Download to read offline

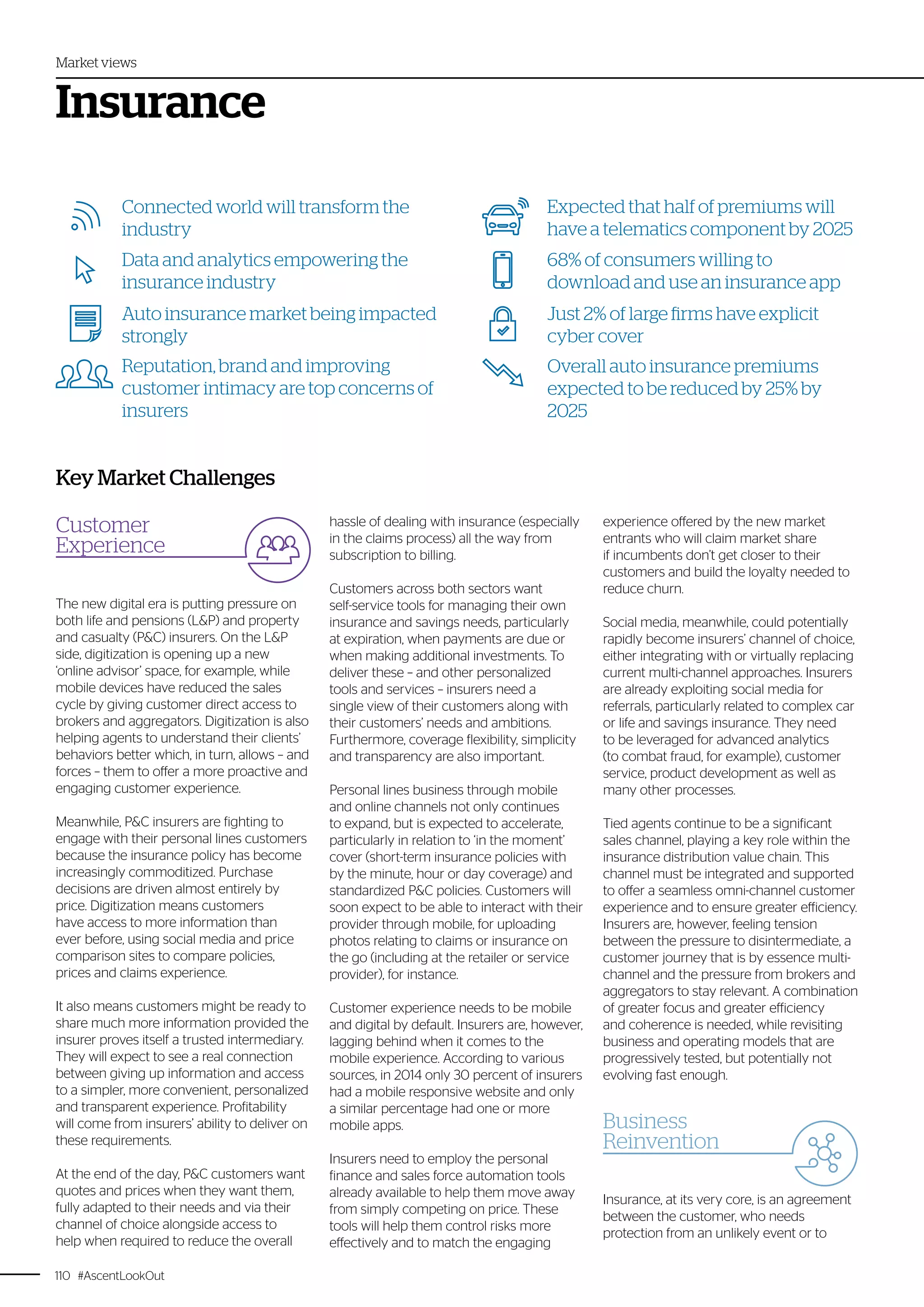

The document discusses how digitization is transforming the insurance industry. It is putting pressure on life/pensions and property/casualty insurers to improve customer experience through digital channels. Customers now expect seamless, personalized experiences through mobile and online access. Insurers need to leverage new technologies like analytics, cloud computing, and the internet of things to meet these rising expectations and compete in the digital era. Data and digitization offer opportunities to better understand customers, price policies dynamically, and automate processes, but insurers must also address challenges of security, regulation and building customer trust.