Accounting Principle 6th Edition Weygandt Test Bank

Accounting Principle 6th Edition Weygandt Test Bank

Accounting Principle 6th Edition Weygandt Test Bank

Accounting Principle 6th Edition Weygandt Test Bank

Accounting Principle 6th Edition Weygandt Test Bank

1.

Download the fullversion and explore a variety of test banks

or solution manuals at https://testbankfan.com

Accounting Principle 6th Edition Weygandt Test

Bank

_____ Tap the link below to start your download _____

https://testbankfan.com/product/accounting-principle-6th-

edition-weygandt-test-bank/

Find test banks or solution manuals at testbankfan.com today!

2.

We believe theseproducts will be a great fit for you. Click

the link to download now, or visit testbankfan.com

to discover even more!

Financial Accounting 6th Edition Weygandt Test Bank

https://testbankfan.com/product/financial-accounting-6th-edition-

weygandt-test-bank/

Financial Accounting 6th Edition Weygandt Solutions Manual

https://testbankfan.com/product/financial-accounting-6th-edition-

weygandt-solutions-manual/

Managerial Accounting Tools for Business Decision Making

6th Edition Weygandt Test Bank

https://testbankfan.com/product/managerial-accounting-tools-for-

business-decision-making-6th-edition-weygandt-test-bank/

Principles of Economics 8th Edition Marshall Test Bank

https://testbankfan.com/product/principles-of-economics-8th-edition-

marshall-test-bank/

3.

Media Essentials 4thEdition Campbell Test Bank

https://testbankfan.com/product/media-essentials-4th-edition-campbell-

test-bank/

Hands-On Ethical Hacking and Network Defense 1st Edition

Simpson Test Bank

https://testbankfan.com/product/hands-on-ethical-hacking-and-network-

defense-1st-edition-simpson-test-bank/

Managerial Economics Foundations of Business Analysis and

Strategy 11th Edition Thomas Test Bank

https://testbankfan.com/product/managerial-economics-foundations-of-

business-analysis-and-strategy-11th-edition-thomas-test-bank/

Marine Biology 10th Edition Castro Solutions Manual

https://testbankfan.com/product/marine-biology-10th-edition-castro-

solutions-manual/

Intermediate Statistics Using SPSS 1st Edition Knapp

Solutions Manual

https://testbankfan.com/product/intermediate-statistics-using-

spss-1st-edition-knapp-solutions-manual/

CHAPTER 10

CURRENT LIABILITIESAND PAYROLL

SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM’S

TAXONOMY

Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT

Exercises

1. 1 AP 6. 1 AP 11. 2 AP 16. 3 AN 21. 5 AN

2. 1 AP 7. 1,3,4 AN 12. 2 AP 17. 4 AP 22. 5 AN

3. 1 AP 8. 2 AP 13. 2,3,4 AN 18. 4 AP *23. 6 AP

4. 1 AP 9. 2 AP 14. 2,5 AP 19. 4 AP *24. 6 AP

5. 1 AP 10. 2 AP 15. 3 E 20. 5 AN *25. 6 AP

Note: AN = Analysis AP = Application E = Evaluation

6.

SUMMARY OF QUESTIONSBY LEVEL OF DIFFICULTY (LOD)

Item SO LOD Item SO LOD Item SO LOD Item SO LOD Item SO LOD

Exercises

1. 1 M 6. 1 M 11. 2 M 16. 3 M 21. 5 E

2. 1 E 7. 1,3,4 E 12. 2 H 17. 4 E 22. 5 E

3. 1 E 8. 2 E 13. 2,3,4 M 18. 4 E *23. 6 H

4. 1 M 9. 2 M 14. 2,5 H 19. 4 M *24. 6 M

5. 1 E 10. 2 M 15. 3 M 20. 5 M *25. 6 M

Note: E = Easy M = Medium H=Hard

7.

CHAPTER STUDY OBJECTIVES

1.Account for determinable or certain current liabilities. Liabilities are present

obligations arising from past events, to make future payments of assets or services.

Determinable liabilities have certainty about their existence, amount, and timing—in

other words, they have a known amount, payee, and due date. Examples of

determinable current liabilities include operating lines of credit, notes payable, accounts

payable, sales taxes, unearned revenue, current maturities of long-term debt, and

accrued liabilities such as property taxes, payroll, and interest.

2. Account for estimated liabilities. Estimated liabilities exist, but their amount or timing

is uncertain. As long as it is likely the company will have to settle the obligation, and the

company can reasonably estimate the amount, the liability is recognized. Product

warranties, customer loyalty programs, and gift cards result in liabilities that must be

estimated. They are recorded either as an expense (or as a decrease in revenue) or a

liability in the period when the sales occur. These liabilities are reduced when repairs

under warranty or redemptions occur. Gift cards are a type of unearned revenue as they

result in a liability until the gift card is redeemed. As some cards are never redeemed, it

is necessary to estimate the liability and make adjustments.

3. Account for contingencies. A contingency is an existing condition or situation that is

uncertain, where it cannot be known if a loss (and a related liability) will result until a

future event happens, or does not happen. Under ASPE, a liability for a contingent loss

is recorded if it is it likely a loss will occur and the amount of the contingency can be

reasonably estimated. Under IFRS, the threshold for recording the loss is lower. It is

recorded if a loss is probable. Under ASPE, these liabilities are called contingent

liabilities, and under IFRS, these liabilities are called provisions. If it is not possible to

estimate the amount, these liabilities are only disclosed. They are not disclosed if they

are unlikely.

4. Determine payroll costs and record payroll transactions. Payroll costs consist of

employee and employer payroll costs. In recording employee costs, Salaries Expense is

debited for the gross pay, individual liability accounts are credited for net pay. In

recording employer payroll costs, Employee Benefits Expense is debited for the

employer’s share of CPP, EI, workers’ compensation, vacation pay, and any other

deductions or benefits provided. Each benefit is credited to its specific current liability

account.

5. Prepare the current liabilities section of the balance sheet. The nature and amount

of each current liability and contingency should be reported in the balance sheet or in the

notes accompanying the financial statements. Traditionally, current liabilities are

reported first and in order of liquidity. International companies sometimes report current

liabilities on the lower section of the balance sheet and in reverse order of liquidity.

8.

