Advance tax - Who should pay and when? | CA Sana Baqai

•

0 likes•63 views

A brief note on the advance tax liability under the Indian Income Tax Act. Find out, who is liable to pay advance tax and who is excluded from that category? When to pay the advance tax? And what are the consequences for non-payment of advance tax.

Report

Share

Report

Share

Download to read offline

Recommended

Income tax slabs 2018 19

Here are the income tax rates for financial year 2018-19 for individuals, Hindu undivided family, association of persons, body of individuals, artificial juridical person post Union Budget 2018.

Filing of income tax return for financial year 2017

Filing of income tax return for the 2017-18 financial year is approaching, with the deadline of July 31st for individuals not requiring a tax audit, and September 30th for those that do. Anyone with over 250,000 rupees in taxable income must file a return. Tax audits are mandatory for businesses over 1 crore rupees in sales and professionals over 50 lakhs in receipts. Returns can be filed online or physically, and different forms apply based on income level and sources. Advance tax is due quarterly for those forecasting over 10,000 rupees in tax, and rates range from 5-30% depending on income level with exemptions for seniors.

To go report

This document provides instructions for using a tax optimization tool. It states that a taxpayer must be selected before downloading or uploading any files. The user is instructed to download an input sheet, fill it with accurate tax data, and then upload the completed sheet to have a tax expert prepare an optimized tax return using the tool.

I taxes ( a y 2009-10)

The document discusses the steps to calculate income tax in India. It explains that there are three steps: 1) identify all sources of income, 2) identify applicable deductions, 3) apply the relevant tax slab based on gender and age after deductions. It then provides the tax slabs for resident individuals below 65 years old, resident women below 65, and resident senior citizens. The slabs show the tax-free income amounts and tax rates for portions of income above those amounts.

Income tax slab for fy 2013 14

The document outlines the income tax slabs and rates for the fiscal year 2013-2014, including no changes from the previous year's rates. It provides details on a rebate of Rs. 2000 for individuals with total income up to Rs. 5 lakh. Tables are included showing the income tax slabs and rates for various categories including senior citizens, women, and others.

Income tax rates slabs

income tax slabs for last ten years. to file income tax return of the financial year. you have to see the income tax slabs for assessment year. income tax slab 2011-12. income tax rates 2010-11, income tax slabs 2009-10.

basic of taxes

This document outlines the various types of taxes in India including direct and indirect taxes. Direct taxes include income tax and wealth tax, with income tax rates varying based on taxpayer type (individual, HUF, firm, local authority, or company). Indirect taxes include excise duty, custom duty, central sales tax, value added tax, and service tax. The document also provides details on income tax slabs and rates for individuals of different ages, sources of income, special features of income tax law, recent amendments, and income computation and disclosure standards.

Heads of Income and Return Filing

The document provides an overview of income tax and return filing in India. It defines income tax as a tax charged by the Central Government on income under the Income Tax Act of 1961. Incomes are taxed under five heads: salary, house property, business/profession, capital gains, and other sources. The document outlines the tax rates for individuals, HUFs, companies, and partnership firms. It also lists the different forms used for filing returns depending on the type of assessee and income. In the end, the author provides his contact details and thanks participants for their patience.

Recommended

Income tax slabs 2018 19

Here are the income tax rates for financial year 2018-19 for individuals, Hindu undivided family, association of persons, body of individuals, artificial juridical person post Union Budget 2018.

Filing of income tax return for financial year 2017

Filing of income tax return for the 2017-18 financial year is approaching, with the deadline of July 31st for individuals not requiring a tax audit, and September 30th for those that do. Anyone with over 250,000 rupees in taxable income must file a return. Tax audits are mandatory for businesses over 1 crore rupees in sales and professionals over 50 lakhs in receipts. Returns can be filed online or physically, and different forms apply based on income level and sources. Advance tax is due quarterly for those forecasting over 10,000 rupees in tax, and rates range from 5-30% depending on income level with exemptions for seniors.

To go report

This document provides instructions for using a tax optimization tool. It states that a taxpayer must be selected before downloading or uploading any files. The user is instructed to download an input sheet, fill it with accurate tax data, and then upload the completed sheet to have a tax expert prepare an optimized tax return using the tool.

I taxes ( a y 2009-10)

The document discusses the steps to calculate income tax in India. It explains that there are three steps: 1) identify all sources of income, 2) identify applicable deductions, 3) apply the relevant tax slab based on gender and age after deductions. It then provides the tax slabs for resident individuals below 65 years old, resident women below 65, and resident senior citizens. The slabs show the tax-free income amounts and tax rates for portions of income above those amounts.

Income tax slab for fy 2013 14

The document outlines the income tax slabs and rates for the fiscal year 2013-2014, including no changes from the previous year's rates. It provides details on a rebate of Rs. 2000 for individuals with total income up to Rs. 5 lakh. Tables are included showing the income tax slabs and rates for various categories including senior citizens, women, and others.

Income tax rates slabs

income tax slabs for last ten years. to file income tax return of the financial year. you have to see the income tax slabs for assessment year. income tax slab 2011-12. income tax rates 2010-11, income tax slabs 2009-10.

basic of taxes

This document outlines the various types of taxes in India including direct and indirect taxes. Direct taxes include income tax and wealth tax, with income tax rates varying based on taxpayer type (individual, HUF, firm, local authority, or company). Indirect taxes include excise duty, custom duty, central sales tax, value added tax, and service tax. The document also provides details on income tax slabs and rates for individuals of different ages, sources of income, special features of income tax law, recent amendments, and income computation and disclosure standards.

