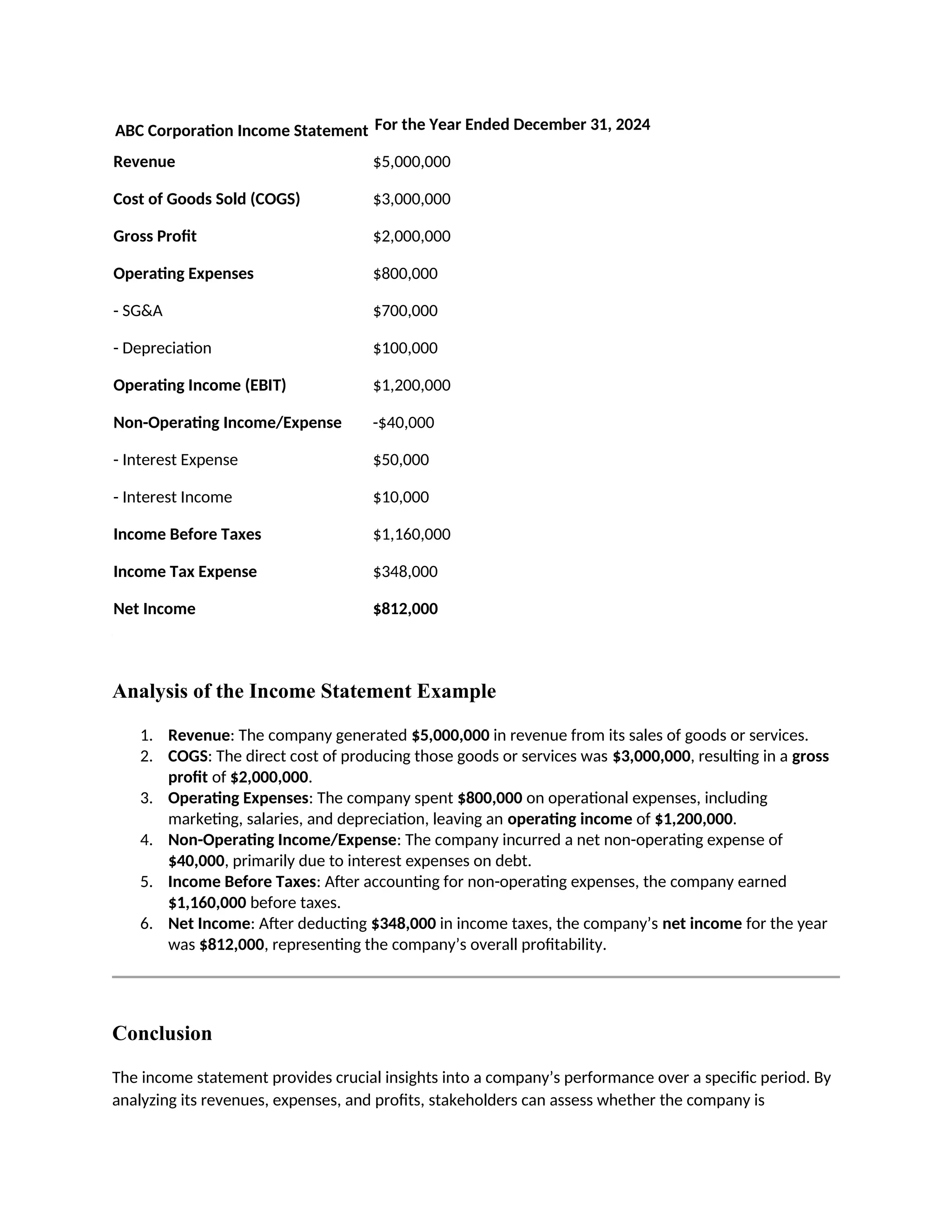

Example of a Full Income Statement

Here’s an example of a complete income statement for ABC Corporation for the year ended December

31, 2024:

29.