6. Calculate mandatorypayroll deductions (Appendix 10A). Mandatory payroll

deductions include CPP, EI, and income taxes. CPP is calculated by multiplying

pensionable earnings (gross pay minus the pay period exemption) by the CPP

contribution rate. EI is calculated by multiplying insurable earnings by the EI contribution

rate. Federal and provincial income taxes are calculated using a progressive tax scheme

and are based on taxable earnings and personal tax credits. The calculations are very

complex and it is best to use one of the CRA income tax calculation tools such as payroll

deduction tables.

9.

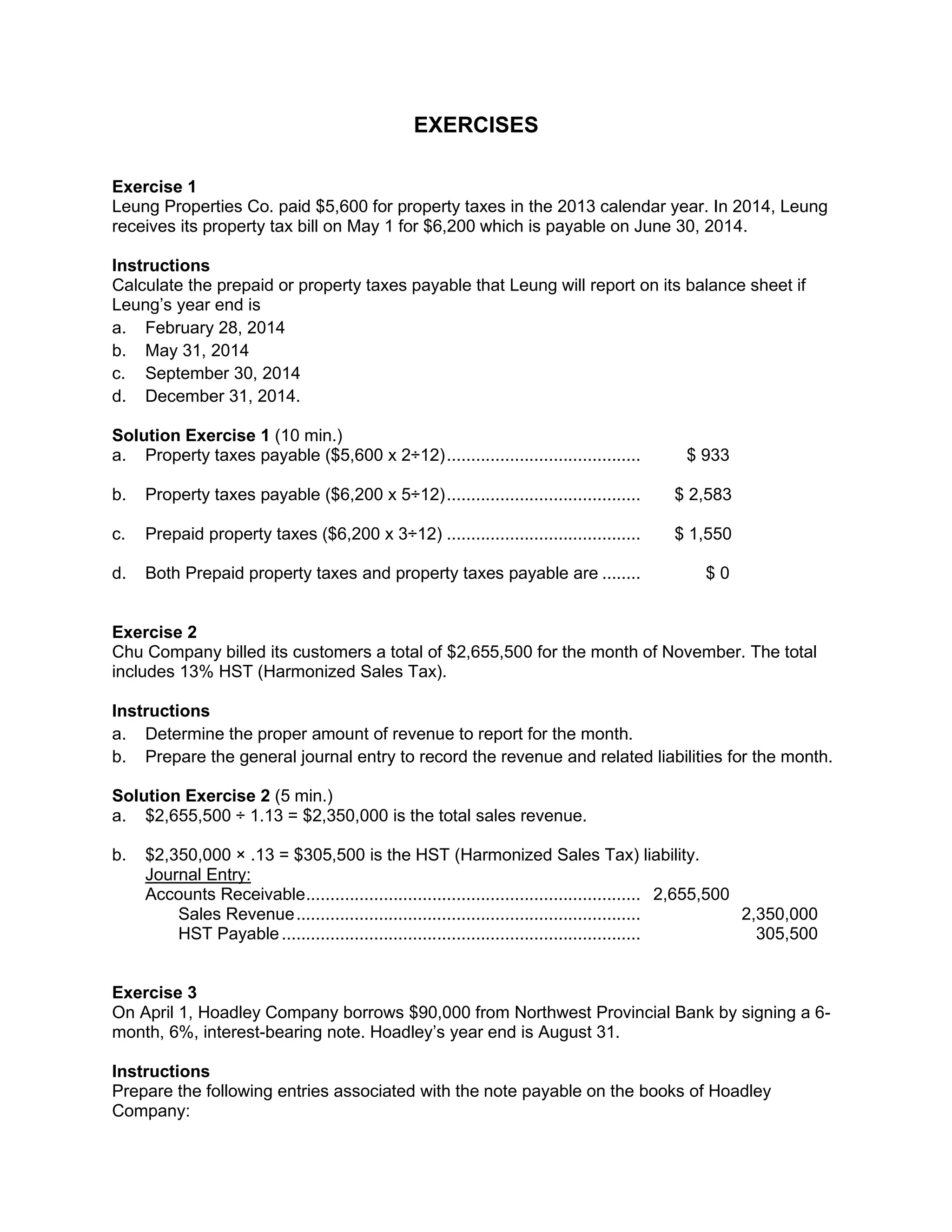

EXERCISES

Exercise 1

Leung PropertiesCo. paid $5,600 for property taxes in the 2013 calendar year. In 2014, Leung

receives its property tax bill on May 1 for $6,200 which is payable on June 30, 2014.

Instructions

Calculate the prepaid or property taxes payable that Leung will report on its balance sheet if

Leung’s year end is

a. February 28, 2014

b. May 31, 2014

c. September 30, 2014

d. December 31, 2014.

Solution Exercise 1 (10 min.)

a. Property taxes payable ($5,600 x 2÷12)........................................ $ 933

b. Property taxes payable ($6,200 x 5÷12)........................................ $ 2,583

c. Prepaid property taxes ($6,200 x 3÷12) ........................................ $ 1,550

d. Both Prepaid property taxes and property taxes payable are ........ $ 0

Exercise 2

Chu Company billed its customers a total of $2,655,500 for the month of November. The total

includes 13% HST (Harmonized Sales Tax).

Instructions

a. Determine the proper amount of revenue to report for the month.

b. Prepare the general journal entry to record the revenue and related liabilities for the month.

Solution Exercise 2 (5 min.)

a. $2,655,500 ÷ 1.13 = $2,350,000 is the total sales revenue.

b. $2,350,000 × .13 = $305,500 is the HST (Harmonized Sales Tax) liability.

Journal Entry:

Accounts Receivable..................................................................... 2,655,500

Sales Revenue....................................................................... 2,350,000

HST Payable.......................................................................... 305,500

Exercise 3

On April 1, Hoadley Company borrows $90,000 from Northwest Provincial Bank by signing a 6-

month, 6%, interest-bearing note. Hoadley’s year end is August 31.

Instructions

Prepare the following entries associated with the note payable on the books of Hoadley

Company:

10.

a. The entryon April 1 when the note was issued.

b. Any adjusting entries necessary on May 31 in order to prepare the quarterly financial

statements. Assume no other interest accrual entries have been made.

c. The adjusting entry at August 31 to accrue interest.

d. The entry to record payment of the note at maturity.

