Download to read offline

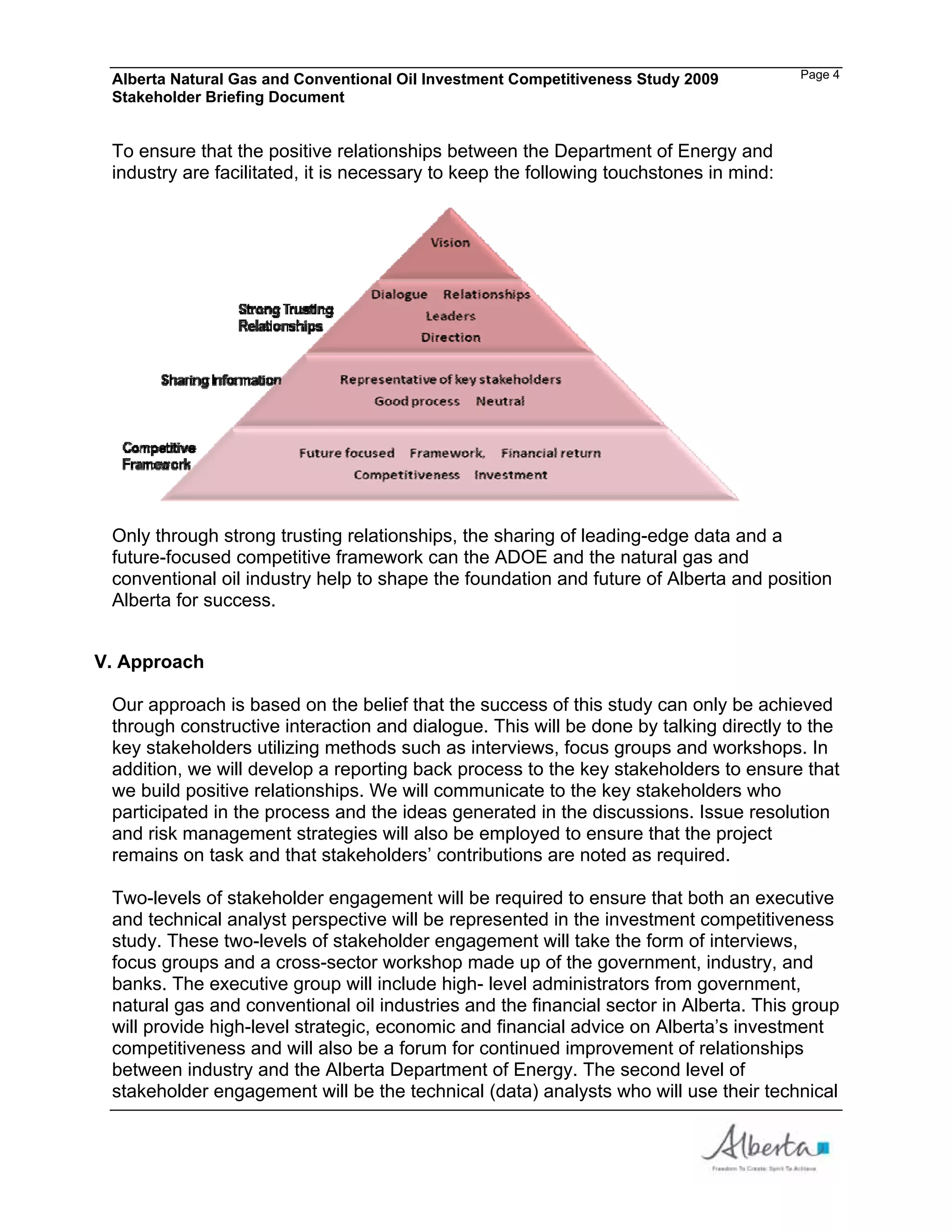

The document summarizes an investment competitiveness study being conducted by the Alberta Department of Energy regarding Alberta's natural gas and conventional oil sectors. The study aims to establish a common understanding of resource economics between the Department and industry stakeholders, and determine what regulatory and fiscal framework is needed to ensure the sectors remain competitive and profitable into the future. A multi-level stakeholder engagement process will be used, involving both executive-level administrators and technical analysts from government, industry and financial institutions. The goal is to facilitate constructive dialogue and maintain positive relationships between stakeholders.

![[Smart Grid Market Research] APEC Tariffs & Renewables - Zpryme Smart Grid In...](https://cdn.slidesharecdn.com/ss_thumbnails/apectariffsandrenewablesoctober2012zprymesmartgridinsightsstandard1-121126203102-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)