ABC Corporation IncomeStatement For the Year Ended December 31, 2024

Revenue $5,000,000

Cost of Goods Sold (COGS) $3,000,000

Gross Profit $2,000,000

Operating Expenses $800,000

- SG&A $700,000

- Depreciation $100,000

Operating Income (EBIT) $1,200,000

Non-Operating Income/Expense -$40,000

- Interest Expense $50,000

- Interest Income $10,000

Income Before Taxes $1,160,000

Income Tax Expense $348,000

Net Income $812,000

Analysis of the Income Statement Example

1. Revenue: The company generated $5,000,000 in revenue from its sales of goods or services.

2. COGS: The direct cost of producing those goods or services was $3,000,000, resulting in a gross

profit of $2,000,000.

3. Operating Expenses: The company spent $800,000 on operational expenses, including

marketing, salaries, and depreciation, leaving an operating income of $1,200,000.

4. Non-Operating Income/Expense: The company incurred a net non-operating expense of

$40,000, primarily due to interest expenses on debt.

5. Income Before Taxes: After accounting for non-operating expenses, the company earned

$1,160,000 before taxes.

6. Net Income: After deducting $348,000 in income taxes, the company’s net income for the year

was $812,000, representing the company’s overall profitability.

Conclusion

The income statement provides crucial insights into a company’s performance over a specific period. By

analyzing its revenues, expenses, and profits, stakeholders can assess whether the company is

30.

effectively managing itscosts, growing its sales, and generating sufficient profit. The net income figure at

the bottom of the statement is one of the most important indicators of financial health, and it plays a

key role in decision-making by investors, creditors, and company management.

Taxes: In-Depth Explanation

Taxes are mandatory financial charges or levies imposed by governments on individuals, businesses, and

other entities to fund government expenditures, such as public services, infrastructure, and defense.

They are a central element of the economic system, as they allow governments to raise revenue for

various programs and services that benefit society.

Taxes can take many forms, ranging from income taxes to sales taxes, property taxes, and corporate

taxes. Understanding taxes is essential for both individuals and businesses, as they impact financial

decisions, income, and profitability.

Types of Taxes

Taxes are categorized into several types, primarily based on their nature and the entities they apply to.

Below are the major types of taxes:

1. Income Taxes

Income taxes are taxes levied on the earnings of individuals or businesses. Governments typically

impose a progressive income tax system, where higher income is taxed at higher rates.

a. Individual Income Tax

This is the tax on personal income, which includes wages, salaries, interest, dividends, capital gains, and

other sources of income.

Example:

Suppose an individual earns $100,000 annually. If the tax rate is 20% on income up to $50,000,

and 30% on income above that, the tax would be calculated as:

text{Tax on First $50,000} = 50,000 times 0.20 = 10,000 text{Tax on Remaining $50,000} =

50,000 times 0.30 = 15,000 Total Income Tax=10,000+15,000=25,000text{Total Income Tax} =

10,000 + 15,000 = 25,000Total Income Tax=10,000+15,000=25,000

The individual would owe $25,000 in income tax.

31.

b. Corporate IncomeTax

Businesses also pay income taxes on their profits. The corporate income tax rate can vary by country

and is typically a fixed percentage of net income.

Example:

A corporation earns $1,000,000 in profit for the year. If the corporate tax rate is 25%, the

company would owe:

Corporate Tax=1,000,000×0.25=250,000text{Corporate Tax} = 1,000,000 times 0.25 =

250,000Corporate Tax=1,000,000×0.25=250,000

The corporation would pay $250,000 in income taxes.

2. Sales Tax

Sales tax is a consumption tax placed on the sale of goods and services. Typically, it is a percentage of

the sale price and is paid by the buyer, although businesses collect it and remit it to the government.

Example:

If a state imposes a sales tax rate of 8% and you purchase a $100 item, the sales tax would be:

Sales Tax=100×0.08=8text{Sales Tax} = 100 times 0.08 = 8Sales Tax=100×0.08=8

You would pay a total of $108 for the item, which includes the $8 sales tax.

3. Property Tax

Property taxes are levied on property owners, typically based on the value of their property (real

estate). This includes both land and buildings.

