Introduction to fundamentalsof

accounting

Accounting, the language of business, is a system

for recording, summarizing, and reporting financial

information to help stakeholders make informed

decisions. It involves identifying, recording,

classifying, summarizing, analyzing, interpreting,

and communicating financial information.

the primary purpose of accounting is to provide

accurate and reliable financial information to

stakeholders, enabling them to make informed

decisions.

3.

ACCOUNTING CONCEPTS

Fundamental assumptionsthat support accounting practices

1. Entity Concept – A business is treated as separate from its owners.

2. Money Measurement Concept – Only financial transactions measurable in

monetary terms are recorded.

3. Dual Aspect Concept – Every transaction affects two accounts (debit and

credit).

4. Historical Cost Concept – Assets are recorded at their original purchase

price.

5. Realization Concept – Revenue is recognized when earned, not necessarily

when cash is received.

4.

1. Income Statement(Profit & Loss Statement) – Shows revenues, expenses,

and net profit or loss over a period.

Revenue – Expenses = Net Profit/Loss

2. Balance Sheet (Statement of Financial Position) – Represents the financial

position of a business at a specific date.

Assets = Liabilities + Equity

3. Cash Flow Statement – Summarizes cash inflows and outflows under

operating, investing, and financing activities.

FINANCIAL

STATEMENTS

5.

ACCOUNTING

CYCLE

ACCOUNTING CYCLE STAGES

1.Identify transactions

2. Record journal entries

3. Post to ledger accounts

4. Prepare a trial balance

5. Adjust entries

6. Prepare financial statements

7. Close accounts

6.

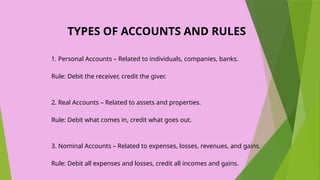

TYPES OF ACCOUNTSAND RULES

1. Personal Accounts – Related to individuals, companies, banks.

Rule: Debit the receiver, credit the giver.

2. Real Accounts – Related to assets and properties.

Rule: Debit what comes in, credit what goes out.

3. Nominal Accounts – Related to expenses, losses, revenues, and gains.

Rule: Debit all expenses and losses, credit all incomes and gains.

7.

KEY FINANCIAL RATIOS

KeyFinancial Ratios

1. Liquidity Ratios – Measure short-term financial stability.

Current Ratio = Current Assets / Current Liabilities

Quick Ratio = (Current Assets - Inventory) / Current Liabilities

2. Profitability Ratios – Measure profitability performance.

Gross Profit Margin = (Gross Profit / Revenue) × 100

Net Profit Margin = (Net Profit / Revenue) × 100

3. Leverage Ratios – Measure financial leverage and debt levels.

Debt-to-Equity Ratio = Total Liabilities / Shareholders’ Equity

4. Efficiency Ratios – Measure how effectively assets are utilized.

Inventory Turnover = Cost of Goods Sold / Average Inventory

8.

ACCOUNTING STANDARDS AND

REGULATORYBODIES

GAAP (Generally Accepted Accounting Principles) –

Standardized accounting guidelines used in many countries.

IFRS (International Financial Reporting Standards) – Global

accounting standards.

FASB (Financial Accounting Standards Board) – US regulatory

body for accounting standards.

IASB (International Accounting Standards Board) – Develops

IFRS standards.

9.

CONCLUSI0N

Accounting is essentialfor tracking financial transactions, ensuring compliance,

and guiding business decisions. A strong understanding of accounting principles, financial

statements, and ethical considerations helps businesses operate effectively and transparently.

Financial accounting helps organizations with accurate recordkeeping, which is key to creating

financial statements that meet accounting standards and legal guidelines. Organizations

following accounting best practices evaluate and optimize their performance more efficiently