Accounting Principle 6th Edition Weygandt Test Bank

Accounting Principle 6th Edition Weygandt Test Bank

Accounting Principle 6th Edition Weygandt Test Bank

Accounting Principle 6th Edition Weygandt Test Bank

Accounting Principle 6th Edition Weygandt Test Bank

1.

Accounting Principle 6thEdition Weygandt Test

Bank download

https://testbankfan.com/product/accounting-principle-6th-edition-

weygandt-test-bank/

Visit testbankfan.com today to download the complete set of

test bank or solution manual

2.

We believe theseproducts will be a great fit for you. Click

the link to download now, or visit testbankfan.com

to discover even more!

Financial Accounting 6th Edition Weygandt Test Bank

https://testbankfan.com/product/financial-accounting-6th-edition-

weygandt-test-bank/

Financial Accounting 6th Edition Weygandt Solutions Manual

https://testbankfan.com/product/financial-accounting-6th-edition-

weygandt-solutions-manual/

Managerial Accounting Tools for Business Decision Making

6th Edition Weygandt Test Bank

https://testbankfan.com/product/managerial-accounting-tools-for-

business-decision-making-6th-edition-weygandt-test-bank/

Principles of Economics 8th Edition Marshall Test Bank

https://testbankfan.com/product/principles-of-economics-8th-edition-

marshall-test-bank/

3.

Media Essentials 4thEdition Campbell Test Bank

https://testbankfan.com/product/media-essentials-4th-edition-campbell-

test-bank/

Hands-On Ethical Hacking and Network Defense 1st Edition

Simpson Test Bank

https://testbankfan.com/product/hands-on-ethical-hacking-and-network-

defense-1st-edition-simpson-test-bank/

Managerial Economics Foundations of Business Analysis and

Strategy 11th Edition Thomas Test Bank

https://testbankfan.com/product/managerial-economics-foundations-of-

business-analysis-and-strategy-11th-edition-thomas-test-bank/

Marine Biology 10th Edition Castro Solutions Manual

https://testbankfan.com/product/marine-biology-10th-edition-castro-

solutions-manual/

Intermediate Statistics Using SPSS 1st Edition Knapp

Solutions Manual

https://testbankfan.com/product/intermediate-statistics-using-

spss-1st-edition-knapp-solutions-manual/

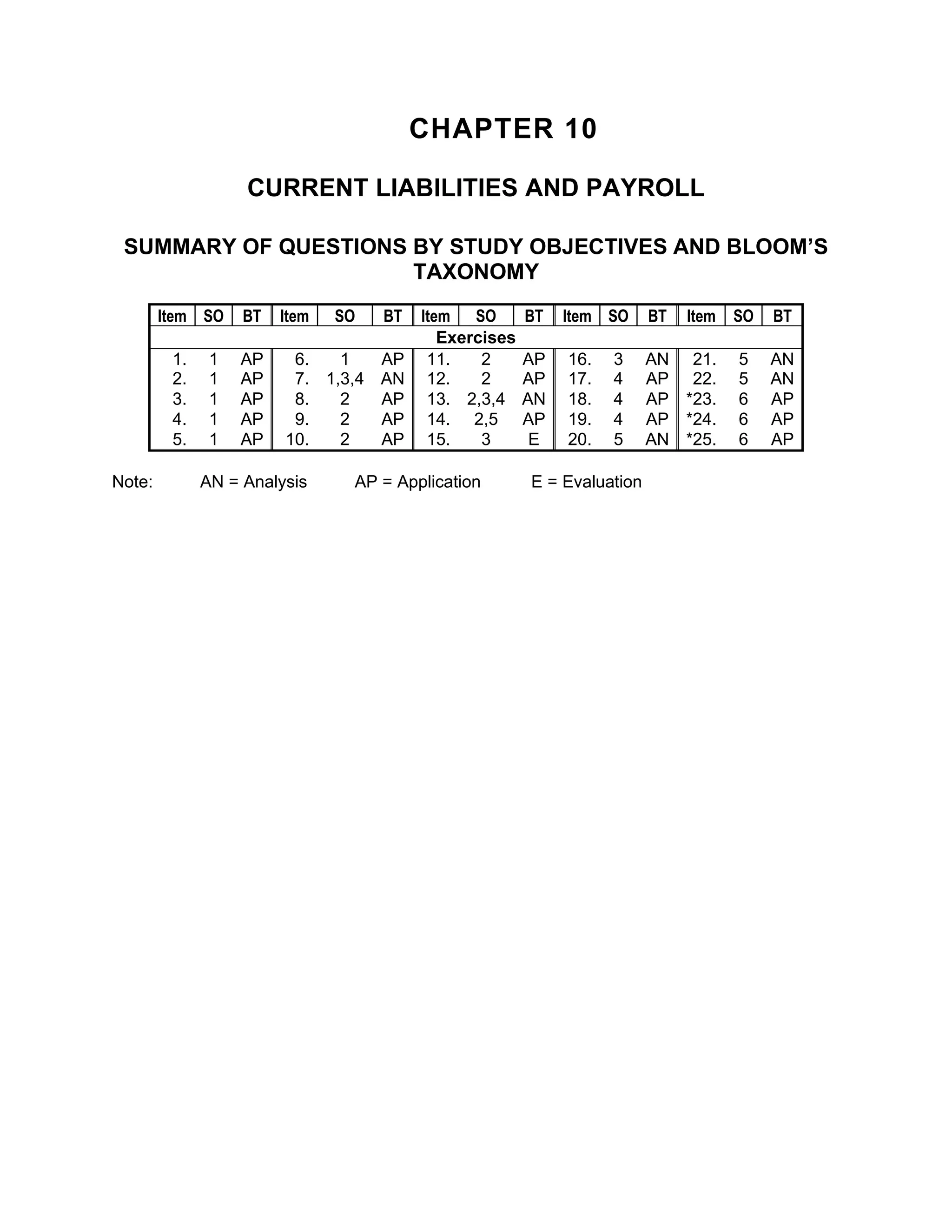

CHAPTER 10

CURRENT LIABILITIESAND PAYROLL

SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM’S

TAXONOMY

Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT

Exercises

1. 1 AP 6. 1 AP 11. 2 AP 16. 3 AN 21. 5 AN

2. 1 AP 7. 1,3,4 AN 12. 2 AP 17. 4 AP 22. 5 AN

3. 1 AP 8. 2 AP 13. 2,3,4 AN 18. 4 AP *23. 6 AP

4. 1 AP 9. 2 AP 14. 2,5 AP 19. 4 AP *24. 6 AP

5. 1 AP 10. 2 AP 15. 3 E 20. 5 AN *25. 6 AP

Note: AN = Analysis AP = Application E = Evaluation

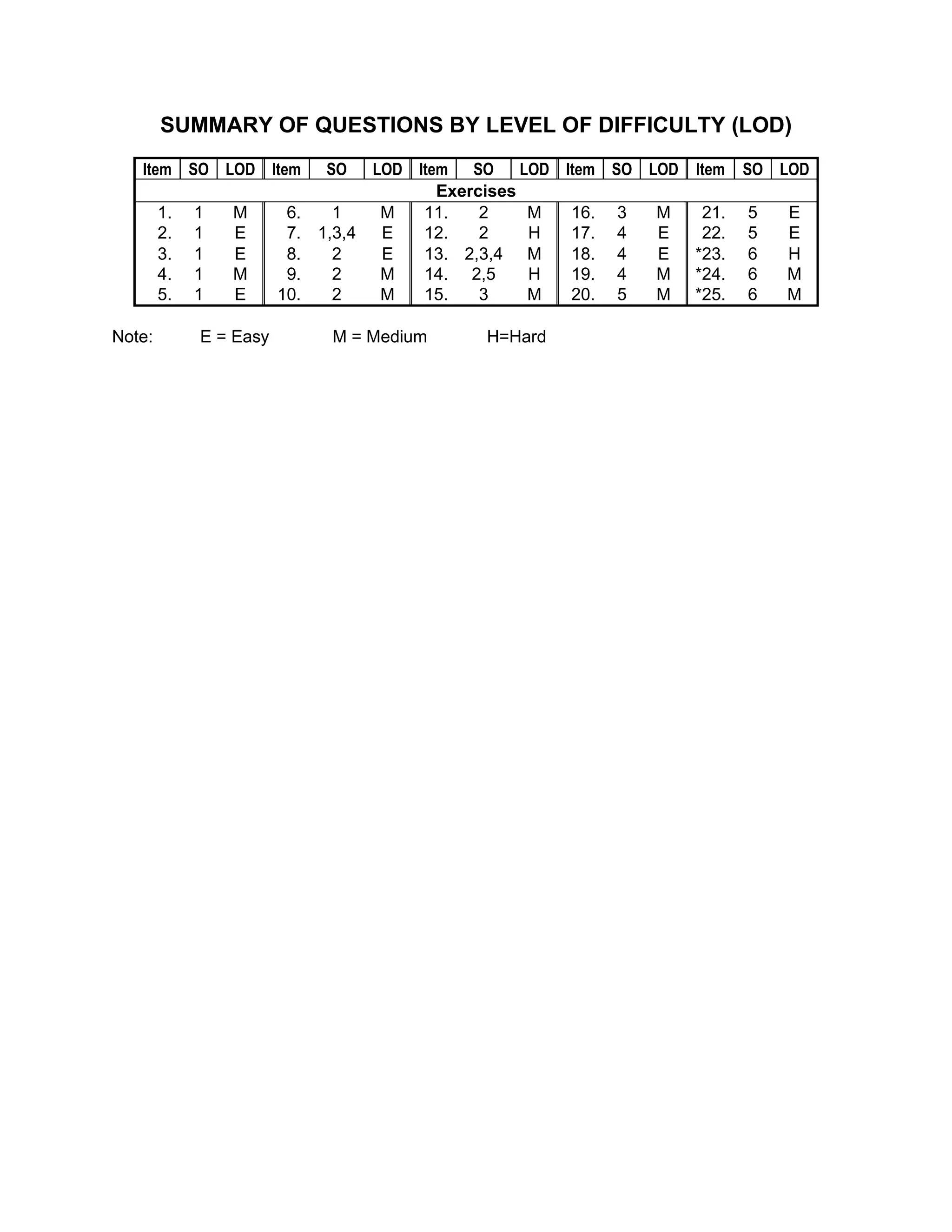

6.

