More Related Content

PPTX

PPT

Keith quicksilver funding - amortized loans

PPT

2 2amortization-110921085439-phpapp01

PDF

Amortization (how to properly pr).pdf.pdf

PPTX

Unit 2 Chapter 2 Busines Finance Amortizatio Loan.pptx

PPTX

427158988-Business-and-Consumer-Loan-pptx.pptx

PPTX

mortgage and amortizationbusinessss.pptx

PDF

Amortization Mathematics of Investment.pptx.pdf Similar to Amortization Schedules_BusinessMath.pptx

PPTX

Amortizing Loan | Finance

PDF

Static Amortization Schedule

PPTX

PDF

Dynamic Amortization Schedule

PPTX

Simple and compound interest.dkldfkfipptx

PPTX

Simple and compound interesmmmmmmmt.pptx

PPTX

PDF

Amortización y Fondos de Amortización.

PPTX

General Mathematics. This presentation is about Loans

PPTX

General.Mathematics_Simple_Interest.pptx

PPTX

basic concepts of consumer loan.....pptx

PPT

PPTX

businessmath-24091qqqqqqqqqq8035709-be4dc68f.pptx

PPT

Lesson: Amortization and Sinking Fund.ppt

PPTX

PPTX

SIMPLE AND COMPOUND INTEREST PPT _20250505_130310_0000_115307.pptx

PPTX

SIMPLE AND COMPOUND INTEREST PPT _20250505_130310_0000_115307.pptx

PPT

PPTX

Bus math lesson 6 interest

PPTX

9A.-SIMPLE-INTEREST-MATH-OF-FINANCE-with-exercises.pptx More from MarkVincentDoria

PPTX

Profit and Loss for Business Mathematics.pptx

PPTX

Ordinary_Annuities_Annuity_Due for BM.pptx

PPTX

fin_alg__-_section_3.6 - Advanced Algebra.pptx

PPT

business_math_powerpoint-Salary and Wages.ppt

PPTX

Compound Interest for business mathematics.pptx

PPT

Quadrilaterals: trapezoids and kites.ppt

PPT

Volume: Prisms and Cylinders for Grade 7

PPTX

CITIZENSHIP TRAINING PROGRAM for Grade 10.pptx

PPT

Graphical Method-Quadratic Equations.ppt

PPT

Solving Fractional Equations - Quadratic.ppt

PPTX

Commission and Sales-Salary and Wages.pptx ![Introduction to rational and irrational numbers [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/introductiontorationalandirrationalnumbersautosaved-241126012733-bd01ba7a-thumbnail.jpg?width=640&height=640&fit=bounds)

PPT

Introduction to rational and irrational numbers [Autosaved].ppt

PPT

rationalnumbers-operations in solving rational numbers.ppt

PPT

Chapter 3 polygons for Mathematics 7.ppt

PPT

INTEREST: Simple and Compound Interest.ppt

PPT

2nd Quarter Review Quiz.ppt Recently uploaded

PDF

BÀI GIẢNG POWERPOINT CHÍNH KHÓA PHIÊN BẢN AI TIẾNG ANH 6 CẢ NĂM, THEO TỪNG BÀ...

PPTX

Palta Utsav Open to All Quiz Final Set.pptx

PPTX

ANTISEPTICS AND DISINFECTANTS CHAPTER NO.05.pptx

PPTX

Report for Prepare Time Management in Odoo 19 POS

PPTX

OXYGEN ADMINISTRATION/THERAPY ......pptx

PPTX

Introduction of Carbohydrates - Dr.M.Jothimuniyandi

PPTX

Redox Titration - Oxidation and Reduction

PPTX

Nanomaterials and its types - Dr.M.Jothimuniyandi

PPTX

Ethiopian soil types , degradation and conservation

PPTX

VAGINAL IRRIGATION..................pptx

PPTX

How to Add or Remove Multiple Followers in a Records

PDF

Caribbean Examinations Council Literacy and Numeracy Standards

PPTX

ANTI-TUSSIVE CHAPTER NO.05 PHARMACOGNOSY

PPTX

ART aPPRECIATION - Lesson 1 AND 2 COVERAGE

PPTX

STERILITY INDICATOR Pharmaceutical microbiology

PDF

Experiment No. 2 To synthesis and submit chlorobutanol.

PPTX

When UDL is no longer enough: Examining post-UDL reflections on inclusive des...