Heads of Income and Return Filing

The document provides an overview of income tax and return filing in India. It defines income tax as a tax charged by the Central Government on income under the Income Tax Act of 1961. Incomes are taxed under five heads: salary, house property, business/profession, capital gains, and other sources. The document outlines the tax rates for individuals, HUFs, companies, and partnership firms. It also lists the different forms used for filing returns depending on the type of assessee and income. In the end, the author provides his contact details and thanks participants for their patience.

Income Tax avoiding Factors

Assignment on Factor affecting avoidance of Income Tax in Bangladesh

Tax experience in practical life

How pay tax

Recent Tax payment system

Problem Face in paying Tax

Recommendation

Comparison of tax slabs

This document outlines the normal tax rates in India from the 2008-2009 to 2012-2013 financial years for individuals based on their income level, gender, and age. It shows the tax rate and income thresholds for nil, 10%, 20%, and 30% tax brackets. Key details include higher nil tax thresholds for women under 65 and senior citizens aged 60-80 or over 80 years old compared to normal rates. The tax for an individual earning 10 lakh rupees is also provided for each financial year.

Presentation on tax office in dhangadhi,kailali

This document provides an overview of taxation in Nepal. It discusses the introduction and types of taxes, the purpose of collecting taxes, tax rates from different sources over recent years, Permanent Account Numbers (PAN), VAT registration requirements, VAT return filing deadlines and penalties, and how the tax office investigates potential tax evasion. The overall aim of taxation is to finance government expenditures and public services.

Last 25 years income tax rates

This document outlines the income tax rates in India from 1992-1993 to 2013-2014. It provides the tax rates for different income slabs for individuals, HUFs, AOPs and BOIs over these years. The tax rates varied from 0% to 50% depending on the income slab and year. Surcharge and education cess were also introduced in some years applicable above certain income thresholds.

Australian Indirect Tax Snapshot

The document summarizes key aspects of Australia's indirect tax system including:

- The goods and services tax (GST) rate is 10% and applies to most goods and services, while some items like financial supplies and residential rent are input taxed and health and education are GST free.

- The GST registration threshold is AUD $75,000 in annual turnover including overseas suppliers, and $150,000 for charities.

- Other indirect taxes include payroll tax, land tax, stamp duty, fringe benefits tax, and customs duties on cigarettes, alcohol, luxury cars and fuel.

- Special tax concessions are available for research and development as well as technology investors.

Income tax slab

The document provides income tax rates and slabs for individuals, HUFs, BOIs, AOPs, firms, partnerships, companies, foreign companies and cooperative societies in India from assessment years 2001-02 to 2011-12. It lists the tax rates and applicable slabs based on the amount of total income for each category for each assessment year. The rates have varied over the years with some categories like senior citizens and very senior citizens having lower or no tax rates for certain income slabs. Surcharge and education cess are also mentioned where applicable for incomes exceeding certain thresholds.

Tax Planning for the Rich_June 2013

A Seminar Conducted by Akash Mahagaonkar, Head - Operations & Business Development, Relativity Management Solutions India Private Limited on How to Save Tax when your Income exceeds Rs.50 Lakhs & Above.

Lesson 16 advanced tax

This document discusses advance tax in India. Advance tax must be paid if tax liability is Rs. 5,000 or more. It is paid in installments throughout the previous year by both corporate and non-corporate assessees. For non-corporate assessees, installments are due on September 15, December 15, and March 15. For corporate assessees, installments are due on June 15, September 15, December 15, and March 15. Advance tax aims to collect tax revenue earlier and is also known as the "pay as you earn" scheme since tax is paid as income is earned in the previous year.

Adv.tax

This document discusses advance tax in India. [1] Advance tax must be paid if tax liability is Rs. 5,000 or more. [2] It is paid in installments throughout the previous year by both corporate and non-corporate assessees. [3] The first installment is due on June 15 for corporates and September 15 for non-corporates, with subsequent installments due on December 15 and March 15, increasing to 100% of estimated tax due.

Income Tax in India.pdf

Income Tax in India, Income taxes are a source of revenue for governments. They are used to fund public services, pay government obligations, and provide goods for citizens.

The first Income-tax Act in India was introduced in 1860 on account of financial stress owing to the mutiny of 1857 and was to be in force for a period of 5 years.

The Income Tax Act 1961 has been brought into force on 1 April 1962. It applies to the whole of India (including Jammu and Kashmir).

An Income Tax in India is a direct tax that a government imposes on the annual income and profits earned by individuals and entities. It is calculated on the net taxable income of a person or entity for the applicable financial/fiscal year, which starts from the 1st of April of a year and ends on the 31st of March of the next calendar year.

Guide to Singapore Tax 2016

1. The document provides a quick guide to Singapore corporate and individual tax laws for 2016. It summarizes Singapore's tax residency rules, tax rates, tax returns and assessments processes for both companies and individuals. For companies, the corporate tax rate is 17% and qualifying newly incorporated companies may receive tax exemptions on a portion of their chargeable income for their first three years. For individuals, tax rates are progressive up to 22% for residents and generally 22% for non-residents.

Tax due date compliance calendar

This document provides information on various tax due dates in India, including for income tax, service tax, VAT, advance tax, and tax deducted at source (TDS). It also outlines the annual and event-based compliance requirements for limited liability partnerships (LLPs) registered in India.

Advance Tax (2).pptx

The document discusses advance tax payments in India. It explains that advance tax is income tax paid in installments over the course of a fiscal year, rather than in a lump sum at year-end. Those with a total annual tax liability over Rs. 10,000 must pay advance tax. Due dates for installments are June 15th, September 15th, December 15th, and March 15th, in percentages of 15%, 45%, 75%, and 100% respectively. Failure to meet installment amounts on time will result in late payment interest of 1% per month on the unpaid amount. The document also provides an example calculation of advance tax payments for an individual.