Example:

If a property is valued at $500,000 and the local government imposes a property tax rate of

1.5%, the tax would be:

Property Tax=500,000×0.015=7,500text{Property Tax} = 500,000 times 0.015 =

7,500Property Tax=500,000×0.015=7,500

The property owner would pay $7,500 in property taxes annually.

32.

4. Payroll Taxes

Payrolltaxes are taxes withheld from an employee's wages and used to fund social insurance programs

like Social Security, Medicare, and unemployment insurance.

a. Social Security and Medicare Taxes (FICA Taxes)

In the U.S., the Federal Insurance Contributions Act (FICA) requires employers to withhold social security

and Medicare taxes from employees' paychecks.

Example:

If an employee earns $60,000 annually, the total FICA tax rate (for Social Security and Medicare)

is 7.65%, split into 6.2% for Social Security and 1.45% for Medicare.

The tax would be calculated as:

FICA Tax=60,000×0.0765=4,590text{FICA Tax} = 60,000 times 0.0765 =

4,590FICA Tax=60,000×0.0765=4,590

The employee would owe $4,590 in payroll taxes for the year, which is withheld by the

employer and paid to the government.

5. Capital Gains Tax

Capital gains tax is levied on the profits from the sale of assets such as stocks, bonds, and real estate.

The rate varies based on the holding period (short-term vs. long-term) and the individual's tax bracket.

a. Short-Term Capital Gains Tax

If an asset is held for one year or less before being sold, the gain is considered short-term and is taxed at

the individual’s ordinary income tax rate.

b. Long-Term Capital Gains Tax

If the asset is held for more than one year, the gain is subject to a lower long-term capital gains tax rate.

Example:

If you sell an investment for $10,000 that you purchased for $7,000, your capital gain is $3,000.

If the long-term capital gains tax rate is 15%, the tax owed would be:

Capital Gains Tax=3,000×0.15=450text{Capital Gains Tax} = 3,000 times 0.15 =

450Capital Gains Tax=3,000×0.15=450

You would owe $450 in capital gains taxes.

33.

6. Estate andInheritance Taxes

Estate taxes are taxes imposed on the transfer of an estate upon an individual's death. Inheritance taxes

are taxes on the value of the assets inherited by heirs.

Example:

If a person inherits $1,000,000 from a deceased relative and the inheritance tax rate is 10%, the

heir would owe:

Inheritance Tax=1,000,000×0.10=100,000text{Inheritance Tax} = 1,000,000 times 0.10 =

100,000Inheritance Tax=1,000,000×0.10=100,000

The heir would pay $100,000 in inheritance taxes.

Taxation Systems

Different countries and regions employ different taxation systems. The key systems are:

1. Progressive Taxation

In a progressive tax system, the tax rate increases as the taxable amount increases. This is typically seen

in personal income taxes, where individuals with higher incomes are taxed at higher rates.

Example:

In a progressive tax system, if an individual earns $50,000, they may be taxed at a rate of 10%,

whereas someone earning $200,000 might be taxed at a rate of 30%.

2. Regressive Taxation

In a regressive tax system, the tax rate decreases as the taxable amount increases. This is commonly

seen in sales taxes, where the percentage remains constant but the relative impact is larger on lower-

income individuals because they spend a higher portion of their income on taxed goods.

Example:

A 10% sales tax on a $100 purchase is a smaller burden for a wealthy individual than for

someone with a lower income, as the tax is a larger percentage of their income.

3. Proportional (Flat) Taxation

In a flat tax system, everyone is taxed at the same rate, regardless of income level. This is often seen in

corporate taxes or certain individual income tax systems.

34.

Example:

If acountry implements a flat tax rate of 15%, both a person earning $50,000 and a person

earning $500,000 would pay the same percentage of their income in taxes.

International Tax Considerations

Multinational companies and individuals with assets in multiple countries may be subject to double

taxation, where both their home country and the country in which they operate tax their income. To

avoid this, many countries enter into tax treaties to reduce or eliminate double taxation.

Example:

A U.S.-based company operating in Europe may pay taxes to both the U.S. and the European

country. However, due to tax treaties, the company might receive a tax credit or exemption to

avoid being taxed twice on the same income.