Solution Exercise 3 (10 min.)

a. Apr 1 Cash ............................................................................. 90,000

Notes Payable........................................................ 90,000

b. May 31 Interest Expense ........................................................... 900

Interest Payable ..................................................... 900

($90,000 × 6% × 2÷12)

c. Aug 31 Interest Expense ........................................................... 1,350

Interest Payable ..................................................... 1,350

($90,000 × 6% × 3÷12)

d. Oct 1 Notes Payable............................................................... 90,000

Interest Payable ($900+$1,350) .................................... 2,250

Interest Expense ($90,000 x 6% x 1÷12)....................... 450

Cash....................................................................... 92,700

Exercise 4

Walters Accounting Company receives its annual property tax bill for the calendar year on

May1, 2015. The bill is for $32,000 and payable on June 30, 2015. Walters paid the bill on June

30, 2015. The company prepares quarterly financial statements and had initially estimated that

its 2015 property taxes would be $30,000.

Instructions

Prepare all the required journal entries for 2015 related to the property taxes.

Solution Exercise 4 (15 min.)

Mar 31 Property Tax Expense ($30,000 × 3÷12) ........................... 7,500

Property Tax Payable.................................................. 7,500

Jun 30 Property Tax Expense ($32,000 × 6÷12 - $7,500).............. 8,500

Property Tax Payable ........................................................ 7,500

Prepaid Property Tax ($32,000 x 6÷12) ............................. 16,000

Cash .......................................................................... 32,000

Sep 30 Property Tax Expense ($32,000 × 3÷12) ........................... 8,000

Prepaid Property Tax ................................................. 8,000

Dec 31 Property Tax Expense ($32,000 × 3÷12) ........................... 8,000

Prepaid Property Tax .................................................. 8,000

Exercise 5

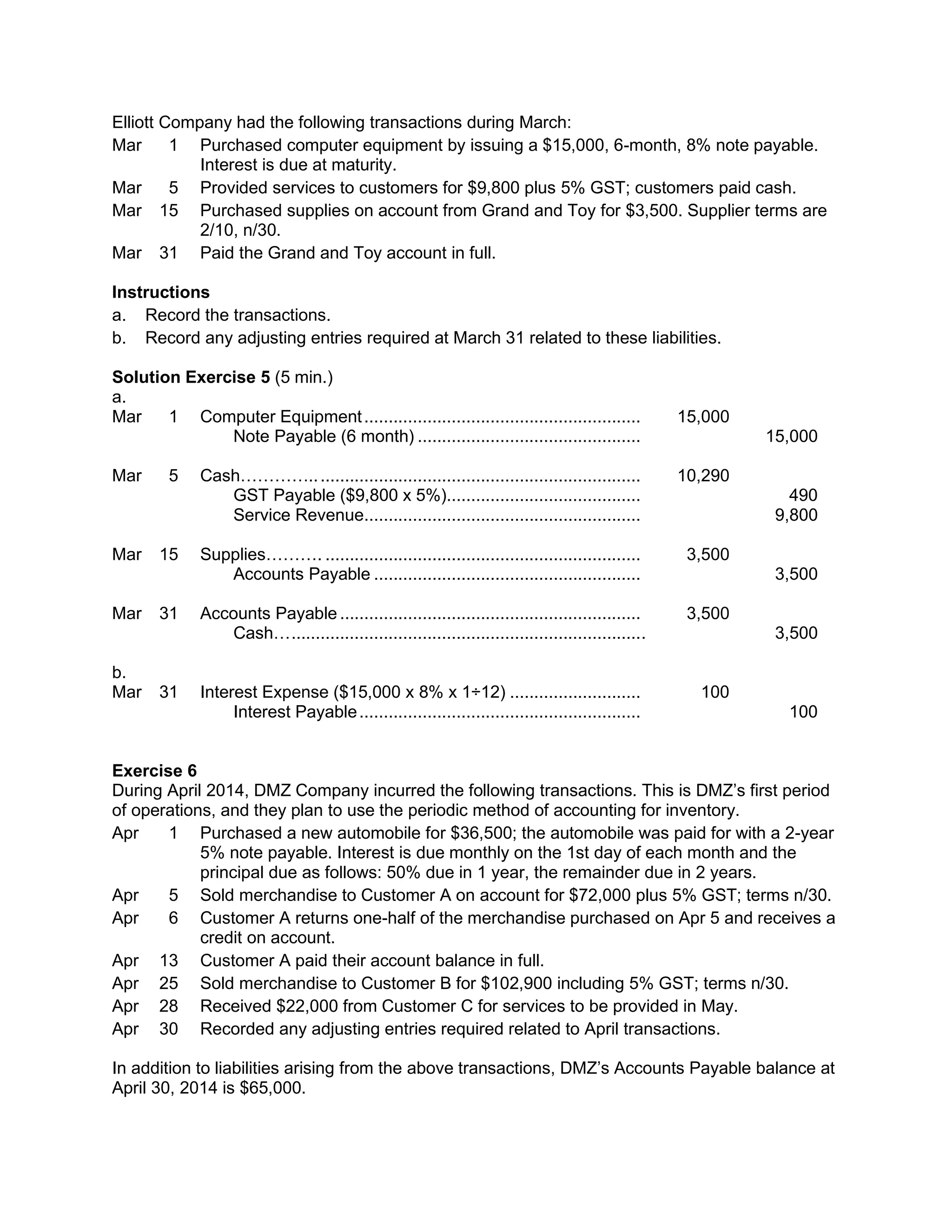

11.

Elliott Company hadthe following transactions during March:

Mar 1 Purchased computer equipment by issuing a $15,000, 6-month, 8% note payable.

Interest is due at maturity.

Mar 5 Provided services to customers for $9,800 plus 5% GST; customers paid cash.

Mar 15 Purchased supplies on account from Grand and Toy for $3,500. Supplier terms are

2/10, n/30.

Mar 31 Paid the Grand and Toy account in full.

Instructions

a. Record the transactions.

b. Record any adjusting entries required at March 31 related to these liabilities.

Solution Exercise 5 (5 min.)

a.

Mar 1 Computer Equipment......................................................... 15,000

Note Payable (6 month) .............................................. 15,000

Mar 5 Cash………….................................................................... 10,290

GST Payable ($9,800 x 5%)........................................ 490

Service Revenue......................................................... 9,800

Mar 15 Supplies………. ................................................................. 3,500

Accounts Payable ....................................................... 3,500

Mar 31 Accounts Payable .............................................................. 3,500

Cash…......................................................................... 3,500

b.