Advance tax

Advance tax must be paid by all individuals whose tax liability is Rs. 5,000 or more. It is paid in installments throughout the previous year to estimate taxes owed on income earned that year. For non-corporate taxpayers, installments are due on September 15 (30% of taxes), December 15 (60%), and March 15 (100%). Corporate taxpayers' installments are due on June 15 (15%), September 15 (30%), December 15 (60%), and March 15 (100%). The advance tax system, also called "pay as you earn," collects taxes concurrently with income to fund government operations on an ongoing basis.

Income tax

Income tax is imposed on individuals according to their income level through a progressive tax system. The assessment year is the financial year during which a person's income from the previous year is assessed for taxation. Various types of incomes are categorized under different heads and then aggregated to determine the gross total income, from which deductions can be claimed to arrive at the total taxable income. An individual's residential status determines whether their global income is taxable in India.

Free-Income-Tax-Guide.pdf

Here are the steps to calculate income tax for the given total incomes:

1. Total income of Rs. 2,88,000:

- Income up to Rs. 2,50,000 is tax exempt

- Taxable income = Rs. 2,88,000 - Rs. 2,50,000 = Rs. 38,000

- Tax on Rs. 38,000 at 5% slab = Rs. 1,900

- Add education cess @ 4% of Rs. 1,900 = Rs. 76

- Total tax payable = Rs. 1,900 + Rs. 76 = Rs. 1,976

2. Total income of Rs. 7,00,000

- Income up

All about Advance Tax in India - With Calculation

Advance tax is the tax payable on total income of the year earned from different sources including salary, business, profession, rent, etc.

Taxation of individuals in singapore

Objectives & Agenda :

To understand basics of income tax like what is taxable/ non taxable income, residential status, Personal Income tax rates etc. The webinar shall dwell upon other aspects like threshold limit for filing Personal Income tax returns, consequence of not filing/ late filing of returns due dates for filing return and various deductions/reliefs available to individuals. Further it would also provide insights on taxation of overseas income in Singapore.

Benefits of filing Income Tax

In India, every assessee whether having a taxable income or not, should definitely file their income tax return. Why? This PPT will tell you why!

Income Tax Fundamental Concepts

Under Fundamental Concepts of Income Tax Presentation, Important Definitions under Income Tax Act, Residential Status of the assesses & its tax incidence is covered.

S 2-Invoicing rules under GST

This document discusses various types of documents that can be issued under the GST Act, including invoices, vouchers, debit notes, credit notes, and delivery challans. It provides details on the purpose and required contents of each type of document. It specifies the timelines for issuing invoices and vouchers and clarifies when revised invoices or consolidated invoices would be required. The document aims to help registered persons understand their documentation obligations under the GST Act.

G.K Kedia.pptx

G. K. Kedia & Co. is a Delhi based CA Firm, which has a robust team of skilled and proficient Chartered Accountants, who can handle all financial services related to Income Tax, Goods & Services Tax (GST), Merger & Acquisitions, Due Diligence Services, Trademarks, Investment in India by Foreign Nationals & NRIs, Societies and Trust (NGO), Import-Export, Technology Park & Special Economic Zone, Business Process Outsource (BPO),

More Related Content

What's hot

Income Tax avoiding Factors

Assignment on Factor affecting avoidance of Income Tax in Bangladesh

Tax experience in practical life

How pay tax

Recent Tax payment system

Problem Face in paying Tax

Recommendation

Comparison of tax slabs

This document outlines the normal tax rates in India from the 2008-2009 to 2012-2013 financial years for individuals based on their income level, gender, and age. It shows the tax rate and income thresholds for nil, 10%, 20%, and 30% tax brackets. Key details include higher nil tax thresholds for women under 65 and senior citizens aged 60-80 or over 80 years old compared to normal rates. The tax for an individual earning 10 lakh rupees is also provided for each financial year.

Presentation on tax office in dhangadhi,kailali

This document provides an overview of taxation in Nepal. It discusses the introduction and types of taxes, the purpose of collecting taxes, tax rates from different sources over recent years, Permanent Account Numbers (PAN), VAT registration requirements, VAT return filing deadlines and penalties, and how the tax office investigates potential tax evasion. The overall aim of taxation is to finance government expenditures and public services.

Last 25 years income tax rates

This document outlines the income tax rates in India from 1992-1993 to 2013-2014. It provides the tax rates for different income slabs for individuals, HUFs, AOPs and BOIs over these years. The tax rates varied from 0% to 50% depending on the income slab and year. Surcharge and education cess were also introduced in some years applicable above certain income thresholds.

Australian Indirect Tax Snapshot

The document summarizes key aspects of Australia's indirect tax system including:

- The goods and services tax (GST) rate is 10% and applies to most goods and services, while some items like financial supplies and residential rent are input taxed and health and education are GST free.

- The GST registration threshold is AUD $75,000 in annual turnover including overseas suppliers, and $150,000 for charities.

- Other indirect taxes include payroll tax, land tax, stamp duty, fringe benefits tax, and customs duties on cigarettes, alcohol, luxury cars and fuel.

- Special tax concessions are available for research and development as well as technology investors.

Income tax slab

The document provides income tax rates and slabs for individuals, HUFs, BOIs, AOPs, firms, partnerships, companies, foreign companies and cooperative societies in India from assessment years 2001-02 to 2011-12. It lists the tax rates and applicable slabs based on the amount of total income for each category for each assessment year. The rates have varied over the years with some categories like senior citizens and very senior citizens having lower or no tax rates for certain income slabs. Surcharge and education cess are also mentioned where applicable for incomes exceeding certain thresholds.

