Downloaded 24 times

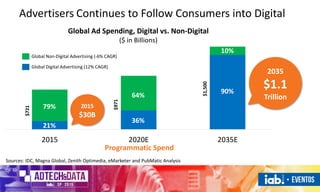

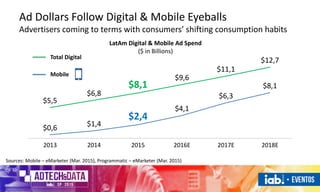

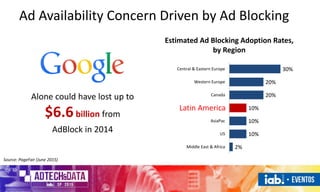

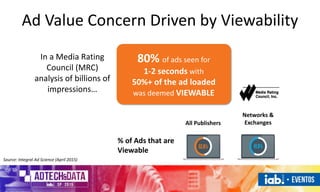

This document discusses 5 thought drivers for the media industry: follow the consumer, empower publishers, inspire buyer confidence, role of technology, and look beyond the horizon. It provides data showing consumers spending more time with more connected devices, leading advertisers to increasingly follow consumers to digital platforms. Publishers need technology to automate identifying, qualifying, nurturing and converting buyers. Addressing issues like ad fraud, blocking, and viewability is important to inspire buyer confidence. Simplifying technology stacks and using data insights can help publishers stay competitive.