PDF

Freshman Geography Chapter 7-Population of Ethiiopia

PDF

Fanatics of LDM a Time Capsule By LDMMIA

PPTX

Sci8-Q3-W29-Tides_Science 8 Matatag.pptx Amortization Schedules_BusinessMath.pptx

- 1.

- 2.

Learning Objectives

• Understandwhat amortization means

• Learn amortization formulas

• Apply amortization in real-life Filipino business

contexts

• Compute loan payments and schedules

- 3.

- 4.

Key Terms

• Principal– Original loan amount

• Interest – Cost of borrowing

• Term – Loan duration

• Payment – Regular installment amount

- 5.

Amortization Formula

• A= P × [i(1+i)^n] / [(1+i)^n – 1]

• A = payment per period

• P = principal, i = interest rate per period, n =

number of periods

- 6.

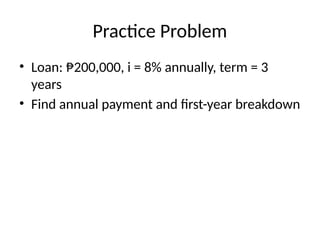

Example: Loan Payment

•P = ₱500,000, i = 10% annually, term = 5 years

(annual payment)

• A = 500,000 × [0.10(1.10)^5] / [(1.10)^5 – 1]

• A = ₱131,366.27

- 7.

- 8.

- 9.

Full 5-Year Table

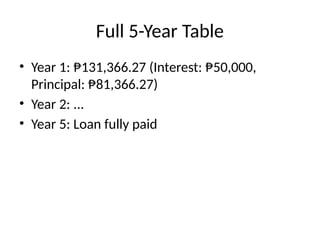

•Year 1: ₱131,366.27 (Interest: ₱50,000,

Principal: ₱81,366.27)

• Year 2: ...

• Year 5: Loan fully paid

- 10.

- 11.

- 12.

Monthly vs AnnualPayments

• Monthly: Smaller payment, more frequent

• Annual: Larger payment, less frequent

- 13.

- 14.

- 15.

- 16.

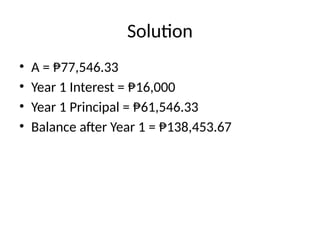

Solution

• A =₱77,546.33

• Year 1 Interest = ₱16,000

• Year 1 Principal = ₱61,546.33

• Balance after Year 1 = ₱138,453.67

- 17.

- 18.

Common Mistakes

• Notconverting interest rate properly

• Mixing monthly and annual rates

• Rounding errors

- 19.

- 20.

Thank You /Q&A

• Any questions?

• Share a personal loan example for discussion

Editor's Notes

- #1 Introduce amortization topic, explaining its importance in finance and loans.

- #2 Outline the goals for the lesson.

- #3 Give examples: housing loan, car loan, business loan.

- #4 Define and explain each term.

- #5 Explain how each variable affects payment calculation.

- #6 Solve step-by-step.

- #7 Explain why it's important to understand payment distribution.

- #8 Show how to get interest and principal for the first year.

- #9 Encourage students to practice completing the table.

- #10 Relate amortization to real-life Filipino scenarios.

- #11 Discuss how each factor changes the payment.

- #12 Compare pros and cons for borrowers.

- #13 Encourage students to see benefits of prepayments.

- #14 Connect amortization to business growth strategies.

- #15 Let students solve individually or in pairs.

- #16 Explain step-by-step solution.

- #17 Show quick calculation options.

- #18 Warn students about frequent calculation errors.

- #19 Summarize major points learned.

- #20 Invite questions and class participation.

![Amortization Formula

• A = P × [i(1+i)^n] / [(1+i)^n – 1]

• A = payment per period

• P = principal, i = interest rate per period, n =

number of periods](https://image.slidesharecdn.com/amortizationbusinessmath-250919030650-760bc22d/85/Amortization-Schedules_BusinessMath-pptx-5-320.jpg)

![Example: Loan Payment

• P = ₱500,000, i = 10% annually, term = 5 years

(annual payment)

• A = 500,000 × [0.10(1.10)^5] / [(1.10)^5 – 1]

• A = ₱131,366.27](https://image.slidesharecdn.com/amortizationbusinessmath-250919030650-760bc22d/85/Amortization-Schedules_BusinessMath-pptx-6-320.jpg)