Mar 31 Interest Expense ($15,000 x 8% x 1÷12) ........................... 100

Interest Payable.......................................................... 100

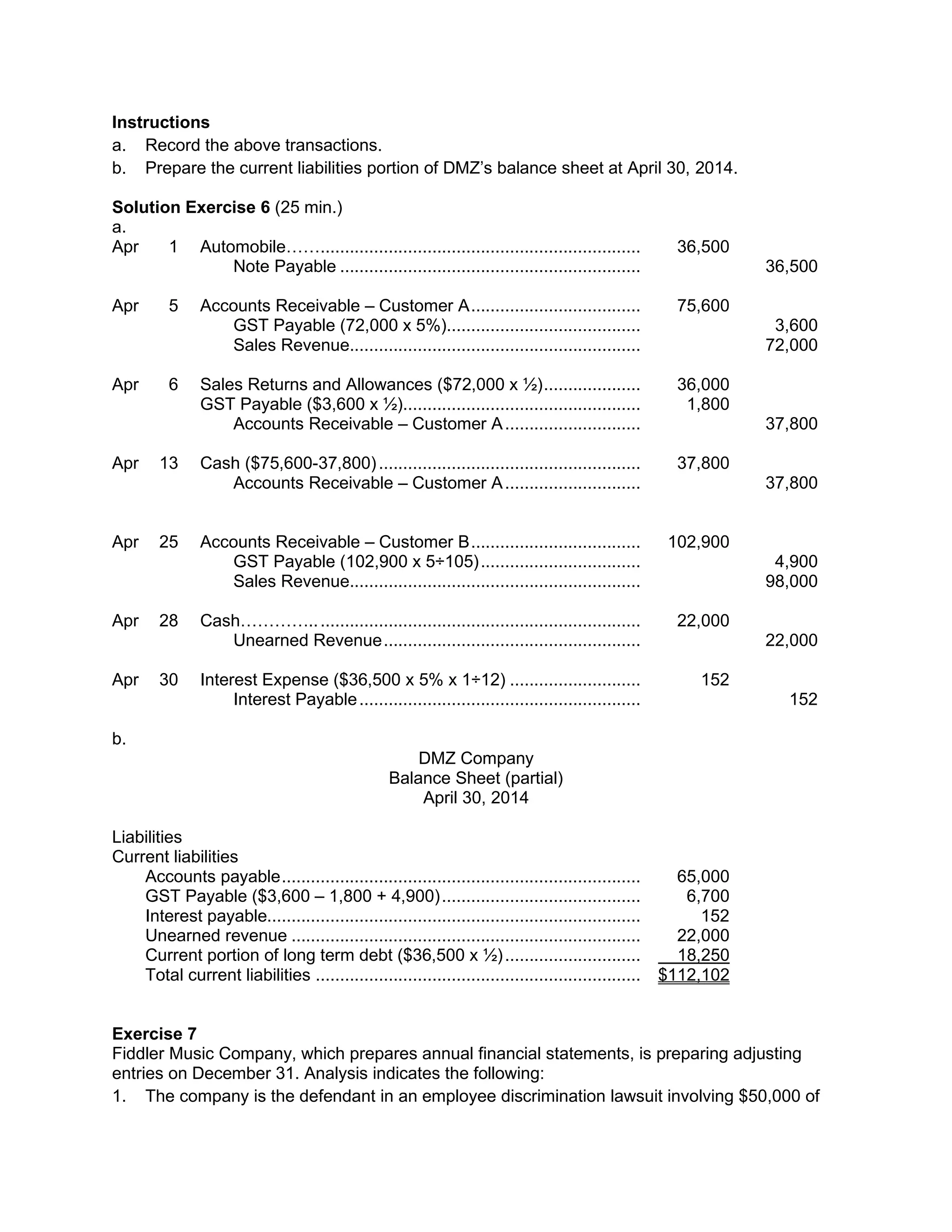

Exercise 6

During April 2014, DMZ Company incurred the following transactions. This is DMZ’s first period

of operations, and they plan to use the periodic method of accounting for inventory.

Apr 1 Purchased a new automobile for $36,500; the automobile was paid for with a 2-year

5% note payable. Interest is due monthly on the 1st day of each month and the

principal due as follows: 50% due in 1 year, the remainder due in 2 years.

Apr 5 Sold merchandise to Customer A on account for $72,000 plus 5% GST; terms n/30.

Apr 6 Customer A returns one-half of the merchandise purchased on Apr 5 and receives a

credit on account.

Apr 13 Customer A paid their account balance in full.

Apr 25 Sold merchandise to Customer B for $102,900 including 5% GST; terms n/30.

Apr 28 Received $22,000 from Customer C for services to be provided in May.

Apr 30 Recorded any adjusting entries required related to April transactions.

In addition to liabilities arising from the above transactions, DMZ’s Accounts Payable balance at

April 30, 2014 is $65,000.

12.

Instructions

a. Record theabove transactions.

b. Prepare the current liabilities portion of DMZ’s balance sheet at April 30, 2014.

Solution Exercise 6 (25 min.)

a.

Apr 1 Automobile…….................................................................. 36,500

Note Payable .............................................................. 36,500

Apr 5 Accounts Receivable – Customer A................................... 75,600

GST Payable (72,000 x 5%)........................................ 3,600

Sales Revenue............................................................ 72,000

Apr 6 Sales Returns and Allowances ($72,000 x ½).................... 36,000

GST Payable ($3,600 x ½)................................................. 1,800

Accounts Receivable – Customer A............................ 37,800

Apr 13 Cash ($75,600-37,800)...................................................... 37,800

Accounts Receivable – Customer A............................ 37,800

Apr 25 Accounts Receivable – Customer B................................... 102,900

GST Payable (102,900 x 5÷105)................................. 4,900

Sales Revenue............................................................ 98,000

Apr 28 Cash………….................................................................... 22,000

Unearned Revenue..................................................... 22,000

Apr 30 Interest Expense ($36,500 x 5% x 1÷12) ........................... 152

Interest Payable.......................................................... 152

b.