SUMMARY OF QUESTIONSBY LEVEL OF DIFFICULTY (LOD)

Item SO LOD Item SO LOD Item SO LOD Item SO LOD Item SO LOD

Exercises

1. 1 M 6. 1 M 11. 2 M 16. 3 M 21. 5 E

2. 1 E 7. 1,3,4 E 12. 2 H 17. 4 E 22. 5 E

3. 1 E 8. 2 E 13. 2,3,4 M 18. 4 E *23. 6 H

4. 1 M 9. 2 M 14. 2,5 H 19. 4 M *24. 6 M

5. 1 E 10. 2 M 15. 3 M 20. 5 M *25. 6 M

Note: E = Easy M = Medium H=Hard

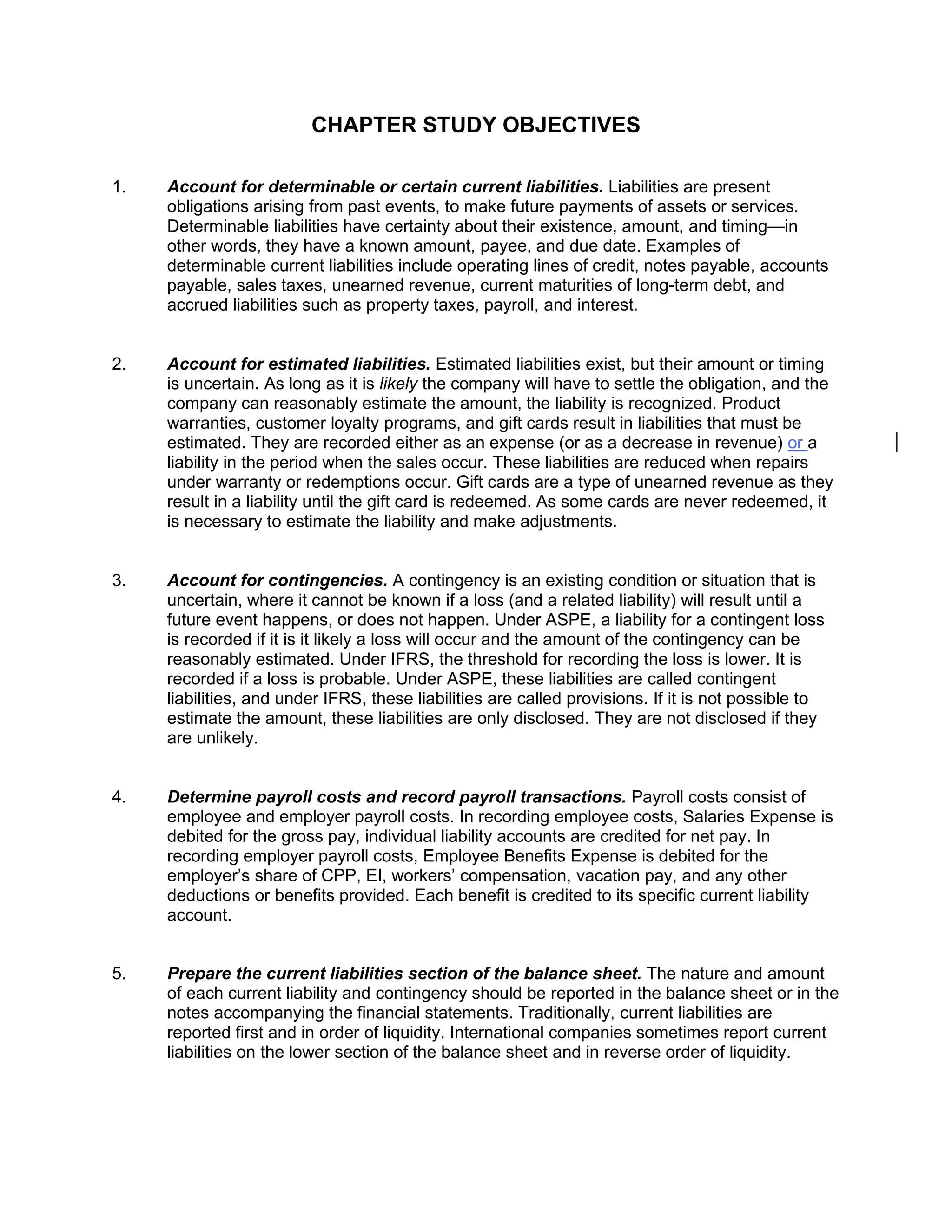

7.

CHAPTER STUDY OBJECTIVES

1.Account for determinable or certain current liabilities. Liabilities are present

obligations arising from past events, to make future payments of assets or services.

Determinable liabilities have certainty about their existence, amount, and timing—in

other words, they have a known amount, payee, and due date. Examples of

determinable current liabilities include operating lines of credit, notes payable, accounts

payable, sales taxes, unearned revenue, current maturities of long-term debt, and

accrued liabilities such as property taxes, payroll, and interest.

2. Account for estimated liabilities. Estimated liabilities exist, but their amount or timing

is uncertain. As long as it is likely the company will have to settle the obligation, and the

company can reasonably estimate the amount, the liability is recognized. Product

warranties, customer loyalty programs, and gift cards result in liabilities that must be

estimated. They are recorded either as an expense (or as a decrease in revenue) or a

liability in the period when the sales occur. These liabilities are reduced when repairs

under warranty or redemptions occur. Gift cards are a type of unearned revenue as they

result in a liability until the gift card is redeemed. As some cards are never redeemed, it

is necessary to estimate the liability and make adjustments.

3. Account for contingencies. A contingency is an existing condition or situation that is

uncertain, where it cannot be known if a loss (and a related liability) will result until a

future event happens, or does not happen. Under ASPE, a liability for a contingent loss

is recorded if it is it likely a loss will occur and the amount of the contingency can be

reasonably estimated. Under IFRS, the threshold for recording the loss is lower. It is

recorded if a loss is probable. Under ASPE, these liabilities are called contingent

liabilities, and under IFRS, these liabilities are called provisions. If it is not possible to

estimate the amount, these liabilities are only disclosed. They are not disclosed if they

are unlikely.

4. Determine payroll costs and record payroll transactions. Payroll costs consist of

employee and employer payroll costs. In recording employee costs, Salaries Expense is

debited for the gross pay, individual liability accounts are credited for net pay. In

recording employer payroll costs, Employee Benefits Expense is debited for the

employer’s share of CPP, EI, workers’ compensation, vacation pay, and any other

deductions or benefits provided. Each benefit is credited to its specific current liability

account.

5. Prepare the current liabilities section of the balance sheet. The nature and amount

of each current liability and contingency should be reported in the balance sheet or in the

notes accompanying the financial statements. Traditionally, current liabilities are

reported first and in order of liquidity. International companies sometimes report current

liabilities on the lower section of the balance sheet and in reverse order of liquidity.

8.

6. Calculate mandatorypayroll deductions (Appendix 10A). Mandatory payroll

deductions include CPP, EI, and income taxes. CPP is calculated by multiplying

pensionable earnings (gross pay minus the pay period exemption) by the CPP

contribution rate. EI is calculated by multiplying insurable earnings by the EI contribution

rate. Federal and provincial income taxes are calculated using a progressive tax scheme

and are based on taxable earnings and personal tax credits. The calculations are very

complex and it is best to use one of the CRA income tax calculation tools such as payroll

deduction tables.

9.