Tax Planning for the Rich_June 2013

A Seminar Conducted by Akash Mahagaonkar, Head - Operations & Business Development, Relativity Management Solutions India Private Limited on How to Save Tax when your Income exceeds Rs.50 Lakhs & Above.

What's hot (7)

Similar to Advance tax - Who should pay and when? | CA Sana Baqai

Lesson 16 advanced tax

This document discusses advance tax in India. Advance tax must be paid if tax liability is Rs. 5,000 or more. It is paid in installments throughout the previous year by both corporate and non-corporate assessees. For non-corporate assessees, installments are due on September 15, December 15, and March 15. For corporate assessees, installments are due on June 15, September 15, December 15, and March 15. Advance tax aims to collect tax revenue earlier and is also known as the "pay as you earn" scheme since tax is paid as income is earned in the previous year.

Adv.tax

This document discusses advance tax in India. [1] Advance tax must be paid if tax liability is Rs. 5,000 or more. [2] It is paid in installments throughout the previous year by both corporate and non-corporate assessees. [3] The first installment is due on June 15 for corporates and September 15 for non-corporates, with subsequent installments due on December 15 and March 15, increasing to 100% of estimated tax due.

Income Tax in India.pdf

Income Tax in India, Income taxes are a source of revenue for governments. They are used to fund public services, pay government obligations, and provide goods for citizens.

The first Income-tax Act in India was introduced in 1860 on account of financial stress owing to the mutiny of 1857 and was to be in force for a period of 5 years.

The Income Tax Act 1961 has been brought into force on 1 April 1962. It applies to the whole of India (including Jammu and Kashmir).

An Income Tax in India is a direct tax that a government imposes on the annual income and profits earned by individuals and entities. It is calculated on the net taxable income of a person or entity for the applicable financial/fiscal year, which starts from the 1st of April of a year and ends on the 31st of March of the next calendar year.

Guide to Singapore Tax 2016

1. The document provides a quick guide to Singapore corporate and individual tax laws for 2016. It summarizes Singapore's tax residency rules, tax rates, tax returns and assessments processes for both companies and individuals. For companies, the corporate tax rate is 17% and qualifying newly incorporated companies may receive tax exemptions on a portion of their chargeable income for their first three years. For individuals, tax rates are progressive up to 22% for residents and generally 22% for non-residents.

Tax due date compliance calendar

This document provides information on various tax due dates in India, including for income tax, service tax, VAT, advance tax, and tax deducted at source (TDS). It also outlines the annual and event-based compliance requirements for limited liability partnerships (LLPs) registered in India.

Advance Tax (2).pptx

The document discusses advance tax payments in India. It explains that advance tax is income tax paid in installments over the course of a fiscal year, rather than in a lump sum at year-end. Those with a total annual tax liability over Rs. 10,000 must pay advance tax. Due dates for installments are June 15th, September 15th, December 15th, and March 15th, in percentages of 15%, 45%, 75%, and 100% respectively. Failure to meet installment amounts on time will result in late payment interest of 1% per month on the unpaid amount. The document also provides an example calculation of advance tax payments for an individual.

Advance tax

Advance tax must be paid by all individuals whose tax liability is Rs. 5,000 or more. It is paid in installments throughout the previous year to estimate taxes owed on income earned that year. For non-corporate taxpayers, installments are due on September 15 (30% of taxes), December 15 (60%), and March 15 (100%). Corporate taxpayers' installments are due on June 15 (15%), September 15 (30%), December 15 (60%), and March 15 (100%). The advance tax system, also called "pay as you earn," collects taxes concurrently with income to fund government operations on an ongoing basis.

Income tax

Income tax is imposed on individuals according to their income level through a progressive tax system. The assessment year is the financial year during which a person's income from the previous year is assessed for taxation. Various types of incomes are categorized under different heads and then aggregated to determine the gross total income, from which deductions can be claimed to arrive at the total taxable income. An individual's residential status determines whether their global income is taxable in India.

Free-Income-Tax-Guide.pdf

Here are the steps to calculate income tax for the given total incomes:

1. Total income of Rs. 2,88,000:

- Income up to Rs. 2,50,000 is tax exempt

- Taxable income = Rs. 2,88,000 - Rs. 2,50,000 = Rs. 38,000

- Tax on Rs. 38,000 at 5% slab = Rs. 1,900

- Add education cess @ 4% of Rs. 1,900 = Rs. 76

- Total tax payable = Rs. 1,900 + Rs. 76 = Rs. 1,976

2. Total income of Rs. 7,00,000

- Income up

All about Advance Tax in India - With Calculation

Advance tax is the tax payable on total income of the year earned from different sources including salary, business, profession, rent, etc.

Taxation of individuals in singapore

Objectives & Agenda :

To understand basics of income tax like what is taxable/ non taxable income, residential status, Personal Income tax rates etc. The webinar shall dwell upon other aspects like threshold limit for filing Personal Income tax returns, consequence of not filing/ late filing of returns due dates for filing return and various deductions/reliefs available to individuals. Further it would also provide insights on taxation of overseas income in Singapore.

Benefits of filing Income Tax

In India, every assessee whether having a taxable income or not, should definitely file their income tax return. Why? This PPT will tell you why!

Income Tax Fundamental Concepts

Under Fundamental Concepts of Income Tax Presentation, Important Definitions under Income Tax Act, Residential Status of the assesses & its tax incidence is covered.

S 2-Invoicing rules under GST

This document discusses various types of documents that can be issued under the GST Act, including invoices, vouchers, debit notes, credit notes, and delivery challans. It provides details on the purpose and required contents of each type of document. It specifies the timelines for issuing invoices and vouchers and clarifies when revised invoices or consolidated invoices would be required. The document aims to help registered persons understand their documentation obligations under the GST Act.