DMZ Company

Balance Sheet (partial)

April 30, 2014

Liabilities

Current liabilities

Accounts payable.......................................................................... 65,000

GST Payable ($3,600 – 1,800 + 4,900)......................................... 6,700

Interest payable............................................................................. 152

Unearned revenue ........................................................................ 22,000

Current portion of long term debt ($36,500 x ½)............................ 18,250

Total current liabilities ................................................................... $112,102

Exercise 7

Fiddler Music Company, which prepares annual financial statements, is preparing adjusting

entries on December 31. Analysis indicates the following:

1. The company is the defendant in an employee discrimination lawsuit involving $50,000 of

13.

damages. Legal counselbelieves it is unlikely that the company will have to pay any

damages.

2. December 31st is a Friday. The employees of the company have been paid on Monday,

December 27th for the previous week which ended on Friday, December 24th. The

company employs 30 people who earn $80 per day and 15 people who earn $120 per day.

All employees work 5-day weeks.

3. Employees are entitled to one day's vacation for each month worked. All employees

described above in 2. worked the month of December.

4. The company is a defendant in a $750,000 product liability lawsuit. Legal counsel believes

the company probably will have to pay the amount requested.

5. On November 1, Fiddler signed a $10,000, 6-month, 8% note payable. No interest has

been accrued to date.

Instructions

Prepare any adjusting entries necessary at the end of the year.

Solution Exercise 7 (12 min.)

1. No entry—loss is not likely.

2. Wages Expense............................................................................ 21,000

Wages Payable ...................................................................... 21,000

30 × $80 × 5 = $12,000

15 × $120 × 5 = 9,000

$21,000

3. Vacation Benefits Expense ........................................................... 4,200

Vacation Benefits Payable [(30 × $80) + (15 × $120)] ............ 4,200

4. Loss from Lawsuit ......................................................................... 750,000

Estimated Liability from Lawsuit ............................................. 750,000

5. Interest Expense ($10,000 × 8% × 2 ÷ 12) .................................... 133

Interest Payable ..................................................................... 133

Exercise 8

During the month of July, Toys to Go started a new promotion. The company offered to reward

their customers for all sales made on Barbie dolls or Toy Trucks during the month of July. For

each sale made, the customer will receive a 1% reward of the sales price which can be

redeemed on future purchases until December of the current year. During the month of July,

$250,000 of Barbie dolls and Toy Trucks were sold. There was $755 worth of redemptions in

August.

Instructions

a. Prepare the journal entries to record all transactions related to the reward promotion.

b. Identify any liabilities that would be reported on the August 31, 2014 balance sheet.

Solution Exercise 8 (10 min.)

a. July 31 Sales Discounts for Redemption Rewards Issued ......... 2,500

Redemption Rewards Liability ................................ 2,500

14.

(250,000 x .01)

Aug31 Redemption Rewards Liability ....................................... 755

Cash....................................................................... 755

b. Redemption Reward Liability ($2,500-755).................................... $1,745

Exercise 9

The following situations are independent:

1. During the Christmas season, Betty’s Spa sold $15,000 worth of gift certificates for spa

treatments. In accordance with Canadian legislation, these gift certificates have no expiry

date. During the first year, 75% of the gift certificates are redeemed by customers.

2. Bill’s Car Service sells coupon books for oil changes. The books sell for $300 and include

10 coupons. Without a coupon, the price of an oil change is $35. During the first year of the

coupon book sales, Bill’s sold 200 books, and by the end of the year, 400 coupons had

been claimed. According to Bill’s research, 90% of coupons will eventually be claimed. The

coupons have no expiry date.

Instructions

For each situation, calculate the related liability at the end of the first year.

Solution Exercise 9 (10 min.)

1. Total liability .................................................................................. $ 15,000

Less amounts claimed ($15,000 x 75%)........................................ 11,250

Remaining liability ......................................................................... $ 3,750

2. Total liability for coupons sold (200 books x 10 coupons x $35) .... $70,000

Less 10% will remain unclaimed ................................................... 7,000

Net……………............................................................................... 63,000

Less coupons already claimed (400 x $35) ................................... 14,000

Remaining liability ......................................................................... $ 49,000

Exercise 10

Duane Herman sells exercise machines for home use. The machines carry a 4-year warranty.

Past experience indicates that 6% of the units sold will be returned during the warranty period

for repairs. The average cost of repairs under warranty is $45 for labour and $75 for parts per

unit. During 2015, 2,500 exercise machines were sold at an average price of $800. During the

year, 60 of the machines that were sold were repaired at the average price per unit. The

opening balance in the Warranty Liability account is zero.

Instructions

a. Prepare the journal entry to record the repairs made under warranty.

b. Prepare the journal entry to record the estimated warranty expense for the year. Determine

the balance in the Warranty Liability account at the end of the year.

Solution Exercise 10 (10 min.)

15.

a. Labour onrepaired units: $45 × 60 = $2,700

Parts on repaired units: $75 × 60 = $4,500

Warranty Liability........................................................................... 7,200

Repair Parts ........................................................................... 4,500

Wages Payable ...................................................................... 2,700

To record honouring of 60 warranty contracts

b. 2,500 units × 6% = 150 units

150 units × ($45+$75) = $18,000

Warranty Expense......................................................................... 18,000

Warranty Liability.................................................................... 18,000

To record estimated cost of honouring 150 warranty contracts

The balance in Warranty Liability at year end is $10,800 ($18,000 – $7,200), which equals the

expected cost of honouring the 90 remaining warranty contracts.

Exercise 11

Hardin Manufacturing began operations in January 2014. Hardin manufactures and sells two

different computer monitors.

Monitor A, is a flat panel hi-definition monitor, which carries a two-year manufacturer's warranty

against defects in workmanship. Hardin's management project that 8% of the monitors will

require repair during the first year of the warranty while approximately 6% will require repair

during the second year of the warranty. Monitor A sells for $400. The average cost to repair a

monitor is $80.

Monitor B is a regular LED monitor that retails for $150. Hardin has entered into an agreement

with a local electronics firm who charges Hardin $20 per monitor sold and then covers all

warranty costs related to this monitor.

Sales and warranty information for 2014 is as follows:

Sold 2,000 monitors (800 monitor A and 1,200 monitor B); all sales were on account.

Actual warranty expenditures for monitor A were $4,000.

Instructions

a. Prepare journal entries that summarize the sales and any aspects of the warranty for 2014.

b. Determine the balance in the Warranty Liability account at the end of 2014.