EXERCISES

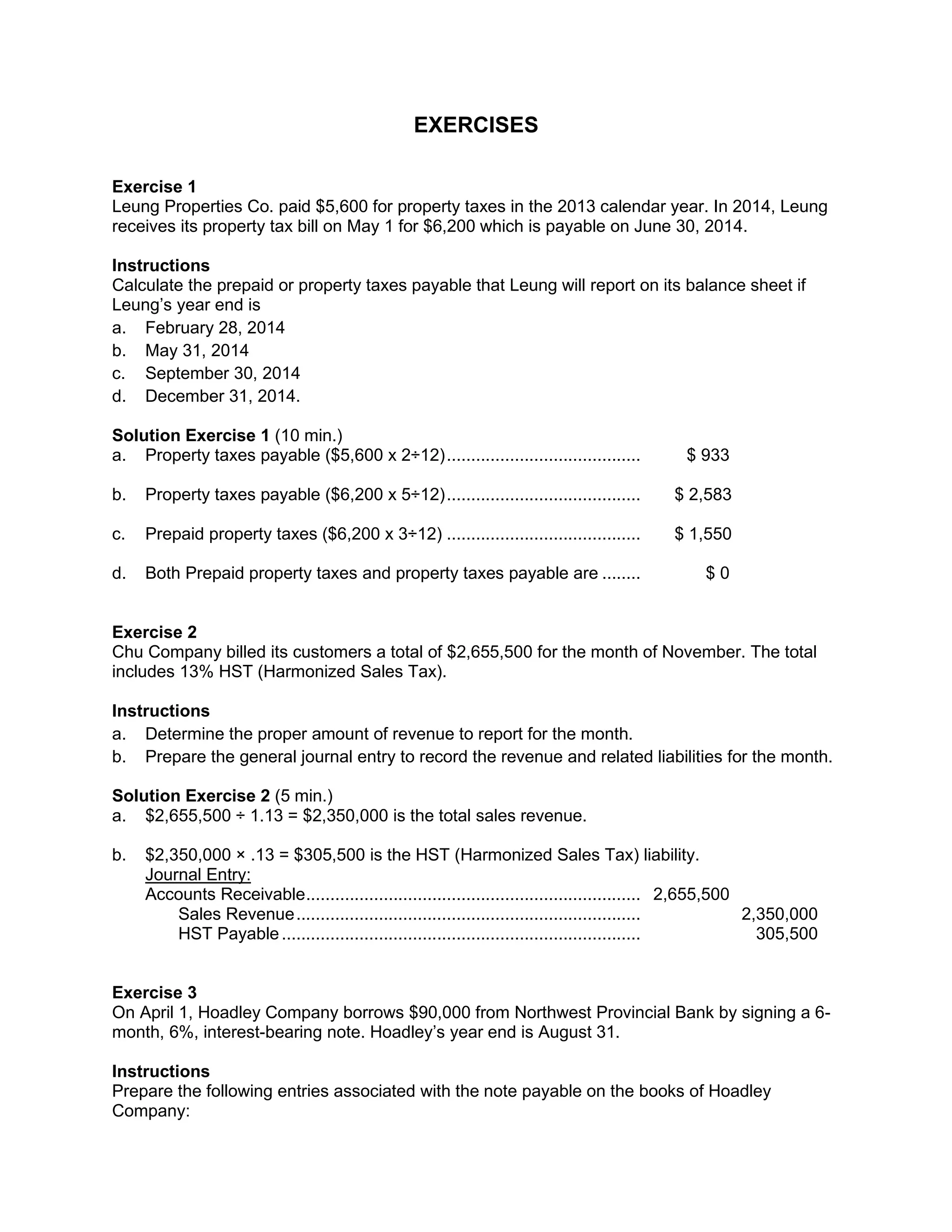

Exercise 1

Leung PropertiesCo. paid $5,600 for property taxes in the 2013 calendar year. In 2014, Leung

receives its property tax bill on May 1 for $6,200 which is payable on June 30, 2014.

Instructions

Calculate the prepaid or property taxes payable that Leung will report on its balance sheet if

Leung’s year end is

a. February 28, 2014

b. May 31, 2014

c. September 30, 2014

d. December 31, 2014.

Solution Exercise 1 (10 min.)

a. Property taxes payable ($5,600 x 2÷12)........................................ $ 933

b. Property taxes payable ($6,200 x 5÷12)........................................ $ 2,583

c. Prepaid property taxes ($6,200 x 3÷12) ........................................ $ 1,550

d. Both Prepaid property taxes and property taxes payable are ........ $ 0

Exercise 2

Chu Company billed its customers a total of $2,655,500 for the month of November. The total

includes 13% HST (Harmonized Sales Tax).

Instructions

a. Determine the proper amount of revenue to report for the month.

b. Prepare the general journal entry to record the revenue and related liabilities for the month.

Solution Exercise 2 (5 min.)

a. $2,655,500 ÷ 1.13 = $2,350,000 is the total sales revenue.

b. $2,350,000 × .13 = $305,500 is the HST (Harmonized Sales Tax) liability.

Journal Entry:

Accounts Receivable..................................................................... 2,655,500

Sales Revenue....................................................................... 2,350,000

HST Payable.......................................................................... 305,500

Exercise 3

On April 1, Hoadley Company borrows $90,000 from Northwest Provincial Bank by signing a 6-

month, 6%, interest-bearing note. Hoadley’s year end is August 31.

Instructions

Prepare the following entries associated with the note payable on the books of Hoadley

Company:

10.

a. The entryon April 1 when the note was issued.

b. Any adjusting entries necessary on May 31 in order to prepare the quarterly financial

statements. Assume no other interest accrual entries have been made.

c. The adjusting entry at August 31 to accrue interest.

d. The entry to record payment of the note at maturity.

Solution Exercise 3 (10 min.)

a. Apr 1 Cash ............................................................................. 90,000

Notes Payable........................................................ 90,000

b. May 31 Interest Expense ........................................................... 900

Interest Payable ..................................................... 900

($90,000 × 6% × 2÷12)

c. Aug 31 Interest Expense ........................................................... 1,350

Interest Payable ..................................................... 1,350

($90,000 × 6% × 3÷12)

d. Oct 1 Notes Payable............................................................... 90,000

Interest Payable ($900+$1,350) .................................... 2,250

Interest Expense ($90,000 x 6% x 1÷12)....................... 450

Cash....................................................................... 92,700

Exercise 4

Walters Accounting Company receives its annual property tax bill for the calendar year on

May1, 2015. The bill is for $32,000 and payable on June 30, 2015. Walters paid the bill on June

30, 2015. The company prepares quarterly financial statements and had initially estimated that

its 2015 property taxes would be $30,000.

Instructions

Prepare all the required journal entries for 2015 related to the property taxes.

Solution Exercise 4 (15 min.)

Mar 31 Property Tax Expense ($30,000 × 3÷12) ........................... 7,500

Property Tax Payable.................................................. 7,500

Jun 30 Property Tax Expense ($32,000 × 6÷12 - $7,500).............. 8,500

Property Tax Payable ........................................................ 7,500

Prepaid Property Tax ($32,000 x 6÷12) ............................. 16,000

Cash .......................................................................... 32,000

Sep 30 Property Tax Expense ($32,000 × 3÷12) ........................... 8,000

Prepaid Property Tax ................................................. 8,000

Dec 31 Property Tax Expense ($32,000 × 3÷12) ........................... 8,000

Prepaid Property Tax .................................................. 8,000

Exercise 5

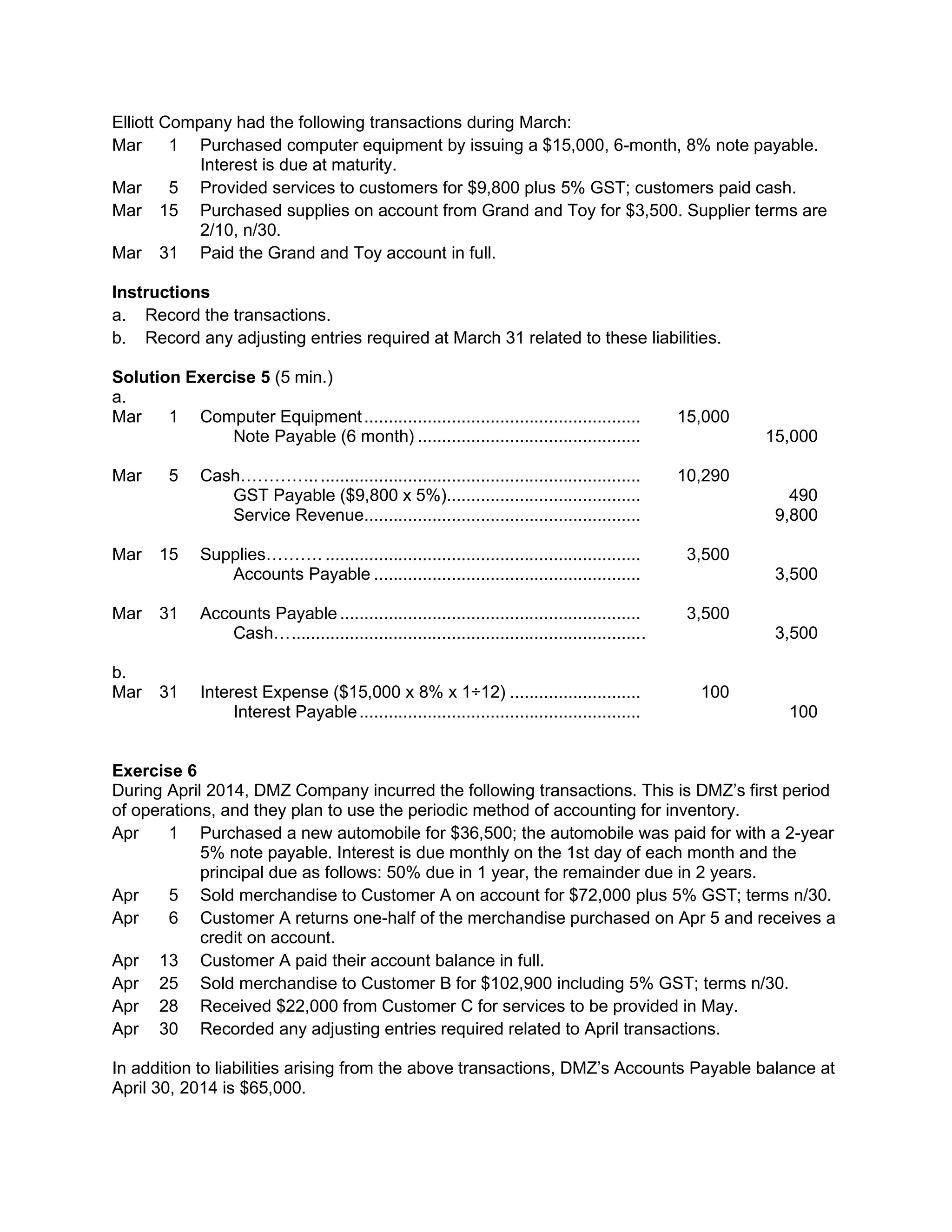

11.

Elliott Company hadthe following transactions during March:

Mar 1 Purchased computer equipment by issuing a $15,000, 6-month, 8% note payable.

Interest is due at maturity.

Mar 5 Provided services to customers for $9,800 plus 5% GST; customers paid cash.

Mar 15 Purchased supplies on account from Grand and Toy for $3,500. Supplier terms are

2/10, n/30.

Mar 31 Paid the Grand and Toy account in full.

Instructions

a. Record the transactions.

b. Record any adjusting entries required at March 31 related to these liabilities.

Solution Exercise 5 (5 min.)

a.