Tax Avoidance vs. Tax Evasion

Tax Avoidance:

Tax avoidance is the legal practice of minimizing taxes by taking advantage of deductions,

credits, and other strategies. It's legal and often involves strategic planning to reduce tax

liabilities.

o Example:

A company might claim deductions for business expenses like office supplies, travel, and

depreciation to reduce its taxable income.

Tax Evasion:

Tax evasion is the illegal act of deliberately falsifying tax information or hiding income to avoid

paying taxes. It’s considered a crime and can lead to fines and penalties.

o Example:

A business might hide revenue from sales to avoid paying sales tax or underreport

income to reduce income tax obligations.

Conclusion

Taxes are essential for financing government functions and services, but they can be complex. Different

types of taxes, such as income taxes, sales taxes, and property taxes, affect individuals and businesses in

various ways. Understanding the intricacies of the tax system is important for making informed financial

decisions and ensuring compliance with tax laws. While tax avoidance strategies can help minimize

liabilities legally, tax evasion can result in significant penalties and legal consequences.

35.

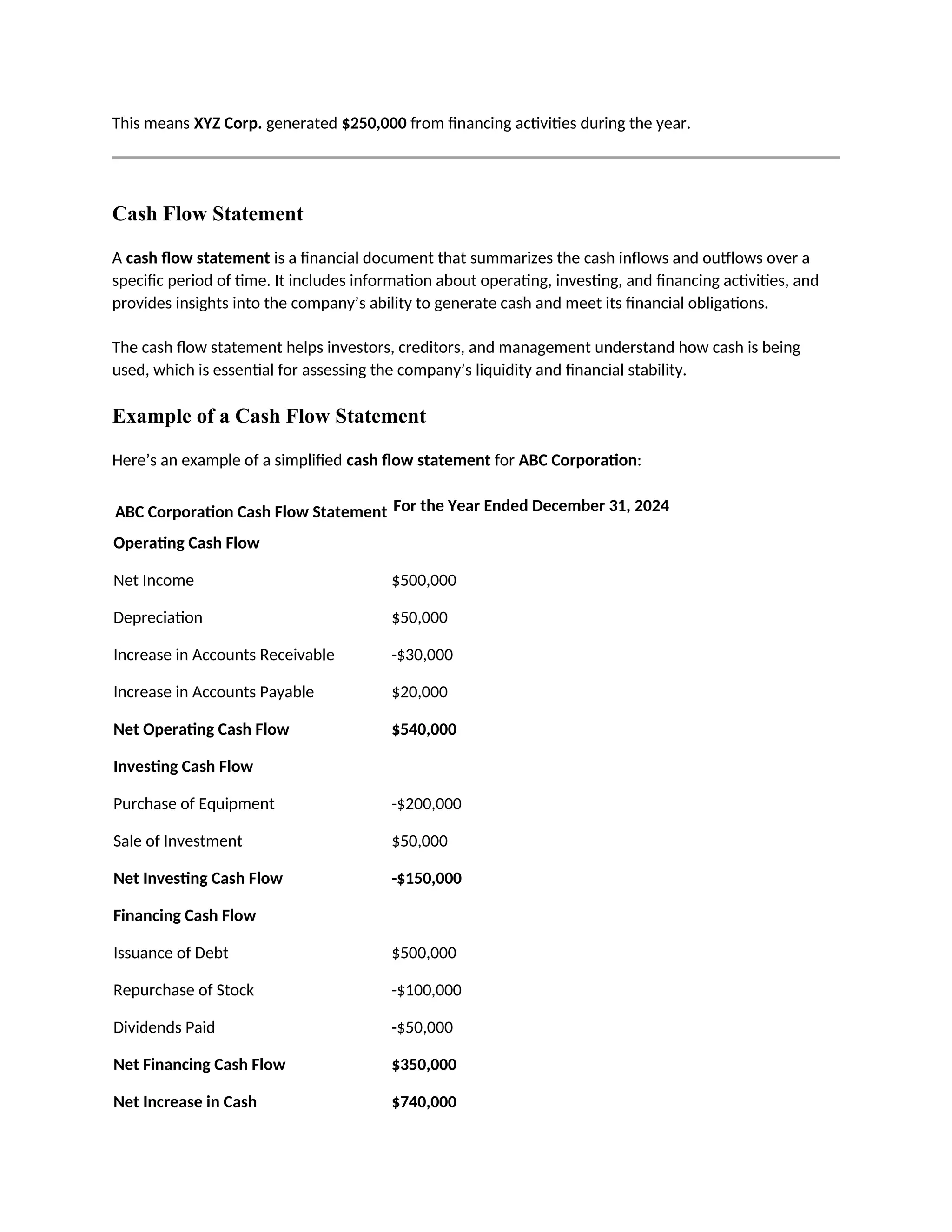

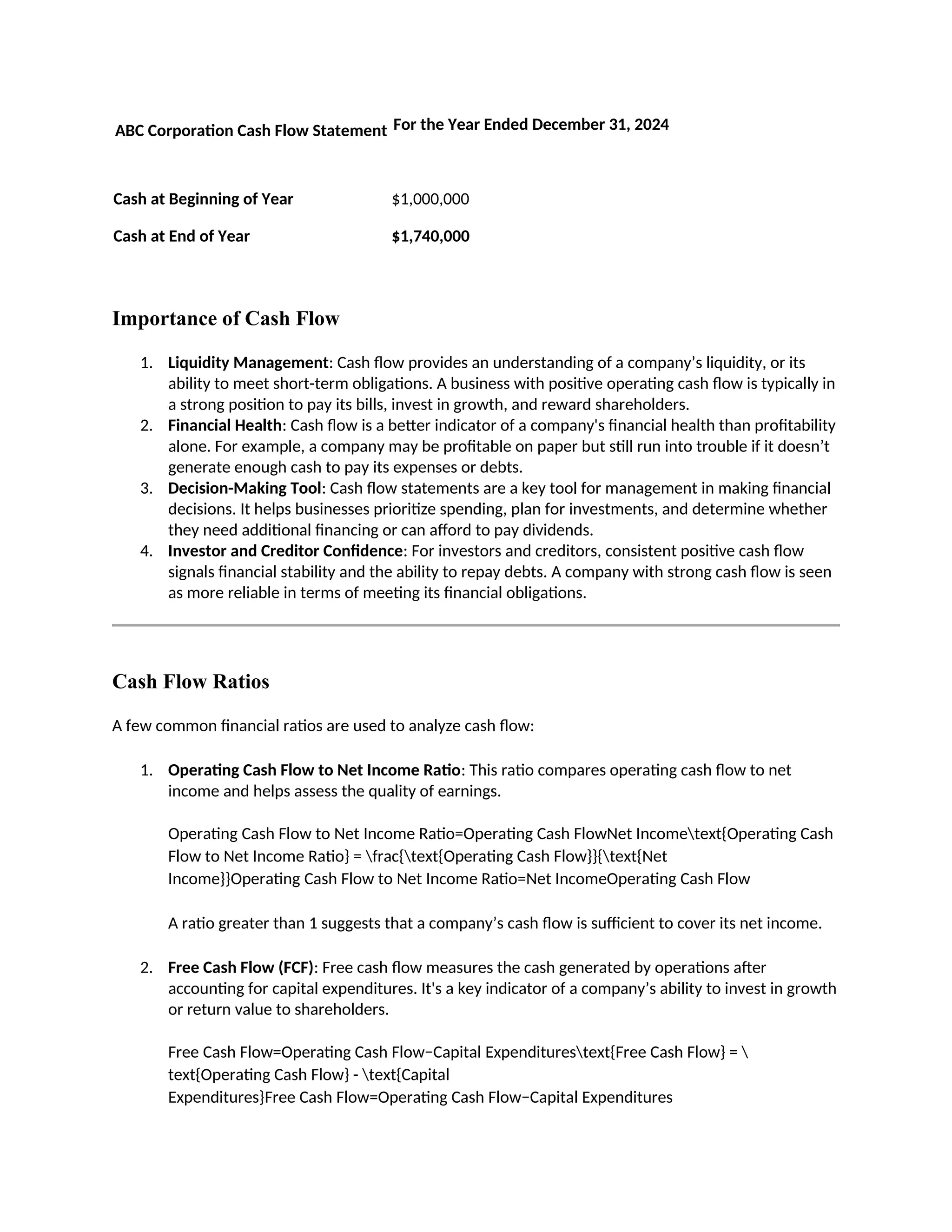

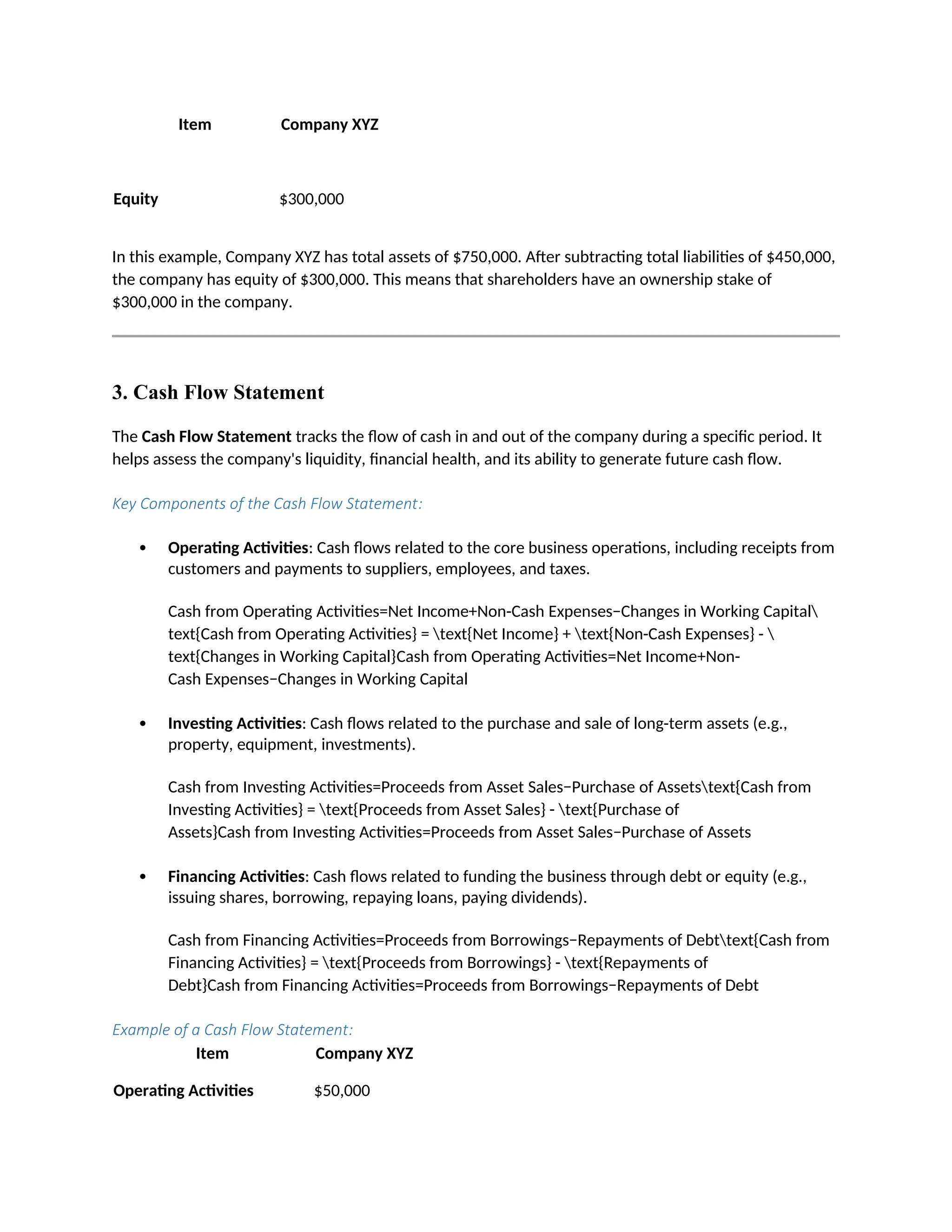

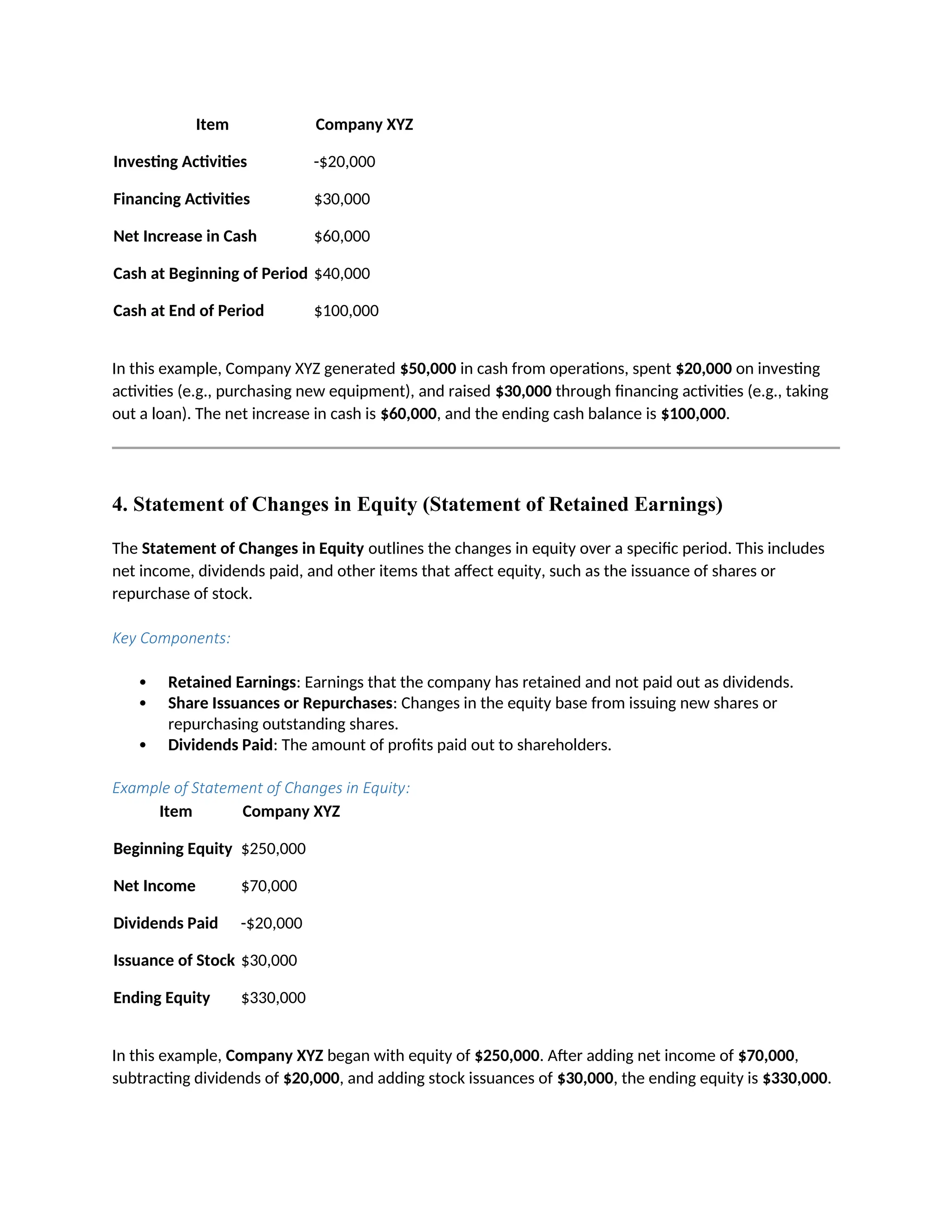

Cash Flow: In-DepthExplanation

Cash flow refers to the movement of money into and out of a business over a specific period of time. It

is an essential measure of a company's financial health and liquidity, showing how much cash a business

generates or spends from its operations, investments, and financing activities. Cash flow is crucial

because even a profitable business can face financial difficulties if it does not manage its cash flow

effectively.