Solution Exercise 11 (5 min.)

a. To record sales

Accounts Receivable..................................................................... 500,000

Sales Revenue—A (800 × $400)............................................ 320,000

Sales Revenue—B (1,200 × $150)......................................... 180,000

Related to the cost of the maintenance contract on monitor B

Warranty Expense (1,200 × $20)................................................... 24,000

Cash....................................................................................... 24,000

16.

To estimate costof warranty on monitor A

Warranty Expense (800 × 14% × $80) .......................................... 8,960

Warranty Liability.................................................................... 8,960

To record actual warranty costs on monitor A

Warranty Liability........................................................................... 4,000

Cash....................................................................................... 4,000

b. $8,960 – $4,000 = $4,960

Exercise 12

During the year, Canada Ski Cross Ltd. instituted a customer rewards program. The company

sells skis which are specially used for the latest type of skiing, ski cross. For every $250 of ski

cross equipment purchased by a customer, the company will rebate $50 towards the cost of

purchasing a ski cross helmet. In January, the company had ski cross equipment sales of

$64,000. There were no helmets purchased. In February, there were sales of $32,600 and there

were 135 helmets sold.

Instructions

a. Prepare journal entries for January. What is the ending balance in the liability account for

the end of January?

b. Prepare journal entries for February. What is the ending balance in the liability account for

the end of February?

Solution Exercise 12 (10-13 min.)

a. January Entries

Cash ............................................................................................. $64,000

Sales...................................................................................... $64,000

Sales Discounts for Redemption Rewards .................................... 12,800

Redemptions Rewards Liability .............................................. 12,800

($64,000 ÷ $250 x $50)

Liability end of January = $12,800

b. February Entries

Cash ............................................................................................. $32,600

Sales...................................................................................... $32,600

Sales Discounts for Redemption Rewards .................................... 6,520

Redemptions Rewards Liability .............................................. 6,520

($32,600 ÷ $250 x $50)

Redemptions Rewards Liability ..................................................... 6,750

Cash....................................................................................... 6,750

(135 x 50)

Liability end of February ($12,800 + $6,520 – $6,750) = $12,570

17.

Exercise 13

Milner Companyis preparing adjusting entries at December 31. An analysis reveals the

following:

1. During December, Milner Company sold 4,900 units of a product that carries a 60-day

warranty. The sales for this product totalled $100,000. The company expects 6% of the

units to need repair under the warranty and it estimates that the average repair cost per unit

will be $15.

2. The company has been sued by a disgruntled employee. Legal counsel believes it is likely

that the company will have to pay $200,000 in damages.

3. The company has been named as one of several defendants in a $400,000 damage suit.

Legal counsel believes it is unlikely that the company will have to pay any damages.

4. During December, ten employees earn vacation pay at a rate of 1 day per month. Their

average daily wage is $100 per employee.

Instructions

Prepare adjusting entries, if required, for each of the four items.

Solution Exercise 13 (10 min.)

1. 4,900 units × 6% = 294 units expected to be defective.

294 units × $15 = $4,410

Warranty Expense......................................................................... 4,410

Warranty Liability.................................................................... 4,410

2. An entry is required because the loss is likely and estimable.

Loss from Lawsuit ......................................................................... 200,000

Estimated Liability from Lawsuit ............................................. 200,000

3. The loss is unlikely and does not require accrual or disclosure. No entry is required.

4. 10 employees × $100 × 1 day = $1,000.

Vacation Benefits Expense ........................................................... 1,000

Vacation Benefits Payable...................................................... 1,000

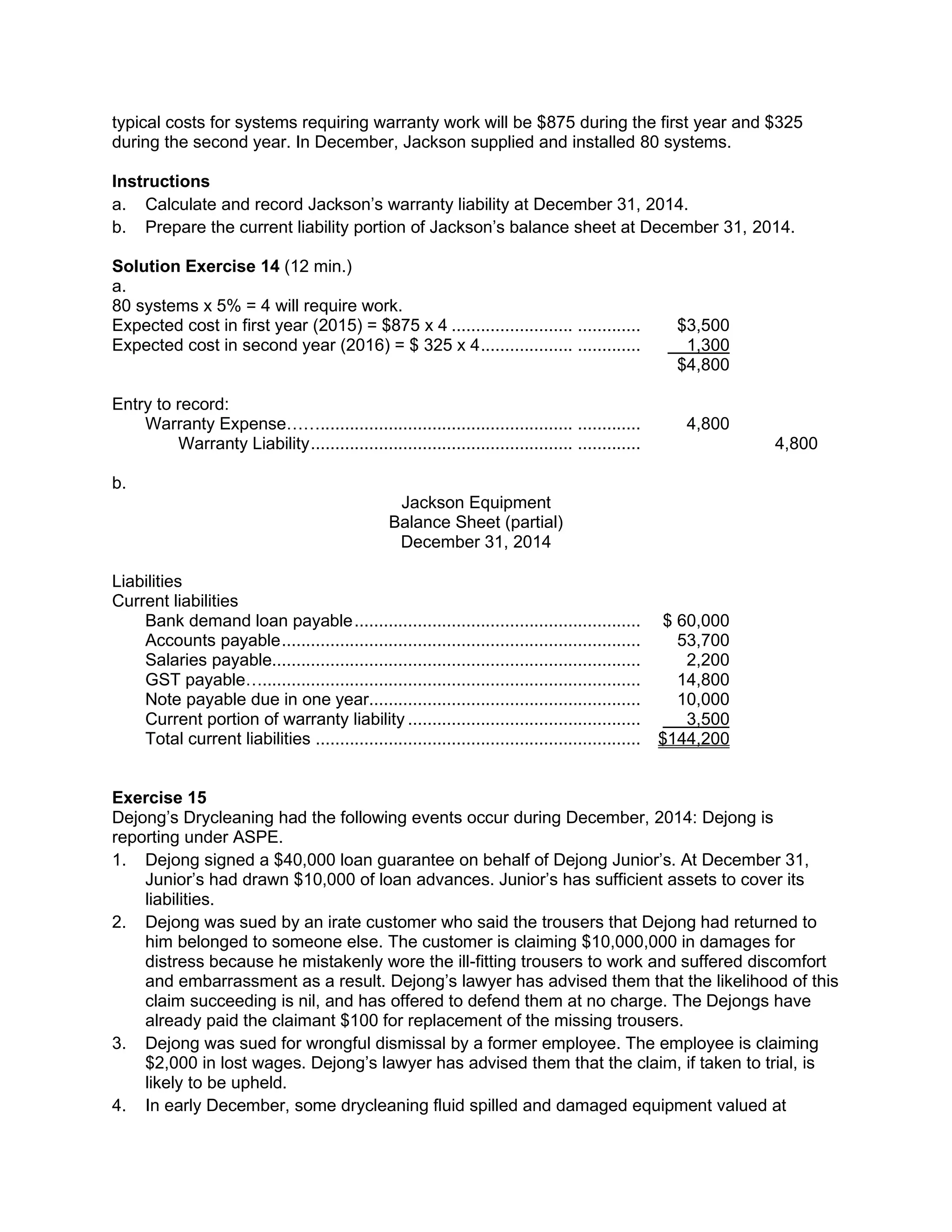

Exercise 14

The following unadjusted balances are taken from the trial balance of Jackson Equipment at