Mar 1 Computer Equipment......................................................... 15,000

Note Payable (6 month) .............................................. 15,000

Mar 5 Cash………….................................................................... 10,290

GST Payable ($9,800 x 5%)........................................ 490

Service Revenue......................................................... 9,800

Mar 15 Supplies………. ................................................................. 3,500

Accounts Payable ....................................................... 3,500

Mar 31 Accounts Payable .............................................................. 3,500

Cash…......................................................................... 3,500

b.

Mar 31 Interest Expense ($15,000 x 8% x 1÷12) ........................... 100

Interest Payable.......................................................... 100

Exercise 6

During April 2014, DMZ Company incurred the following transactions. This is DMZ’s first period

of operations, and they plan to use the periodic method of accounting for inventory.

Apr 1 Purchased a new automobile for $36,500; the automobile was paid for with a 2-year

5% note payable. Interest is due monthly on the 1st day of each month and the

principal due as follows: 50% due in 1 year, the remainder due in 2 years.

Apr 5 Sold merchandise to Customer A on account for $72,000 plus 5% GST; terms n/30.

Apr 6 Customer A returns one-half of the merchandise purchased on Apr 5 and receives a

credit on account.

Apr 13 Customer A paid their account balance in full.

Apr 25 Sold merchandise to Customer B for $102,900 including 5% GST; terms n/30.

Apr 28 Received $22,000 from Customer C for services to be provided in May.

Apr 30 Recorded any adjusting entries required related to April transactions.

In addition to liabilities arising from the above transactions, DMZ’s Accounts Payable balance at

April 30, 2014 is $65,000.

12.

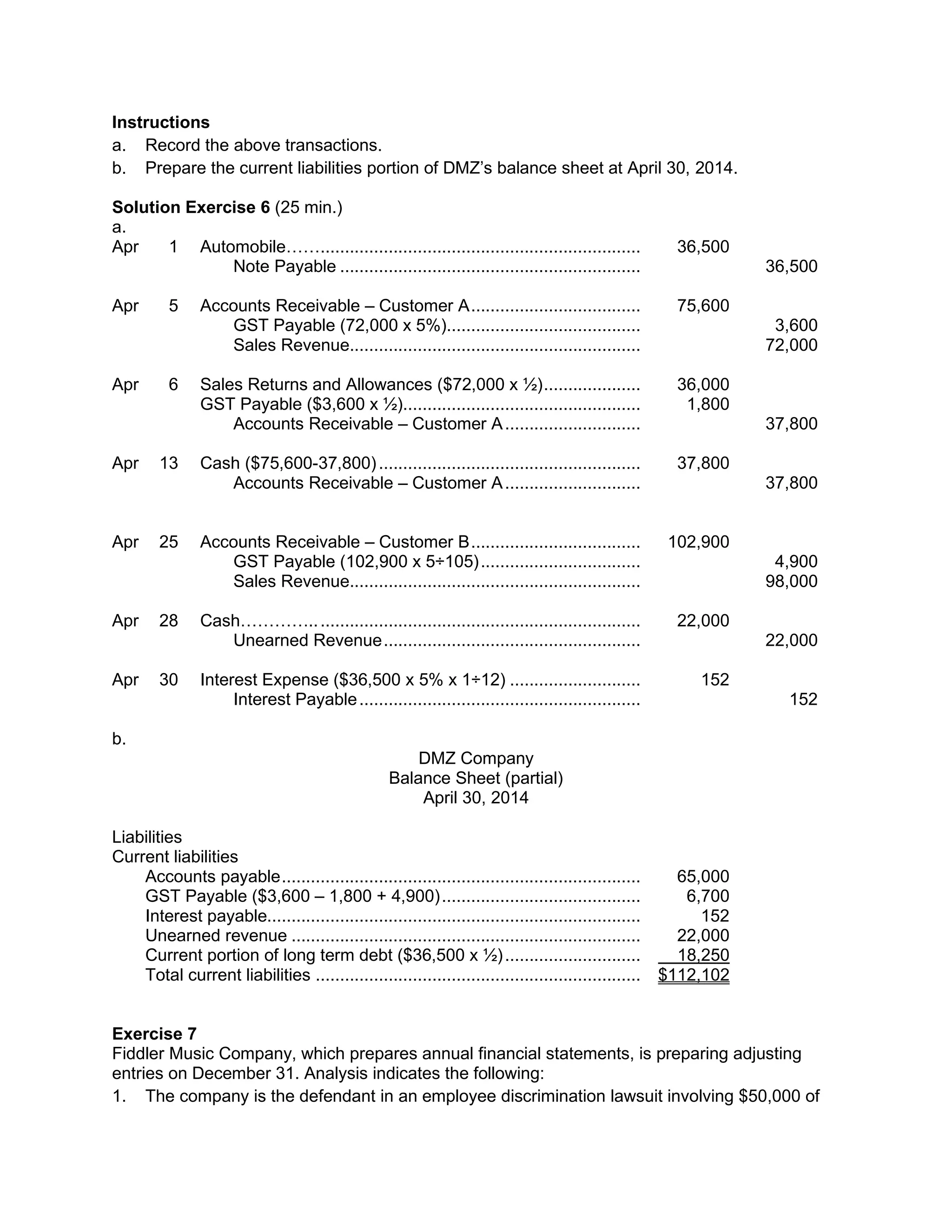

Instructions

a. Record theabove transactions.

b. Prepare the current liabilities portion of DMZ’s balance sheet at April 30, 2014.

Solution Exercise 6 (25 min.)

a.

Apr 1 Automobile…….................................................................. 36,500

Note Payable .............................................................. 36,500

Apr 5 Accounts Receivable – Customer A................................... 75,600

GST Payable (72,000 x 5%)........................................ 3,600

Sales Revenue............................................................ 72,000

Apr 6 Sales Returns and Allowances ($72,000 x ½).................... 36,000

GST Payable ($3,600 x ½)................................................. 1,800

Accounts Receivable – Customer A............................ 37,800

Apr 13 Cash ($75,600-37,800)...................................................... 37,800

Accounts Receivable – Customer A............................ 37,800

Apr 25 Accounts Receivable – Customer B................................... 102,900

GST Payable (102,900 x 5÷105)................................. 4,900

Sales Revenue............................................................ 98,000

Apr 28 Cash………….................................................................... 22,000

Unearned Revenue..................................................... 22,000

Apr 30 Interest Expense ($36,500 x 5% x 1÷12) ........................... 152

Interest Payable.......................................................... 152

b.

DMZ Company

Balance Sheet (partial)

April 30, 2014

Liabilities

Current liabilities

Accounts payable.......................................................................... 65,000

GST Payable ($3,600 – 1,800 + 4,900)......................................... 6,700

Interest payable............................................................................. 152

Unearned revenue ........................................................................ 22,000

Current portion of long term debt ($36,500 x ½)............................ 18,250

Total current liabilities ................................................................... $112,102

Exercise 7

Fiddler Music Company, which prepares annual financial statements, is preparing adjusting

entries on December 31. Analysis indicates the following:

1. The company is the defendant in an employee discrimination lawsuit involving $50,000 of

13.

damages. Legal counselbelieves it is unlikely that the company will have to pay any

damages.

2. December 31st is a Friday. The employees of the company have been paid on Monday,

December 27th for the previous week which ended on Friday, December 24th. The

company employs 30 people who earn $80 per day and 15 people who earn $120 per day.

All employees work 5-day weeks.

3. Employees are entitled to one day's vacation for each month worked. All employees

described above in 2. worked the month of December.

4. The company is a defendant in a $750,000 product liability lawsuit. Legal counsel believes

the company probably will have to pay the amount requested.

5. On November 1, Fiddler signed a $10,000, 6-month, 8% note payable. No interest has

been accrued to date.

Instructions

Prepare any adjusting entries necessary at the end of the year.

Solution Exercise 7 (12 min.)

1. No entry—loss is not likely.

2. Wages Expense............................................................................ 21,000

Wages Payable ...................................................................... 21,000

30 × $80 × 5 = $12,000

15 × $120 × 5 = 9,000

$21,000

3. Vacation Benefits Expense ........................................................... 4,200

Vacation Benefits Payable [(30 × $80) + (15 × $120)] ............ 4,200

4. Loss from Lawsuit ......................................................................... 750,000

Estimated Liability from Lawsuit ............................................. 750,000

5. Interest Expense ($10,000 × 8% × 2 ÷ 12) .................................... 133

Interest Payable ..................................................................... 133