G.K Kedia.pptx

G. K. Kedia & Co. is a Delhi based CA Firm, which has a robust team of skilled and proficient Chartered Accountants, who can handle all financial services related to Income Tax, Goods & Services Tax (GST), Merger & Acquisitions, Due Diligence Services, Trademarks, Investment in India by Foreign Nationals & NRIs, Societies and Trust (NGO), Import-Export, Technology Park & Special Economic Zone, Business Process Outsource (BPO),

Income year,Tax year & tax Rate of Bangladesh

The document provides information about income year, assessment year, tax rates, and tax identification numbers (TIN) in Bangladesh. It defines assessment year as the year in which tax is paid, and income year as the year to which the income being taxed refers. It explains that the income year and assessment year can be the same or different depending on the type of taxpayer. The document also outlines Bangladesh's minimum taxable income limits, general tax rates, and surcharges on income tax based on asset levels. It provides details about 12-digit TINs, including how they are issued and required uses.

Income Tax for New Tax Return Filers- FAQs.pptx

This article provides a detailed overview of income tax, including its definition, the administrative framework, return filing period, who is liable to pay tax, how to pay tax, precautions in tax payment, advance tax calculation, income tax challans, Form 26AS, exempt income, taxable income, maintaining books of account, professions, and the period for which records should be kept. It also covers topics such as revenue receipts, capital receipts, agricultural income, and relief from double taxation.

INCOME TAX ASSESSMENT - Copy.pptx

The document discusses various aspects of income tax in India including income tax, advance tax, assessment, returns and related topics. Some key points:

1. Income tax is a direct tax charged by the central government on the annual income of individuals and businesses. It is calculated based on tax slabs defined by the Income Tax Department.

2. Advance tax is a method of collecting tax in advance throughout the year in the form of installments to match the taxpayer's estimated annual liability.

3. There are different types of income tax assessments including self-assessment, summary assessment, scrutiny assessment, best judgement assessment, and income escaping assessment. Faceless assessment is now conducted electronically without any physical interface between the taxpayer

Tax Deduction at Source (TDS).pptx

The document discusses Tax Deduction at Source (TDS) in India. Some key points:

- TDS is a system where the payer of certain types of payments like salary, rent, interest, etc. is required to deduct a percentage of tax from the payment amount.

- Common deductions include interest, commission, rent, salary. The deducted amount is paid to the government on behalf of the recipient.

- TDS rates vary based on the type of income and thresholds. For example, interest income above ₹40,000 is taxed at 10%.

- Form 26AS issued by the employer/payer shows the TDS deducted from salary payments.

Assessment procedure 1

This document provides an overview of key concepts related to income tax assessment in India, including:

- Definitions of basic terms like assessee, assessment year, and previous year.

- Explanations of the assessment process and roles of the assessing officer.

- Details on tax rates for individuals and corporations.

- Formats for computing total income and tax liability.

- Due dates for filing income tax returns in different forms.

- The types of assessments including self-assessment, summary assessment, and reassessment.

- Procedures for notices of demand and penalties.

Similar to Advance tax - Who should pay and when? | CA Sana Baqai (20)

More from Sana Baqai

Powerful Audit Report Writing

The document discusses best practices for writing powerful internal audit reports. It emphasizes the importance of clear and concise communication through the use of plain language and visual aids. It provides tips for different sections of an audit report including the executive summary, findings, conclusions, and recommendations. The document also outlines dos and don'ts for effective report writing such as following the five C's framework, emphasizing potential improvements, and obtaining stakeholder feedback.

Start-up Trends Post Pandemic

The document discusses start-up trends that are likely to grow after the COVID-19 pandemic. Some sectors that are expected to grow include ed-tech, health and wellness, agri-tech, SAAS, e-commerce, and online gaming. It also outlines challenges start-ups faced during the pandemic, such as cash management, changing valuations, leadership complexities, and changing space needs. Finally, it provides tips for start-up survival during the pandemic, including doing reality checks, lending help to customers, caring for employees, communicating often, using time wisely, applying for financing, and looking for new opportunities.

Beyond Box Ticking - Internal Audit & Controls - Companies Act, 2013 Perspect...

As we all know, the Companies Act, 2013 has brought about significant changes to the corporate governance landscape in India. One of the key areas where these changes are being felt is in internal audit and control. It is no longer enough for companies to simply tick the boxes when it comes to internal audit and control. They must go beyond that and ensure that their internal audit and control processes are effective and compliant with the Companies Act, 2013.

The Companies Act, 2013 (CA, 2013) has introduced a number of new requirements for companies in relation to income audit and control. These requirements are designed to improve the accuracy and reliability of financial reporting, and to reduce the risk of fraud and error.

One of the key changes introduced by the CA, 2013 is the requirement for companies to have an internal audit function. The internal audit function is responsible for providing independent assurance to the board of directors on the effectiveness of the company's internal controls over financial reporting.

Networking of CA Firms – ICAI Guidelines

The Council of ICAI issued Network Guidelines for the first time in the year 2005, and thereafter, the same was revised by the Council in the year 2011.

The previous guidelines did not fetch the expected level of enthusiasm from

members, and only close to 100 networks could get registered with ICAI as of date. This threw up the need to review the Guidelines in order to make them more relevant and attractive in terms of the current professional scenario.

It is of paramount importance to enable Indian CA Firms to come together and grow stronger so that they can serve the need of the country as we move to become a $5 trillion economy and also render services in the global market.