December 31, 2014:

Accounts payable…………............................................................ $ 53,700

Salaries payable………................................................................. 2,200

Bank demand loan payable........................................................... 60,000

GST payable…………… ............................................................... 14,800

Note payable, maturing March 31, 2015........................................ 10,000

Note payable, maturing March 31, 2016........................................ 100,000

Jackson Equipment sells and installs security systems. Beginning on December 1, 2014,

Jackson began offering a 2-year product warranty. Based on research in the industry, Jackson’s

management believes that 5% of security systems will require some warranty work and that the

18.

typical costs forsystems requiring warranty work will be $875 during the first year and $325

during the second year. In December, Jackson supplied and installed 80 systems.

Instructions

a. Calculate and record Jackson’s warranty liability at December 31, 2014.

b. Prepare the current liability portion of Jackson’s balance sheet at December 31, 2014.

Solution Exercise 14 (12 min.)

a.

80 systems x 5% = 4 will require work.

Expected cost in first year (2015) = $875 x 4 ......................... ............. $3,500

Expected cost in second year (2016) = $ 325 x 4................... ............. 1,300

$4,800

Entry to record:

Warranty Expense…….................................................... ............. 4,800

Warranty Liability...................................................... ............. 4,800

b.

Jackson Equipment

Balance Sheet (partial)

December 31, 2014

Liabilities

Current liabilities

Bank demand loan payable........................................................... $ 60,000

Accounts payable.......................................................................... 53,700

Salaries payable............................................................................ 2,200

GST payable….............................................................................. 14,800

Note payable due in one year........................................................ 10,000

Current portion of warranty liability ................................................ 3,500

Total current liabilities ................................................................... $144,200

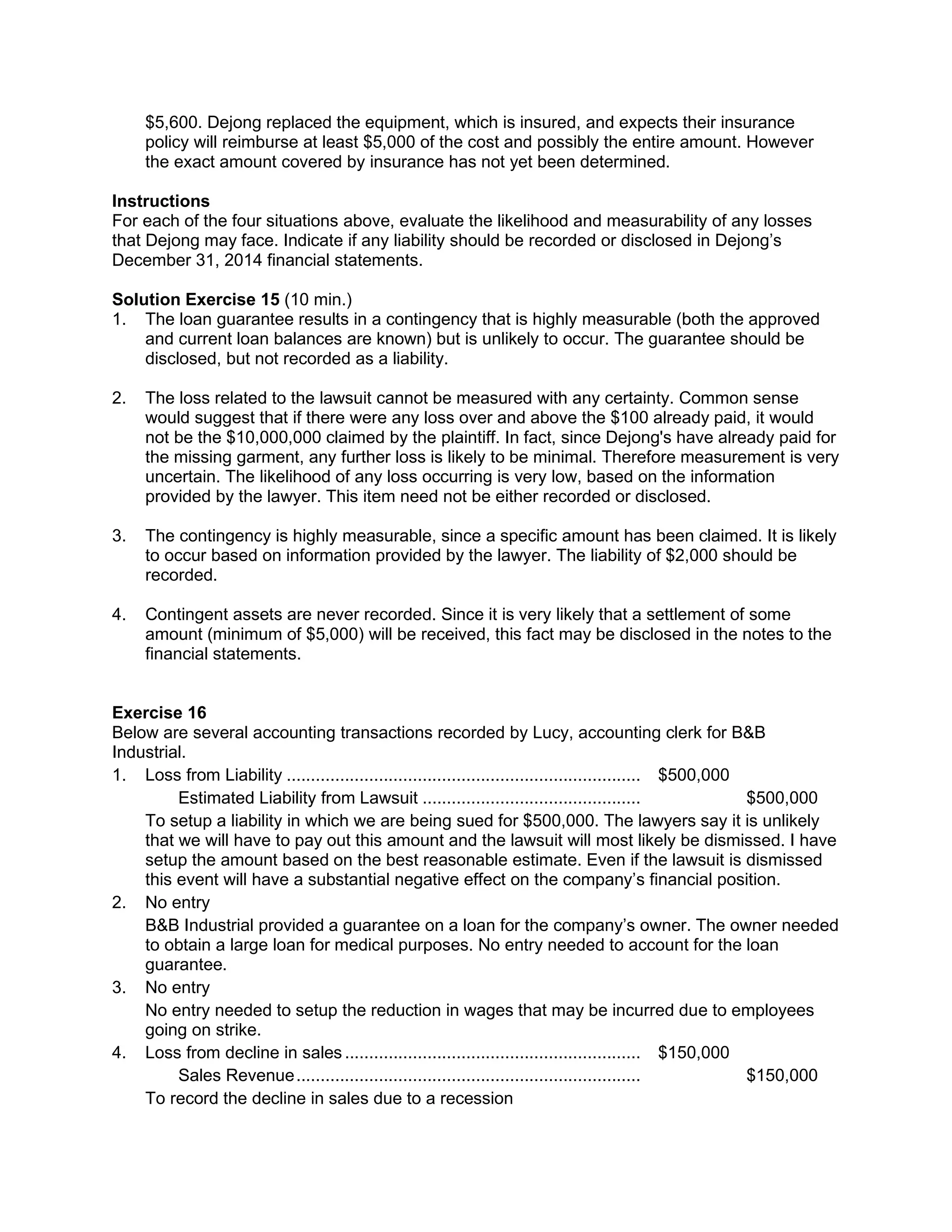

Exercise 15

Dejong’s Drycleaning had the following events occur during December, 2014: Dejong is

reporting under ASPE.