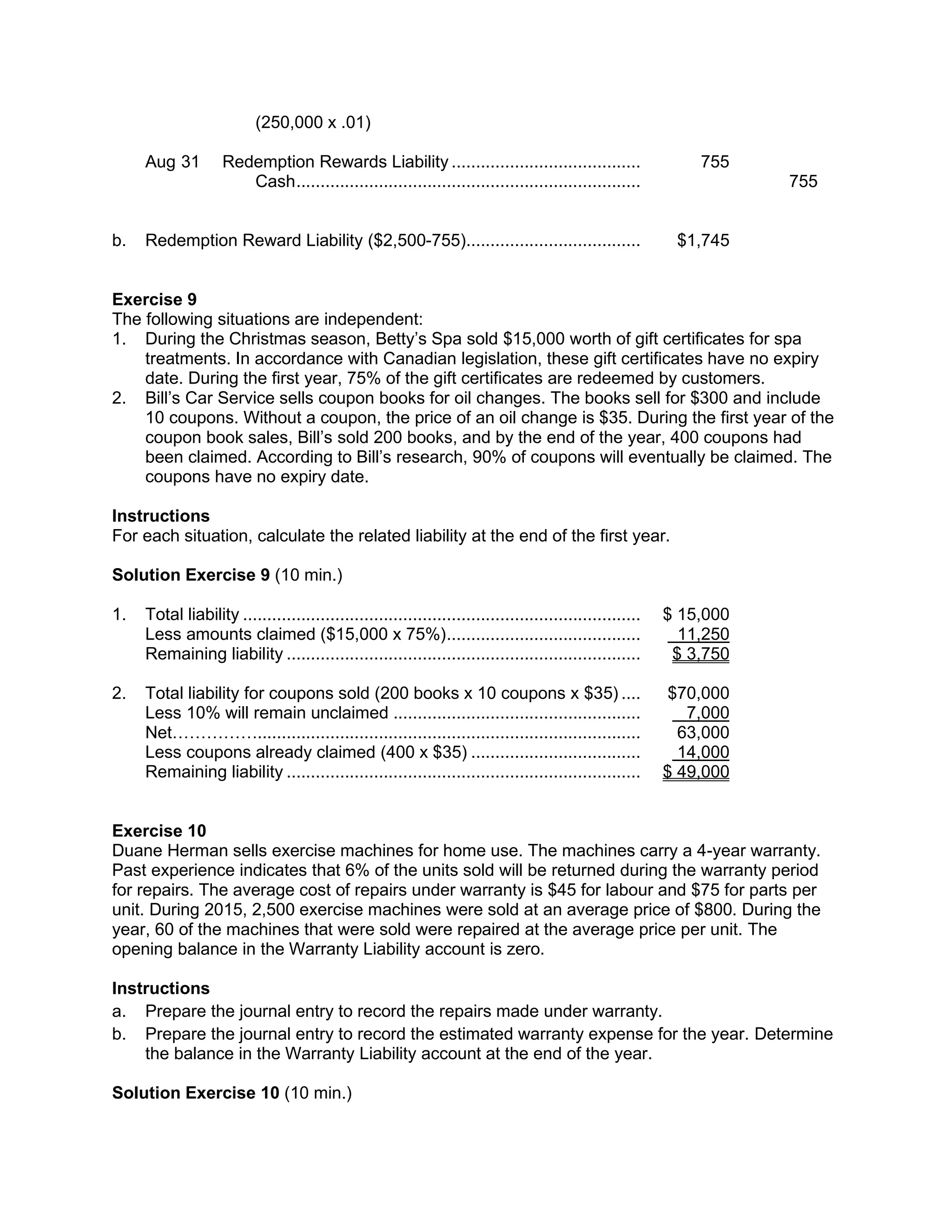

Exercise 8

During the month of July, Toys to Go started a new promotion. The company offered to reward

their customers for all sales made on Barbie dolls or Toy Trucks during the month of July. For

each sale made, the customer will receive a 1% reward of the sales price which can be

redeemed on future purchases until December of the current year. During the month of July,

$250,000 of Barbie dolls and Toy Trucks were sold. There was $755 worth of redemptions in

August.

Instructions

a. Prepare the journal entries to record all transactions related to the reward promotion.

b. Identify any liabilities that would be reported on the August 31, 2014 balance sheet.

Solution Exercise 8 (10 min.)

a. July 31 Sales Discounts for Redemption Rewards Issued ......... 2,500

Redemption Rewards Liability ................................ 2,500

14.

(250,000 x .01)

Aug31 Redemption Rewards Liability ....................................... 755

Cash....................................................................... 755

b. Redemption Reward Liability ($2,500-755).................................... $1,745

Exercise 9

The following situations are independent:

1. During the Christmas season, Betty’s Spa sold $15,000 worth of gift certificates for spa

treatments. In accordance with Canadian legislation, these gift certificates have no expiry

date. During the first year, 75% of the gift certificates are redeemed by customers.

2. Bill’s Car Service sells coupon books for oil changes. The books sell for $300 and include

10 coupons. Without a coupon, the price of an oil change is $35. During the first year of the

coupon book sales, Bill’s sold 200 books, and by the end of the year, 400 coupons had

been claimed. According to Bill’s research, 90% of coupons will eventually be claimed. The

coupons have no expiry date.

Instructions

For each situation, calculate the related liability at the end of the first year.

Solution Exercise 9 (10 min.)

1. Total liability .................................................................................. $ 15,000

Less amounts claimed ($15,000 x 75%)........................................ 11,250

Remaining liability ......................................................................... $ 3,750

2. Total liability for coupons sold (200 books x 10 coupons x $35) .... $70,000

Less 10% will remain unclaimed ................................................... 7,000

Net……………............................................................................... 63,000

Less coupons already claimed (400 x $35) ................................... 14,000

Remaining liability ......................................................................... $ 49,000

Exercise 10

Duane Herman sells exercise machines for home use. The machines carry a 4-year warranty.

Past experience indicates that 6% of the units sold will be returned during the warranty period

for repairs. The average cost of repairs under warranty is $45 for labour and $75 for parts per

unit. During 2015, 2,500 exercise machines were sold at an average price of $800. During the

year, 60 of the machines that were sold were repaired at the average price per unit. The

opening balance in the Warranty Liability account is zero.

Instructions

a. Prepare the journal entry to record the repairs made under warranty.

b. Prepare the journal entry to record the estimated warranty expense for the year. Determine

the balance in the Warranty Liability account at the end of the year.

Solution Exercise 10 (10 min.)

15.

a. Labour onrepaired units: $45 × 60 = $2,700

Parts on repaired units: $75 × 60 = $4,500

Warranty Liability........................................................................... 7,200

Repair Parts ........................................................................... 4,500

Wages Payable ...................................................................... 2,700

To record honouring of 60 warranty contracts

b. 2,500 units × 6% = 150 units

150 units × ($45+$75) = $18,000

Warranty Expense......................................................................... 18,000

Warranty Liability.................................................................... 18,000

To record estimated cost of honouring 150 warranty contracts

The balance in Warranty Liability at year end is $10,800 ($18,000 – $7,200), which equals the

expected cost of honouring the 90 remaining warranty contracts.

Exercise 11

Hardin Manufacturing began operations in January 2014. Hardin manufactures and sells two

different computer monitors.

Monitor A, is a flat panel hi-definition monitor, which carries a two-year manufacturer's warranty

against defects in workmanship. Hardin's management project that 8% of the monitors will

require repair during the first year of the warranty while approximately 6% will require repair

during the second year of the warranty. Monitor A sells for $400. The average cost to repair a

monitor is $80.

Monitor B is a regular LED monitor that retails for $150. Hardin has entered into an agreement

with a local electronics firm who charges Hardin $20 per monitor sold and then covers all

warranty costs related to this monitor.

Sales and warranty information for 2014 is as follows:

Sold 2,000 monitors (800 monitor A and 1,200 monitor B); all sales were on account.

Actual warranty expenditures for monitor A were $4,000.

Instructions

a. Prepare journal entries that summarize the sales and any aspects of the warranty for 2014.

b. Determine the balance in the Warranty Liability account at the end of 2014.

Solution Exercise 11 (5 min.)

a. To record sales

Accounts Receivable..................................................................... 500,000

Sales Revenue—A (800 × $400)............................................ 320,000

Sales Revenue—B (1,200 × $150)......................................... 180,000

Related to the cost of the maintenance contract on monitor B

Warranty Expense (1,200 × $20)................................................... 24,000

Cash....................................................................................... 24,000

16.

To estimate costof warranty on monitor A

Warranty Expense (800 × 14% × $80) .......................................... 8,960

Warranty Liability.................................................................... 8,960

To record actual warranty costs on monitor A

Warranty Liability........................................................................... 4,000

Cash....................................................................................... 4,000

b. $8,960 – $4,000 = $4,960

Exercise 12

During the year, Canada Ski Cross Ltd. instituted a customer rewards program. The company

sells skis which are specially used for the latest type of skiing, ski cross. For every $250 of ski

cross equipment purchased by a customer, the company will rebate $50 towards the cost of

purchasing a ski cross helmet. In January, the company had ski cross equipment sales of

$64,000. There were no helmets purchased. In February, there were sales of $32,600 and there

were 135 helmets sold.

Instructions

a. Prepare journal entries for January. What is the ending balance in the liability account for

the end of January?

b. Prepare journal entries for February. What is the ending balance in the liability account for

the end of February?

Solution Exercise 12 (10-13 min.)

a. January Entries

Cash ............................................................................................. $64,000

Sales...................................................................................... $64,000

Sales Discounts for Redemption Rewards .................................... 12,800

Redemptions Rewards Liability .............................................. 12,800

($64,000 ÷ $250 x $50)

Liability end of January = $12,800

b. February Entries

Cash ............................................................................................. $32,600

Sales...................................................................................... $32,600

Sales Discounts for Redemption Rewards .................................... 6,520

Redemptions Rewards Liability .............................................. 6,520

($32,600 ÷ $250 x $50)

Redemptions Rewards Liability ..................................................... 6,750

Cash....................................................................................... 6,750

(135 x 50)

Liability end of February ($12,800 + $6,520 – $6,750) = $12,570

Male man isnot in danger of passing out of existence but one

variety of man is doomed, the type which has always wished to mate

with the two types of women which, in the preceding chapter, I

declared doomed, the doll and the flirt.

The Wise Husband. That almost extinct species is the

type of husband who speakes of HIS wife, who knows "women" and

what is "good" for them, the home Jehovah, all-knowing and all-

powerful, who must be served and obeyed, who, on his return from

work must find his wife ready to entertain him if so he wishes, or to

plunge back into the depths of the kitchen if his mood so requires,

the husband who knows that he is the aim and goal of his wife's

existence.

A ridiculous old man, abandoned by his too young wife, made to

the reporters a statement betraying sadly the infinite conceit of that

type: "She will return to me because I love her so."

A most unprepossessing man was bewailing in my office the fact

that his wife had grown sexually indifferent to him. I advised him not

to compel her to have intercourse with him against her will,

especially as he was diseased. He naïvely remarked: "But she is my

wife."

That type of husband, in other words, considers a wife as a

chattel, to be submitted to any sort of legal indignity because she is

"only a female." He may force motherhood upon her to demonstrate

his doubtful virility or to protect his jealous egotism. He would

accept with enthusiasm Goldschmidt's theories which I presented for

what they were worth in the chapter on Virginity, and according to

which, woman is soft wax and characterless, waiting to be shaped

into a personality by her husband's caresses.