Overview of code of ethics – Vol 1 | ICAI | CA Sana Baqai

This contains the overview of code of ethics 2019 vol-1 issued by ICAI. Major changes over 2009 code and the deferred provisions are covered

Effective Tips for Time management – Increase your productivity | CA Sana Baqai

We all have limited time in hand to accomplish the tasks and achieve the goals. Therefore, proper time management is a tool for success. We have to attain the set goals in a specified time frame.

Here are certain tips for time management.

Click here to watch the video - https://youtu.be/lIQWt6Y_TBw

Tips for Making Effective and Powerful PowerPoint Presentation | Sana Baqai

The document provides rules for creating an appealing and powerful presentation. It advises avoiding cluttered slides with too much text or many bullet points. Presenters should not include more than 7 words per line or 7 lines per slide. Slides should emphasize key points through visuals rather than long paragraphs of text and aim to be a visual aid rather than distraction.

Latest Format for Audit Report and Financials for LLP | CA Sana Baqai

Where Turnover of Limited Liability Partnership exceeds Rs. 40 lac or partner’s obligation of contribution exceeds Rs. 25 lakhs then LLP is required to get its books of accounts audited.

On completion of the audit, the auditor issues Audit Report to the partners of LLP. The LLP Audit report contains information about Management responsibility, auditor responsibility & Audit Opinion.

Here is the latest Audit Report and financial statements format for LLP.

Tax Rates for Assessment Year 2021 22 | CA Sana Baqai

For the assessment year 2021-22 i.e. for Financial year 2020-21 the tax rates for individuals, partnership firms, LLP, Indian Companies, Foreign Companies are defined in this document.

The tax rates may vary from year to year and changes in tax rates take place every year through Unio Budget announced by Finance Minister in the month of February.

Permanent Account Number (PAN) Necessity and Uses - Tax Literacy | Sana Baqai

Permanent Account Number, in short PAN, is the unique identification number allotted by Income Tax Department to the person who applies for it.

All about Section 44AD of the Income Tax Act | Sana Baqai

Special provision for computing profits and gains of business on a presumptive basis. Under section 44AD of Income tax Act, small taxpayers with less than Rs. 2 crore of turnover are not required to maintain books of accounts and their profits are presumed to be 8% or 6%, as the case may be, of their turnover.

Agreement for CSR Implementation Partner / Agency / NGO | Sana Baqai

This document contains an agreement between ABC Ltd and XYZ Foundation regarding funding from ABC for XYZ's project "Girls Empowerment through Education".

Key details include:

- ABC will provide Rs. 76 lakhs in funding for the project over 3 years.

- Payments will be made in installments based on progress reports and utilization certificates submitted by XYZ.

- XYZ will implement the project as per the agreed scope and timeline.

- Both parties will adhere to reporting, accounting and auditing requirements to ensure proper use of funds.

- Unspent funds must be refunded by XYZ upon completion of the project.

The agreement outlines the roles and responsibilities of both parties to ensure effective implementation

Highly Effective Tips for Impressive Presentation | Sana Baqai

Making an effective presentation requires good presentation skills & techniques. You will learn tips on how to prepare, how to present and effective use of PPT.

Unique Document Identification Number - Objectives and Benefits | Sana Baqai

What is UDIN? What are the Objectives and Benefits of UDIN? When UDIN has been made mandatory for Chartered Accountants?

Foundation of Internal Auditing | Sana Baqai

It aims to give a basic understanding of the internal audit. Recognize the knowledge, skills, and competencies required to fulfill the responsibilities of the internal audit activity. It also interprets the difference between assurance and consulting services provided by the internal auditor.

Emerging Issues and Challenges | Sana Baqai

The document discusses various topics related to internal auditing including financial accounting and budgeting risks, business challenges, project management, organizational change, fraud risks, forensic accounting, and emerging issues. It provides details on budget variance analysis, internal audit areas of focus, challenges during the pandemic, and comparisons of in-house, outsourcing, and co-sourcing internal audit assignments. Risk management approaches including the COSO framework are outlined. Types of fraud investigations like corruption, asset misappropriation, and financial statement fraud are defined. Emerging issues facing internal auditors related to technology and standards are also noted.

More from Sana Baqai (16)

Beyond Box Ticking - Internal Audit & Controls - Companies Act, 2013 Perspect...

Beyond Box Ticking - Internal Audit & Controls - Companies Act, 2013 Perspect...

Overview of code of ethics – Vol 1 | ICAI | CA Sana Baqai

Overview of code of ethics – Vol 1 | ICAI | CA Sana Baqai

Effective Tips for Time management – Increase your productivity | CA Sana Baqai

Effective Tips for Time management – Increase your productivity | CA Sana Baqai

Tips for Making Effective and Powerful PowerPoint Presentation | Sana Baqai

Tips for Making Effective and Powerful PowerPoint Presentation | Sana Baqai

Latest Format for Audit Report and Financials for LLP | CA Sana Baqai

Latest Format for Audit Report and Financials for LLP | CA Sana Baqai

Tax Rates for Assessment Year 2021 22 | CA Sana Baqai

Tax Rates for Assessment Year 2021 22 | CA Sana Baqai

Permanent Account Number (PAN) Necessity and Uses - Tax Literacy | Sana Baqai

Permanent Account Number (PAN) Necessity and Uses - Tax Literacy | Sana Baqai

All about Section 44AD of the Income Tax Act | Sana Baqai

All about Section 44AD of the Income Tax Act | Sana Baqai

Agreement for CSR Implementation Partner / Agency / NGO | Sana Baqai

Agreement for CSR Implementation Partner / Agency / NGO | Sana Baqai

Highly Effective Tips for Impressive Presentation | Sana Baqai

Highly Effective Tips for Impressive Presentation | Sana Baqai

Unique Document Identification Number - Objectives and Benefits | Sana Baqai

Unique Document Identification Number - Objectives and Benefits | Sana Baqai

Recently uploaded

What's a worker’s market? Job quality and labour market tightness

What's a worker’s market? Job quality and labour market tightnessLabour Market Information Council | Conseil de l’information sur le marché du travail

In a tight labour market, job-seekers gain bargaining power and leverage it into greater job quality—at least, that’s the conventional wisdom.

