Downloaded 101 times

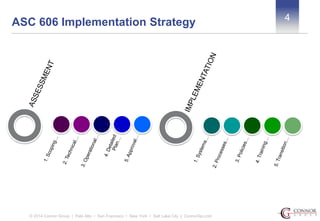

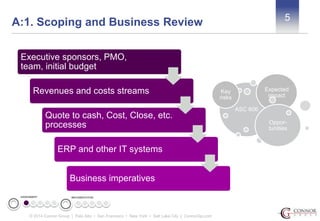

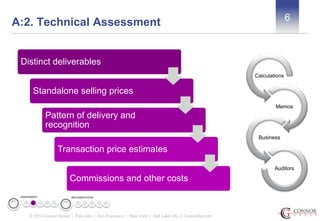

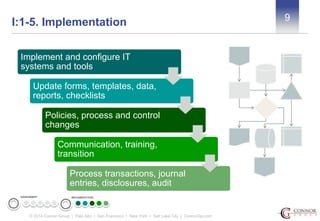

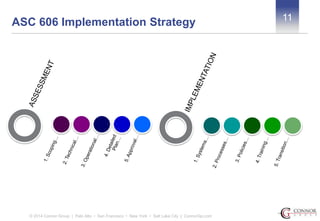

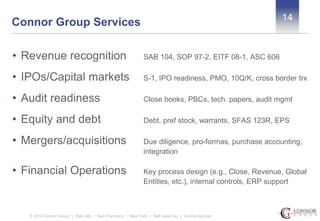

The document outlines the ASC 606 implementation strategy by Connor Group, detailing a structured approach to aid organizations in adapting to new revenue recognition standards. It highlights roles of key personnel, including experts in technical accounting and operational processes, and emphasizes the importance of assessment, planning, and implementation phases for successful transition. Connor Group offers a range of professional services, leveraging extensive experience across various industries to support clients with technical accounting, IPOs, M&A, and financial operations.

![[Webinar] From Tactical to Strategic: A Shift in the Understanding of Account...](https://cdn.slidesharecdn.com/ss_thumbnails/fromtacticaltostrategic-ashiftintheunderstandingofaccountspayable-131120124048-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)