Scientific investigators of a more reliable type than Goldschmidt

and who avoid drawing "yellow" conclusions from their labors, have

supplied the reading world with facts which should cause the

Jehovah husband to fear for his lofty position.

19.

Is the MaleIndispensable? Jacques Loeb and

others have demonstrated that as far as the physical results of love,

the continuance of the race, is concerned, the male may not be

absolutely indispensable.

Loeb had shown that almost anything which causes the

protoplasm of the egg to separate itself from its membrane is

sufficient to introduce "life" into that curious organism which until

then only holds possibilities of life.

Nature, in order to produce one individual demands two

principles, one male and one female principle. She must have one

egg which is modified by some product of the male organism, pollen

or sperm.

Modern Scientists Have Beaten Nature at

Her Own Game of creation; they have taken one egg, the

female principle and proceeded to fertilise that egg without any male

product whatsoever.

The experiment has only been made on low forms of animal life,

sea urchins and the like, but the egg of the sea urchin is not

different in any essential respect from the egg of the human species.

By taking unfecundated eggs and placing them for two minutes

in a mixture of sea water and acetic, or butyric, or valerianic acid,

then placing them back in sea water and twenty minutes later,

immersing them for about an hour in hypertonic sea water or sugar

solution, and finally returning them to sea water, Loeb was able to

bring to life young larvæ. A French scientist, Delage, repeating the

same experiments managed to keep those larvæ alive until the time

of their sexual maturity.

Loeb also succeeded in fertilising eggs by placing them in the

blood serum of cows, sheep, pigs or rabbits.

Mathews has fertilised some by shaking them gently for a period

of time.

20.

Twins To Order.Loeb and others have gone further even

than that and produced not only single individuals but twins, triplets,

etc.

The secrets of nature's laboratory are being revealed more and

more clearly from day to day.

The conceited fathers who imagine that the bringing into life of

twins is a symptom of their powerful virility must learn that a mere

chemical phenomenon called osmosis is responsible for the over-

fertility of some wives.

Remove from sea water sea urchin's eggs and place them for

fifteen minutes or so in ordinary water. The density of water being

lower than that of sea water, the eggs will absorb a great deal of

water and burst open. A drop of protoplasm will come out at the

break in the membrane. Replace the exploded egg into sea water

and two larvæ will hatch out of it. Separate the two portions of the

exploded egg and the twins will be as healthy as tho they had been

allowed to grow for a while in Siamese style.

By repeating the experiment, Loeb has produced not only twins

but triplets and quadruplets, all normal and growing out of the same

egg which was only meant originally to produce one urchin.

One can understand how a variation in the pressure of the

liquids surrounding the human egg may lead to the same result.

While scientists have created living beings by using the female

principles as a basis, they have not thus far attained any results by

experimenting with the male principle alone.

The Mother is the Race apparently and the

stubbornness of man in claiming and fighting for the principle of

masculine superiority is apparently due to his obscure feeling that

after all he is not indispensable.

The more vociferous the claim, the weaker generally the basis

for that claim. In certain forms of insanity, the more the organism is

destroyed by disease the more extravagant the statements are

21.

which the insaneman makes about himself, claiming power, wealth,

health, youth, beauty, etc.

At least one animal species, the bees, have placed the male on

that footing. The male bee represents a convenient and pleasant

means of bringing about the fecundation of the eggs. After his

chemical part has been played, however, no one takes him seriously

and his official existence ends. Certain spiders and other insects

consider the male in the same light, some of them killing and eating

the male as soon as his fecundating activities have come to an end.

The feminine domination, if it should ever implant itself into our

world would undoubtedly lead to the absurdities, the exaggerations

and the repressions which are the result of our man made

civilisation.

Matriarchal Communities of the Past in which

the woman was the head of the family and probably of the state and

matriarchial groups of Tibet have not left visible tokens of their

worth as a family system. As they preceded the present family

system however, it may be that all traces of their achievements have

been obliterated by time. The Tibetan experiment may have been

blighted by unfavorable geographical conditions and rendered as

barren as the Mongolian patriarchal experiments in a neighboring

part of the world.

Man as a means of fecundation is not likely to be discarded by

normal women but his prestige is likely to decrease as the secret of

his mysterious power becomes better known.

The passing of the smug, self satisfied Jehovah husband, a

neurotic in every case, is in sight and his passing will facilitate the

adaptation of some of the inadapted women I mentioned in the

preceding chapter, some of whom fail to find love, and some of

whom do not dare to seek it.

The Successful Modern Woman is Rather

Conceited. Some of the things I said about female artists

22.

applies in agreat measure to the woman who in business or in a

profession has managed to make her mark.

After struggling years for a certain object which she has at last

attained, she is naturally loath to surrender her personality to the

average husband of the self-styled masculine type.

She at times resorts to homosexualism in an effort to retain her

independence and yet satisfy her love cravings without submitting to

a domination which she feels to be unjustified.

The Terrors of The Climateric. The passing of the

Jehovah husband will also ease a process of woman's (and man's)

life which has to this day held countless terrors to the uninitiated,

the climacteric.

To the old-fashioned and the gullible woman, the change of life

meant the end of life as a female. The stupid man, who is constantly

endeavoring to subdue his mate thru disparagement and kills

speedily her youth, her enthusiasm and her hopes by repeating

constantly the trashy "At your age, my dear," is in a great measure

responsible for transforming that harmless phenomenon into a

painful crisis, mental and physical.

The crisis of the "Dangerous Age," to use Karin Michaelis's

expression, is generally due to the clash of a weak masochistic

female with a weak and sadistic male, a clash in which, owing to age

and the staleness of the mates, affection has no redeeming,

consoling physical features.

The Masculine Man is in No Danger of

Passing Away and he will for ever be as attractive to woman

as the feminine woman is to him.

As Shaw said, what has been killed in men by the growth of

feminism is "not masculinity but boorishness," a characteristic, not of

the strong but of the weak, who is trying to compensate for his

weakness and to conceal it. What has been killed in woman is not

23.

feminine sweetness butoverfeminine silliness which woman used as

a deceptive weapon against the domineering male.

In a world which grants equal opportunities to men and women,

no husband will be able to justify or excuse his treatment of a

woman by saying "She is my wife." He will have to remain her lover

in order to hold her. No wife will be able to make the home hideous

and, at the same time, brandish over her husband's head the

certificate of enslavement called a marriage license. She will have, in

order to compete with the free women whose personality will impose

itself upon her environment, to remain his mistress.

Every step ahead which the world takes fortunately proves a

new step which love takes in the direction of completeness and

freedom from sordidness and ugliness.

24.

CHAPTER XXXI

Perfect MatrimonialAdjustments

While marriage, regardless of whatever form it may assume,

has always been mentioned in this book as unavoidably related to

love, we must not blink the fact that marriage and love are two

absolutely different things forced into frequent association by social

and economic necessity.

Love is an involuntary and compulsory craving which draws a

male and a female into the closest possible union for the purpose of

mutual sexual gratification, generally followed by conception and

reproduction.

Marriage a Compromise. Marriage on the other hand

is merely a compromise between the positive individual cravings

which demand the most complete and frequent gratification of the

love urge, regardless of its consequences, and the negative feeling

which causes the community to shirk all possible responsibilities

incurred by the individual, among others, the support of pregnant or

lactating females and of helpless infants.

Unless the community owns mother and child and can exploit

their labor or receive their cash value (slavery system), it demands

that their owner, the impregnator of the woman and procreator of

the child, supply food and shelter for both.

Marriage is also a compromise between two individual cravings

which may not be synchronised, as the male's desire for the female

may subside before her desire for him does, or reciprocally.

Through the institution of marriage the community protects

itself against new burdens directly by penalties (sentences against

wife deserters or those who abandon children) and indirectly by

25.

protecting the matesagainst their own cravings for whose duration

they are not responsible (laws against bigamy or adultery, etc.).

Considering the Artificial Character of the

Marriage Union, and at the same time the psychological

importance of its durability as far as the mental health of the off-

spring is concerned, one of the most pressing duties of the

community (and one which it never performs), should be to devise

all the possible ways and means whereby the sex cravings of both

mates could be helped to retain their freshness and strength as long

as possible.

Attractiveness an Asset. The first thought which

should be forced into the minds of modern men and women is that

attractiveness is a positive asset not only to woman but to man. In

classic Greece, a man could not be merely good, he had to be

beautiful too. By "good" the Greek meant "fit" but in the compound

word which implied both qualities, kalos, beauty came first.

Cravings being awakened and kept alive by certain fetishes, the

individual should be trained to recognize his and his mate's fetishism

and to make all possible efforts to retain, if necessary by artificial

means, the fetishes which lead to the awakening of erotism between

him and his mate.

The Average Man or Woman of Forty is a

Sorry Sight. Yet a little intelligence would compel them to

retain or regain the physical idiosyncrasies they exhibited at the time

of their marriage.

Too many women consider it sinful to devote much time to their

physical appearance and the care of their body. In a man, any

attempt to make himself attractive is considered in stupid middle-

class circles as a stigma of effeminacy.

The "pretty" man has always been despised by men and

women, and endocrinology has confirmed their judgment by

26.

revealing to usthat he is a glandular weakling. Between the pretty

man and the attractive man, however, there is a far cry.

While the American movies, generally speaking, are catering to

the weak-minded and the unimaginative, they have, in their search

for a bait where-with to catch audiences, rendered mankind a signal

service by starring the kind of man which would have passed muster

in ancient Greece, beautiful and fit.

Athletic, if not Acrobatic, Movie Idols present

to the female part of the audience a complex of physical qualities

which women will gradually demand from their mates. It is

regrettable that women should not attend prize fights in large

numbers, for the sight of the godlike participants in those affrays

would force them to institute enlightening comparisons between

professional fighters and the average male.

