Download to read offline

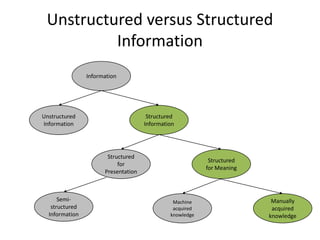

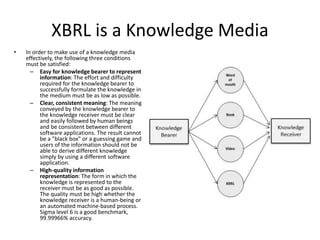

The document discusses the evolution of accounting, reporting, and auditing in light of technological advancements, particularly artificial intelligence and XBRL (eXtensible Business Reporting Language). It emphasizes the need for professionals in the field to update their understanding and skills to remain relevant as the industry transitions towards automation and digital reporting solutions. Additionally, it highlights the importance of developing 'computer empathy' and understanding the limitations and capabilities of technology to leverage it effectively in accounting practices.