Michael, LMIC Economist, presented findings that reveal a weakened relationship between labour market tightness and job quality indicators following the pandemic. Labour market tightness coincided with growth in real wages for only a portion of workers: those in low-wage jobs requiring little education. Several factors—including labour market composition, worker and employer behaviour, and labour market practices—have contributed to the absence of worker benefits. These will be investigated further in future work.Discover the Future of Dogecoin with Our Comprehensive Guidance

Learn in-depth about Dogecoin's trajectory and stay informed with 36crypto's essential and up-to-date information about the crypto space.

Our presentation delves into Dogecoin's potential future, exploring whether it's destined to skyrocket to the moon or face a downward spiral. In addition, it highlights invaluable insights. Don't miss out on this opportunity to enhance your crypto understanding!

https://36crypto.com/the-future-of-dogecoin-how-high-can-this-cryptocurrency-reach/

Fabular Frames and the Four Ratio Problem

Digital, interactive art showing the struggle of a society in providing for its present population while also saving planetary resources for future generations. Spread across several frames, the art is actually the rendering of real and speculative data. The stereographic projections change shape in response to prompts and provocations. Visitors interact with the model through speculative statements about how to increase savings across communities, regions, ecosystems and environments. Their fabulations combined with random noise, i.e. factors beyond control, have a dramatic effect on the societal transition. Things get better. Things get worse. The aim is to give visitors a new grasp and feel of the ongoing struggles in democracies around the world.

Stunning art in the small multiples format brings out the spatiotemporal nature of societal transitions, against backdrop issues such as energy, housing, waste, farmland and forest. In each frame we see hopeful and frightful interplays between spending and saving. Problems emerge when one of the two parts of the existential anaglyph rapidly shrinks like Arctic ice, as factors cross thresholds. Ecological wealth and intergenerational equity areFour at stake. Not enough spending could mean economic stress, social unrest and political conflict. Not enough saving and there will be climate breakdown and ‘bankruptcy’. So where does speculative design start and the gambling and betting end? Behind each fabular frame is a four ratio problem. Each ratio reflects the level of sacrifice and self-restraint a society is willing to accept, against promises of prosperity and freedom. Some values seem to stabilise a frame while others cause collapse. Get the ratios right and we can have it all. Get them wrong and things get more desperate.

1:1制作加拿大麦吉尔大学毕业证硕士学历证书原版一模一样

原版一模一样【微信:741003700 】【加拿大麦吉尔大学毕业证硕士学历证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

falcon-invoice-discounting-a-premier-investment-platform-for-superior-returns...

falcon-invoice-discounting-a-premier-investment-platform-for-superior-returns...Falcon Invoice Discounting

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.Economic Risk Factor Update: June 2024 [SlideShare]

May’s reports showed signs of continued economic growth, said Sam Millette, director, fixed income, in his latest Economic Risk Factor Update.

For more market updates, subscribe to The Independent Market Observer at https://blog.commonwealth.com/independent-market-observer.

How to Use Payment Vouchers in Odoo 18.

Every business, big or small, deals with outgoing payments. Whether it’s to suppliers for inventory, to employees for salaries, or to vendors for services rendered, keeping track of these expenses is crucial. This is where payment vouchers come in – the unsung heroes of the accounting world.

一比一原版美国新罕布什尔大学(unh)毕业证学历认证真实可查

永久可查学历认证【微信:A575476】【美国新罕布什尔大学(unh)毕业证成绩单Offer】【微信:A575476】(留信学历认证永久存档查询)采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信:A575476】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信:A575476】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

→ 【关于价格问题(保证一手价格)

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

选择实体注册公司办理,更放心,更安全!我们的承诺:可来公司面谈,可签订合同,会陪同客户一起到教育部认证窗口递交认证材料,客户在教育部官方认证查询网站查询到认证通过结果后付款,不成功不收费!

Independent Study - College of Wooster Research (2023-2024)

"Does Foreign Direct Investment Negatively Affect Preservation of Culture in the Global South? Case Studies in Thailand and Cambodia."

Do elements of globalization, such as Foreign Direct Investment (FDI), negatively affect the ability of countries in the Global South to preserve their culture? This research aims to answer this question by employing a cross-sectional comparative case study analysis utilizing methods of difference. Thailand and Cambodia are compared as they are in the same region and have a similar culture. The metric of difference between Thailand and Cambodia is their ability to preserve their culture. This ability is operationalized by their respective attitudes towards FDI; Thailand imposes stringent regulations and limitations on FDI while Cambodia does not hesitate to accept most FDI and imposes fewer limitations. The evidence from this study suggests that FDI from globally influential countries with high gross domestic products (GDPs) (e.g. China, U.S.) challenges the ability of countries with lower GDPs (e.g. Cambodia) to protect their culture. Furthermore, the ability, or lack thereof, of the receiving countries to protect their culture is amplified by the existence and implementation of restrictive FDI policies imposed by their governments.

My study abroad in Bali, Indonesia, inspired this research topic as I noticed how globalization is changing the culture of its people. I learned their language and way of life which helped me understand the beauty and importance of cultural preservation. I believe we could all benefit from learning new perspectives as they could help us ideate solutions to contemporary issues and empathize with others.

Bridging the gap: Online job postings, survey data and the assessment of job ...