Besides retaining or regaining their fetishes, human beings

should make a special effort not to let those fetishes lose their

power.

The Worst Foe of Married Happiness. Balzac in

his "Physiology of Marriage" says that the married have to wage a

constant fight with a monster which devours everything: Habit.

Every stimulus, as we know, pleasant or unpleasant, loses its power

when applied continuously or too frequently.

It is only for the first minute or so that the ice cold shower

causes our naked skin to tingle with excitement. As soon as the

reaction sets in and the capillaries fill with red blood, the pleasant

sensation of the water needles becomes dulled.

After holding our hand for a minute in hot water, we no longer

realise the high temperature of the liquid and in order to continue to

experience the feeling of heat we must continually raise the

temperature of the water.

And likewise we may grow so accustomed to one source of

erotic stimulation that we become indifferent to it.

27.

Friendship May Survivethe Death of Sexual

Love, provided the sex desire has died in both mates at the same

time. When desire dies off in the wife first and is not replaced by

aversion, the situation may be very simple for she can still satisfy her

more ardent mate and derive some gratification therefrom.

When the man's desire dies first, on the other hand, there may

arise unpleasant complications. A man may be impotent with a

woman whom he loves tenderly but no longer desires sexually and

yet be potent with some other woman to whom he is not completely

"accustomed."

Jealousy on the part of the wife may then prevent the advent of

the platonic friendship which is not uncommon between old married

mates, altho Montaigne denies the possibility of its existence.

Modern mates, conscious of that danger, have now and then

devised ways and means to combat Balzac's monster.

Not so long ago a well-known woman writer announced that

she was planning to marry a certain man with whom, however, she

did not intend to live day after day. The experiment has many

chances of success if jealousy does not complicate the situation.

I suggested to reporters last summer, when two famous artists

parted company, that their union might have been of longer duration

if one of them had lived at the Plaza while the other was stopping at

the St. Regis.

Married People Should Separate for Periods

of Variable Duration in order that a fresh stimulation may

emanate from their fetishes when they meet again. By leading more

individual lives and having separate sets of friends, they would,

besides, bring to each other a new sort of mental pabulum and

stimulation day after day. Conversation becomes futile and

unnecessary between a husband and wife who always pay and

receive calls together, attend the same spectacles and hence always

see the same side of life. Now and then we read of couples who

28.

separate and afew years later remarry. Those few years spent apart

from each other mean for both new experiences which enrich their

mind and their conversation and make them again interesting to

each other.

The Play Function of Love. Another factor which the

monstrous hypocrisy of puritanism makes very difficult to discuss

openly and honestly and which wrecks many promising unions is the

ignorance, more common than we suspect among married couples,

of what Maurice Parmelee in his "Personality and Behavior" has

called the Play Function of Love, a term which has been given a

broader meaning by Havelock Ellis in an article for the Medical

Review of Reviews for March 1921.

The average man or woman is tragically ignorant of the mission

of sex.

The average man, as Ellis writes, has two aims: "to prove that

he is a man and to relieve a sexual tension.

"He too often considers himself, from traditional habits, as the

active partner in love and his own pleasure as the prime motive of

the sex communion.

"His wife, naturally adopts the complementary attitude, regards

herself as the passive partner and her pleasure as negligible.

"She has not mastered the art of love, with the result that her

whole nature remains ill-developed and unharmonized, and that she

is incapable of bringing her personality (having indeed no achieved

personality to bring) to bear effectively on the problems of society

and the world around her."

I have described in "Sex Happiness" the tragedies which result

from that form of ignorance, especially the tragedy of the unsatisfied

wife, her restlessness, her gradual dislike of her mate, her curiosity

as to what feelings she might experience if married to another man,

when some other man seems to awaken her erotism, and then the

29.

dilemma, repression leadingto neurosis, or indulgence leading into

the divorce court.

Psychoanalysis to the Rescue. "In this matter,"

Ellis writes, "we may learn a lesson from the psychoanalysts of today

without any implication that psychoanalysis is necessarily a desirable

or even possible way of attaining the revelation of love. The wiser

psychoanalysts insist that the process of liberating the individual

from outer and inner influences that repress or deform his energies

and impulses is effected by removing the inhibitions on the free play

of his nature.

"It is a process of education in the true sense, not of the

suppression of natural impulses nor even of the instillation of sound

rules and maxims for their control, not of the pressing in but of the

leading out of the individual's special tendencies.

"It removes inhibitions, even inhibitions that were placed upon

the individual, or that he consciously or unconsciously placed upon

himself, with the best moral intentions, and by so doing it allows a

larger and freer and more natively spontaneous morality to come

into play.

"It has this influence above all in the sphere of sex, where such

inhibitions have been most powerfully laid on the native impulses,

where the natural tendencies have been most surrounded by taboos

and terrors, most tinged with artificial stains of impurity and

degradation derived from alien and antiquated traditions.

"Thus the therapeutical experience of the psychoanalysts

reinforce the lessons we learn from physiology and psychology and

the intimate experiences of life."

Wounded Egotism. Love in marriage is endangered

from another quarter: The greatest foe of sexual desire, as I have

stated several times in this book, is wounded egotism.

A perfect matrimonial adjustment does not mean the

modification of either mate's personality. We have seen in the

30.

chapters on glandsthat the normal personality is practically

inadaptable, that is, nothing short of serious sickness or a surgical

operation can transform an active person into a sluggish one and

vice versa.

It is only the neurotic personality which can be adapted by the

removal of certain unconscious fears which prevent it from attaining

social and biological balance and happiness.

All psychoanalysis does in such cases is to teach the patient to

accept everything which is biologically normal in his personality.

We must then have an absolute respect for personality in

ourselves and others. We must find a socially acceptable outlet for

all our idiosyncrasies, a difficult, but never impossible task.

Lack of an outlet means a neurotic disturbance. The so-called

adaptable people are those who succeed in repressing temporarily

their cravings and denying their existence, a result which they attain

at the cost of much suffering to themselves and, indirectly, to their

environment.

Democracy in the Home is the prerequisite of every

perfect matrimonial adjustment.

The autocratic government of the home by a male bully of a

female nag leads to either a revolution (divorce) or to the

destruction of human material after a bitter strife, (neurotic

ailments).

The bullied wife and the henpecked husband fill the offices of

neurologists, gynaecologists, psychoanalysts and sexologists. This is

the way in which the wounded ego of the defeated mate avenges

itself.

The defeated mate becomes sexually disabled.

The results of maladjustment of the mates are strikingly

summed up by Kempf in his monumental work "Psychopathology":

31.

"Upon marriage asubtle if not overt struggle occurs between

the mates for the dominant position in the contract. The big,

aggressive wife and the timid, little husband attest to the importance

of organic superiority in the adjustment, but the average marriage

does not show such organic differences. The sadistic or masochistic

husband and the masochistic or sadistic wife will certainly adjust to

please their reciprocating cravings, no matter what influence this

may have upon their children, and a sadistic wife and sadistic

husband, although both are cruel in their pleasures, will divorce each

other on the charge of the other being cruel; but it is the

commonplace adjustment which interests us most, because it is

most predominant.

"Nature places an unerring punishment upon the woman, who,

by incessantly using every whim, scheme or artifice, finally succeeds

in dominating her husband. By forcing him to submit to her

thousand and one demands and coercions, within a few years, he

unconsciously becomes a submissive type and loses his sexual

potency with her as the love-object. If he does not have secret love

interests which stimulate him to strive for power, he finally loses his

initiative and sexual potency completely and must live always at a

commonplace level, the servant of more virile men: the counterpart

of the subdued impotent males of the animal herd.

"His more aggressive, selfish mate, if periodically heterosexually

erotic, will become neurotic if her moral restraints are insurpassable,

or seek a new mate whom she will again attempt to subdue. Never

is she able to realise that her selfishness makes her sexually

unattractive. The psychopathologist meets many such women whose

husbands have evaded domination by secretly depending upon the

affections of another more suitably adjusted woman."

In "The New Horizon in Love and Life," Mrs. Havelock Ellis

writes "It is more than probable that the evolved relationship of the

future will be monogamy—but a monogamy wider and more

beautiful than the present caricature of it, as the sea is wider and

more delicious than a duck pond.

32.

"The lifelong, faithfullove of one man for one woman is the

exception and not the rule. The law of affinity being as subtle and as

indefinable as the law of gravitation, we may, by and by, find it

worth while to give it its complete opportunity in those realms where

it can manifest itself most potently. We are on the wrong bridge if

we imagine that laxity is the easiest way to freedom. The bridge

which will bear us must be strong enough to support us while

experiments are tried.

"What is the gospel in this matter of sexual emancipation for

men and women in the new world where love has actually come of

age? It is surely the complete economic independence of women.

While man is economically free and woman still a slave, either

physically, financially or spiritually, mankind as a whole must act as if

blindness, maimness and deafness constituted health.

"The complete independence of husband and wife is the gospel

of the new era of marriage. This is the actual matter which

philosophers, parents, philanthropists and pioneers so often ignore

when teaching the new ideals of morality. When a woman is kept by

a man she is not a free individuality either as child, wife or mistress.

Imagine for a moment a man kept by a woman as women are kept

by men and a sense of humor illuminates the absurdity of the

situation between any class of evolved human beings."

As a clever patient of mine whom I regret I cannot mention by

name said one day: "married happiness, to be lasting, requires more

than sexual cooperation of both mates, it must resolve itself into

cooperative egotism."

33.

Footnotes

[1] See MarySinclair's "The Life and Death of Harriet Freau."

[2] Kings. I, 1-2.

[3] Birth Control Review, April 1922.

THE END

Suggestive draperies, 125

Sutteecustom, 142

Syphilophobiacs, 80

Tall types, 235

Taste, 59

Teeth, 237

Telegony, 116

Test of love, 75

Third sex, 158 sqq.