The primary goal of cash flow analysis is to ensure that a business can meet its obligations, such as

paying bills, repaying loans, and funding growth, while also maintaining enough liquidity to continue

operations.

Types of Cash Flow

Cash flow is typically broken down into three main categories, reflecting the different sources of cash

inflows and outflows:

1. Operating Cash Flow (OCF)

2. Investing Cash Flow (ICF)

3. Financing Cash Flow (FCF)

1. Operating Cash Flow (OCF)

Operating cash flow is the cash generated or used by a company's core business activities. It represents

the net cash generated from the company’s day-to-day operations, excluding any investments or

financing activities.

Operating cash flow can be calculated using two methods:

Direct method: Lists all cash inflows and outflows from operating activities.

Indirect method: Starts with net income and adjusts for changes in working capital and non-

cash items like depreciation.

Key Components of Operating Cash Flow:

Cash Receipts from Customers: Cash inflows from the sale of goods or services.

Cash Payments to Suppliers: Cash outflows related to the production or acquisition of goods or

services.

36.

Operating Expenses:Cash outflows for wages, rent, utilities, etc.

Interest and Taxes: Cash payments related to interest on debt and taxes.

Example of Operating Cash Flow:

Let's assume XYZ Corp. reports the following activities for a quarter:

Revenue: $500,000 from sales to customers.

Payments to Suppliers: $200,000 for inventory and materials.

Operating Expenses: $100,000 in wages, rent, and utilities.

Interest Payments: $20,000.

Taxes: $30,000.

The operating cash flow can be calculated as follows:

Operating Cash Flow=Cash Receipts from Customers−Cash Payments to Suppliers−Operating Expenses−I

nterest Payments−Taxes Paidtext{Operating Cash Flow} = text{Cash Receipts from Customers} -

text{Cash Payments to Suppliers} - text{Operating Expenses} - text{Interest Payments} - text{Taxes

Paid}Operating Cash Flow=Cash Receipts from Customers−Cash Payments to Suppliers−Operating Expen

ses−Interest Payments−Taxes Paid

Operating Cash Flow=500,000−200,000−100,000−20,000−30,000=150,000text{Operating Cash Flow} =

500,000 - 200,000 - 100,000 - 20,000 - 30,000 =

150,000Operating Cash Flow=500,000−200,000−100,000−20,000−30,000=150,000

This means XYZ Corp. generated $150,000 in cash from its core operations for the quarter.

2. Investing Cash Flow (ICF)

Investing cash flow refers to the cash inflows and outflows associated with the acquisition and disposal

of long-term assets, such as property, equipment, or securities. It represents investments made by the

company in its future growth or returns.

Key Components of Investing Cash Flow:

Purchases of Property, Plant, and Equipment (Capex): Cash outflows for purchasing long-term

assets.

Proceeds from the Sale of Assets: Cash inflows from selling property, equipment, or

investments.

Investments in Securities: Cash outflows or inflows related to buying or selling investments.

Example of Investing Cash Flow:

Let's assume ABC Corp. made the following investments during the year:

37.

Purchased Equipment:$200,000.

Sold Property: $50,000.

Invested in Stocks: $30,000.

The investing cash flow is calculated as:

Investing Cash Flow=Proceeds from Sales−Purchases of Assets−Investments in Securitiestext{Investing

Cash Flow} = text{Proceeds from Sales} - text{Purchases of Assets} - text{Investments in

Securities}Investing Cash Flow=Proceeds from Sales−Purchases of Assets−Investments in Securities

Investing Cash Flow=50,000−200,000−30,000=−180,000text{Investing Cash Flow} = 50,000 - 200,000 -

30,000 = -180,000Investing Cash Flow=50,000−200,000−30,000=−180,000