Bridging the gap: Online job postings, survey data and the assessment of job ...Labour Market Information Council | Conseil de l’information sur le marché du travail

OJP data from firms like Vicinity Jobs have emerged as a complement to traditional sources of labour demand data, such as the Job Vacancy and Wages Survey (JVWS). Ibrahim Abuallail, PhD Candidate, University of Ottawa, presented research relating to bias in OJPs and a proposed approach to effectively adjust OJP data to complement existing official data (such as from the JVWS) and improve the measurement of labour demand.Who Is Abhay Bhutada, MD of Poonawalla Fincorp

Abhay Bhutada, the Managing Director of Poonawalla Fincorp Limited, is an accomplished leader with over 15 years of experience in commercial and retail lending. A Qualified Chartered Accountant, he has been pivotal in leveraging technology to enhance financial services. Starting his career at Bank of India, he later founded TAB Capital Limited and co-founded Poonawalla Finance Private Limited, emphasizing digital lending. Under his leadership, Poonawalla Fincorp achieved a 'AAA' credit rating, integrating acquisitions and emphasizing corporate governance. Actively involved in industry forums and CSR initiatives, Abhay has been recognized with awards like "Young Entrepreneur of India 2017" and "40 under 40 Most Influential Leader for 2020-21." Personally, he values mindfulness, enjoys gardening, yoga, and sees every day as an opportunity for growth and improvement.

做澳洲澳大利亚国立大学毕业证荣誉学位证书原版一模一样

原版一模一样【微信:741003700 】【澳洲澳大利亚国立大学毕业证荣誉学位证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

Accounting Information Systems (AIS).pptx

An accounting information system (AIS) refers to tools and systems designed for the collection and display of accounting information so accountants and executives can make informed decisions.

真实可查(nwu毕业证书)美国西北大学毕业证学位证书范本原版一模一样

原版定制【微信:bwp0011】《(nwu毕业证书)美国西北大学毕业证学位证书》【微信:bwp0011】成绩单 、雅思、外壳、留信学历认证永久存档查询,采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信bwp0011】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信bwp0011】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

在线办理(GU毕业证书)美国贡萨加大学毕业证学历证书一模一样

学校原件一模一样【微信:741003700 】《(GU毕业证书)美国贡萨加大学毕业证学历证书》【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

高仿英国伦敦艺术大学毕业证(ual毕业证书)文凭证书原版一模一样

原版一模一样【微信:741003700 】【英国伦敦艺术大学毕业证(ual毕业证书)文凭证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

RMIT University degree offer diploma Transcript

澳洲RMIT毕业证书制作RMIT假文凭定制Q微168899991做RMIT留信网教留服认证海牙认证改RMIT成绩单GPA做RMIT假学位证假文凭高仿毕业证申请墨尔本皇家理工大学RMIT University degree offer diploma Transcript

快速制作美国迈阿密大学牛津分校毕业证文凭证书英文原版一模一样

原版一模一样【微信:741003700 】【美国迈阿密大学牛津分校毕业证文凭证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

How will new technology fields affect economic trade?

Recently uploaded (20)

What's a worker’s market? Job quality and labour market tightness

What's a worker’s market? Job quality and labour market tightness

Discover the Future of Dogecoin with Our Comprehensive Guidance

Discover the Future of Dogecoin with Our Comprehensive Guidance

falcon-invoice-discounting-a-premier-investment-platform-for-superior-returns...

falcon-invoice-discounting-a-premier-investment-platform-for-superior-returns...

Economic Risk Factor Update: June 2024 [SlideShare]

Economic Risk Factor Update: June 2024 [SlideShare]

Independent Study - College of Wooster Research (2023-2024)

Independent Study - College of Wooster Research (2023-2024)

Bridging the gap: Online job postings, survey data and the assessment of job ...

Bridging the gap: Online job postings, survey data and the assessment of job ...

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

Advance tax - Who should pay and when? | CA Sana Baqai

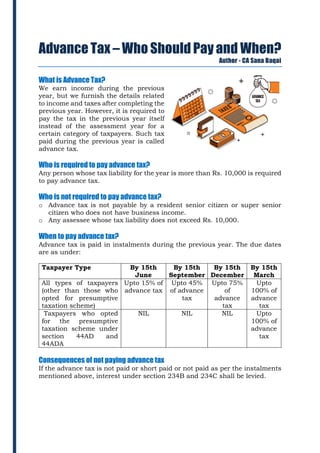

- 1. Advance Tax – Who Should Pay and When? Author - CA Sana Baqai What is Advance Tax? We earn income during the previous year, but we furnish the details related to income and taxes after completing the previous year. However, it is required to pay the tax in the previous year itself instead of the assessment year for a certain category of taxpayers. Such tax paid during the previous year is called advance tax. Who is required to pay advance tax? Any person whose tax liability for the year is more than Rs. 10,000 is required to pay advance tax. Who is not required to pay advance tax? o Advance tax is not payable by a resident senior citizen or super senior citizen who does not have business income. o Any assessee whose tax liability does not exceed Rs. 10,000. When to pay advance tax? Advance tax is paid in instalments during the previous year. The due dates are as under: Taxpayer Type By 15th June By 15th September By 15th December By 15th March All types of taxpayers (other than those who opted for presumptive taxation scheme) Upto 15% of advance tax Upto 45% of advance tax Upto 75% of advance tax Upto 100% of advance tax Taxpayers who opted for the presumptive taxation scheme under section 44AD and 44ADA NIL NIL NIL Upto 100% of advance tax Consequences of not paying advance tax If the advance tax is not paid or short paid or not paid as per the instalments mentioned above, interest under section 234B and 234C shall be levied.