Thyroid, 230

Touch, 60

Transvestites, 159

Triplets, 310

Twins, 309

Type, parent, 39

Ultrafeminine, 93

Unadapted women, 288

Uniform fetishism, 25

Vamps, 213

Varietism, 84

Vital Force, 266

Vomiting, in pregnancy,

243

Von Kupfer, 181, 182

Wagner, 252

Walker, Dr. Mary, 160

War prisoners, 70

46.

Whipping, 202

Wifehood, aprofession,

282

Wilde, Oscar, 180

Will-to-be-the-first, 115

Winckelman, 176

Wise husbands, 306

Women Sadists, 210

Women who enjoy a

beating, 209

Wounded egotism, 324

Wulffen, 193

47.

*** END OFTHE PROJECT GUTENBERG EBOOK PSYCHOANALYSIS

AND LOVE ***

Updated editions will replace the previous one—the old editions will

be renamed.

Creating the works from print editions not protected by U.S.

copyright law means that no one owns a United States copyright in

these works, so the Foundation (and you!) can copy and distribute it

in the United States without permission and without paying

copyright royalties. Special rules, set forth in the General Terms of

Use part of this license, apply to copying and distributing Project

Gutenberg™ electronic works to protect the PROJECT GUTENBERG™

concept and trademark. Project Gutenberg is a registered trademark,

and may not be used if you charge for an eBook, except by following

the terms of the trademark license, including paying royalties for use

of the Project Gutenberg trademark. If you do not charge anything

for copies of this eBook, complying with the trademark license is

very easy. You may use this eBook for nearly any purpose such as

creation of derivative works, reports, performances and research.

Project Gutenberg eBooks may be modified and printed and given

away—you may do practically ANYTHING in the United States with

eBooks not protected by U.S. copyright law. Redistribution is subject

to the trademark license, especially commercial redistribution.

START: FULL LICENSE

PLEASE READ THISBEFORE YOU DISTRIBUTE OR USE THIS WORK

To protect the Project Gutenberg™ mission of promoting the free

distribution of electronic works, by using or distributing this work (or

any other work associated in any way with the phrase “Project

Gutenberg”), you agree to comply with all the terms of the Full

Project Gutenberg™ License available with this file or online at

www.gutenberg.org/license.

Section 1. General Terms of Use and

Redistributing Project Gutenberg™

electronic works

1.A. By reading or using any part of this Project Gutenberg™

electronic work, you indicate that you have read, understand, agree

to and accept all the terms of this license and intellectual property

(trademark/copyright) agreement. If you do not agree to abide by all

the terms of this agreement, you must cease using and return or

destroy all copies of Project Gutenberg™ electronic works in your

possession. If you paid a fee for obtaining a copy of or access to a

Project Gutenberg™ electronic work and you do not agree to be

bound by the terms of this agreement, you may obtain a refund

from the person or entity to whom you paid the fee as set forth in

paragraph 1.E.8.

1.B. “Project Gutenberg” is a registered trademark. It may only be

used on or associated in any way with an electronic work by people

who agree to be bound by the terms of this agreement. There are a

few things that you can do with most Project Gutenberg™ electronic

works even without complying with the full terms of this agreement.

See paragraph 1.C below. There are a lot of things you can do with

Project Gutenberg™ electronic works if you follow the terms of this

agreement and help preserve free future access to Project

Gutenberg™ electronic works. See paragraph 1.E below.

50.

1.C. The ProjectGutenberg Literary Archive Foundation (“the

Foundation” or PGLAF), owns a compilation copyright in the

collection of Project Gutenberg™ electronic works. Nearly all the

individual works in the collection are in the public domain in the

United States. If an individual work is unprotected by copyright law

in the United States and you are located in the United States, we do

not claim a right to prevent you from copying, distributing,

performing, displaying or creating derivative works based on the

work as long as all references to Project Gutenberg are removed. Of

course, we hope that you will support the Project Gutenberg™

mission of promoting free access to electronic works by freely

sharing Project Gutenberg™ works in compliance with the terms of

this agreement for keeping the Project Gutenberg™ name associated

with the work. You can easily comply with the terms of this

agreement by keeping this work in the same format with its attached

full Project Gutenberg™ License when you share it without charge

with others.

1.D. The copyright laws of the place where you are located also

govern what you can do with this work. Copyright laws in most

countries are in a constant state of change. If you are outside the

United States, check the laws of your country in addition to the

terms of this agreement before downloading, copying, displaying,

performing, distributing or creating derivative works based on this

work or any other Project Gutenberg™ work. The Foundation makes

no representations concerning the copyright status of any work in

any country other than the United States.

1.E. Unless you have removed all references to Project Gutenberg:

1.E.1. The following sentence, with active links to, or other

immediate access to, the full Project Gutenberg™ License must

appear prominently whenever any copy of a Project Gutenberg™

work (any work on which the phrase “Project Gutenberg” appears,

or with which the phrase “Project Gutenberg” is associated) is

accessed, displayed, performed, viewed, copied or distributed:

51.

This eBook isfor the use of anyone anywhere in the United

States and most other parts of the world at no cost and with

almost no restrictions whatsoever. You may copy it, give it away

or re-use it under the terms of the Project Gutenberg License

included with this eBook or online at www.gutenberg.org. If you

are not located in the United States, you will have to check the

laws of the country where you are located before using this

eBook.

1.E.2. If an individual Project Gutenberg™ electronic work is derived

from texts not protected by U.S. copyright law (does not contain a

notice indicating that it is posted with permission of the copyright

holder), the work can be copied and distributed to anyone in the

United States without paying any fees or charges. If you are

redistributing or providing access to a work with the phrase “Project

Gutenberg” associated with or appearing on the work, you must

comply either with the requirements of paragraphs 1.E.1 through

1.E.7 or obtain permission for the use of the work and the Project

Gutenberg™ trademark as set forth in paragraphs 1.E.8 or 1.E.9.

1.E.3. If an individual Project Gutenberg™ electronic work is posted

with the permission of the copyright holder, your use and distribution

must comply with both paragraphs 1.E.1 through 1.E.7 and any

additional terms imposed by the copyright holder. Additional terms

will be linked to the Project Gutenberg™ License for all works posted

with the permission of the copyright holder found at the beginning

of this work.

1.E.4. Do not unlink or detach or remove the full Project

Gutenberg™ License terms from this work, or any files containing a

part of this work or any other work associated with Project

Gutenberg™.

1.E.5. Do not copy, display, perform, distribute or redistribute this

electronic work, or any part of this electronic work, without

prominently displaying the sentence set forth in paragraph 1.E.1

52.

Welcome to ourwebsite – the perfect destination for book lovers and

knowledge seekers. We believe that every book holds a new world,

offering opportunities for learning, discovery, and personal growth.

That’s why we are dedicated to bringing you a diverse collection of

books, ranging from classic literature and specialized publications to

self-development guides and children's books.

More than just a book-buying platform, we strive to be a bridge

connecting you with timeless cultural and intellectual values. With an

elegant, user-friendly interface and a smart search system, you can

quickly find the books that best suit your interests. Additionally,

our special promotions and home delivery services help you save time

and fully enjoy the joy of reading.

Join us on a journey of knowledge exploration, passion nurturing, and

personal growth every day!

testbankfan.com

![damages. Legal counsel believes it is unlikely that the company will have to pay any

damages.

2. December 31st is a Friday. The employees of the company have been paid on Monday,

December 27th for the previous week which ended on Friday, December 24th. The

company employs 30 people who earn $80 per day and 15 people who earn $120 per day.

All employees work 5-day weeks.

3. Employees are entitled to one day's vacation for each month worked. All employees

described above in 2. worked the month of December.

4. The company is a defendant in a $750,000 product liability lawsuit. Legal counsel believes

the company probably will have to pay the amount requested.

5. On November 1, Fiddler signed a $10,000, 6-month, 8% note payable. No interest has

been accrued to date.

Instructions

Prepare any adjusting entries necessary at the end of the year.

Solution Exercise 7 (12 min.)

1. No entry—loss is not likely.

2. Wages Expense............................................................................ 21,000

Wages Payable ...................................................................... 21,000

30 × $80 × 5 = $12,000

15 × $120 × 5 = 9,000

$21,000

3. Vacation Benefits Expense ........................................................... 4,200

Vacation Benefits Payable [(30 × $80) + (15 × $120)] ............ 4,200

4. Loss from Lawsuit ......................................................................... 750,000

Estimated Liability from Lawsuit ............................................. 750,000

5. Interest Expense ($10,000 × 8% × 2 ÷ 12) .................................... 133

Interest Payable ..................................................................... 133

Exercise 8

During the month of July, Toys to Go started a new promotion. The company offered to reward

their customers for all sales made on Barbie dolls or Toy Trucks during the month of July. For

each sale made, the customer will receive a 1% reward of the sales price which can be

redeemed on future purchases until December of the current year. During the month of July,

$250,000 of Barbie dolls and Toy Trucks were sold. There was $755 worth of redemptions in

August.

Instructions

a. Prepare the journal entries to record all transactions related to the reward promotion.

b. Identify any liabilities that would be reported on the August 31, 2014 balance sheet.

Solution Exercise 8 (10 min.)

a. July 31 Sales Discounts for Redemption Rewards Issued ......... 2,500

Redemption Rewards Liability ................................ 2,500](https://image.slidesharecdn.com/6776-250711062509-3e7df281/75/Accounting-Principle-6th-Edition-Weygandt-Test-Bank-13-2048.jpg)

![Footnotes

[1] See Mary Sinclair's "The Life and Death of Harriet Freau."

[2] Kings. I, 1-2.

[3] Birth Control Review, April 1922.

THE END](https://image.slidesharecdn.com/6776-250711062509-3e7df281/75/Accounting-Principle-6th-Edition-Weygandt-Test-Bank-33-2048.jpg)