1. Dejong signed a $40,000 loan guarantee on behalf of Dejong Junior’s. At December 31,

Junior’s had drawn $10,000 of loan advances. Junior’s has sufficient assets to cover its

liabilities.

2. Dejong was sued by an irate customer who said the trousers that Dejong had returned to

him belonged to someone else. The customer is claiming $10,000,000 in damages for

distress because he mistakenly wore the ill-fitting trousers to work and suffered discomfort

and embarrassment as a result. Dejong’s lawyer has advised them that the likelihood of this

claim succeeding is nil, and has offered to defend them at no charge. The Dejongs have

already paid the claimant $100 for replacement of the missing trousers.

3. Dejong was sued for wrongful dismissal by a former employee. The employee is claiming

$2,000 in lost wages. Dejong’s lawyer has advised them that the claim, if taken to trial, is

likely to be upheld.

4. In early December, some drycleaning fluid spilled and damaged equipment valued at

19.

$5,600. Dejong replacedthe equipment, which is insured, and expects their insurance

policy will reimburse at least $5,000 of the cost and possibly the entire amount. However

the exact amount covered by insurance has not yet been determined.

Instructions

For each of the four situations above, evaluate the likelihood and measurability of any losses

that Dejong may face. Indicate if any liability should be recorded or disclosed in Dejong’s

December 31, 2014 financial statements.

Solution Exercise 15 (10 min.)

1. The loan guarantee results in a contingency that is highly measurable (both the approved

and current loan balances are known) but is unlikely to occur. The guarantee should be

disclosed, but not recorded as a liability.

2. The loss related to the lawsuit cannot be measured with any certainty. Common sense

would suggest that if there were any loss over and above the $100 already paid, it would

not be the $10,000,000 claimed by the plaintiff. In fact, since Dejong's have already paid for

the missing garment, any further loss is likely to be minimal. Therefore measurement is very

uncertain. The likelihood of any loss occurring is very low, based on the information

provided by the lawyer. This item need not be either recorded or disclosed.

3. The contingency is highly measurable, since a specific amount has been claimed. It is likely

to occur based on information provided by the lawyer. The liability of $2,000 should be

recorded.

4. Contingent assets are never recorded. Since it is very likely that a settlement of some

amount (minimum of $5,000) will be received, this fact may be disclosed in the notes to the

financial statements.

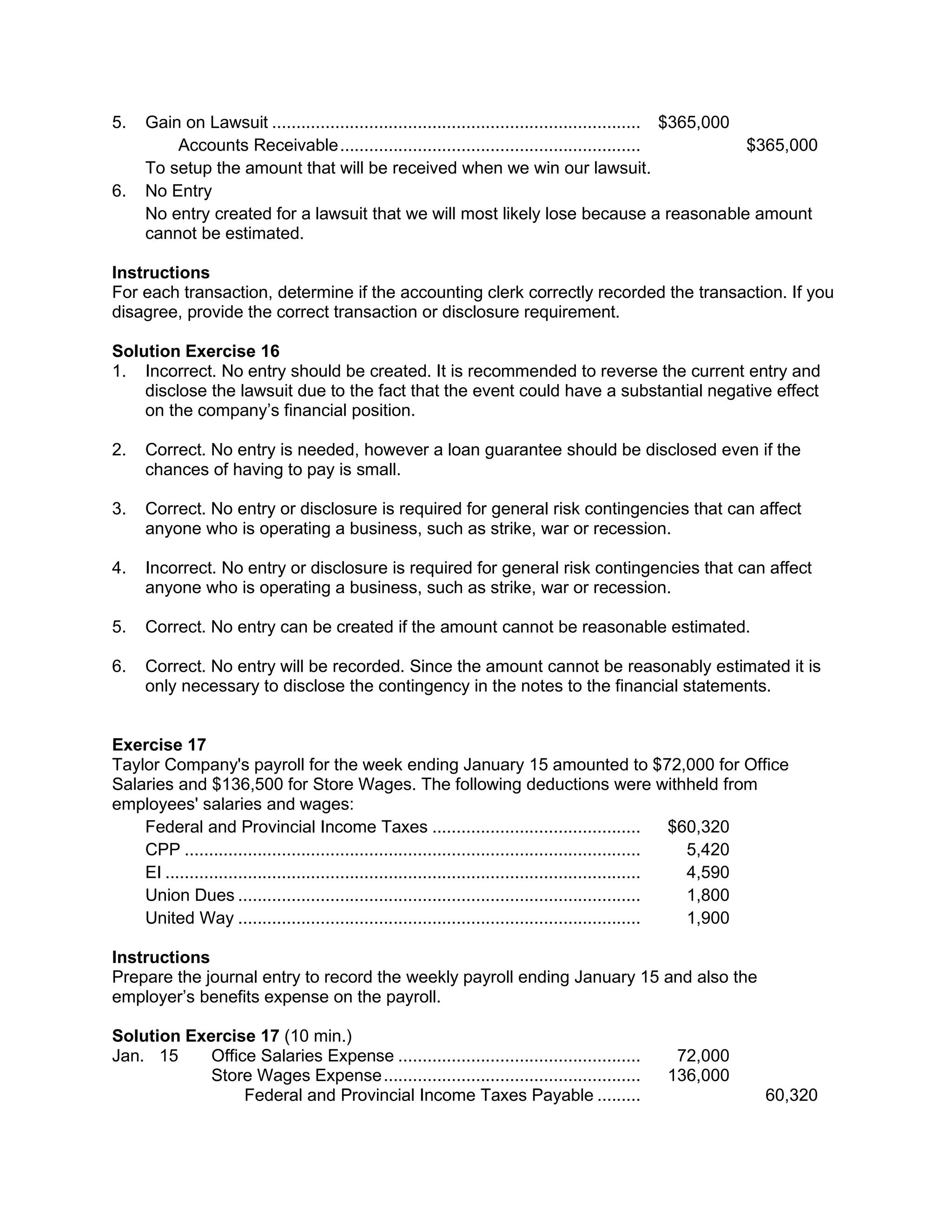

Exercise 16

Below are several accounting transactions recorded by Lucy, accounting clerk for B&B

Industrial.

1. Loss from Liability ......................................................................... $500,000

Estimated Liability from Lawsuit ............................................. $500,000

To setup a liability in which we are being sued for $500,000. The lawyers say it is unlikely

that we will have to pay out this amount and the lawsuit will most likely be dismissed. I have

setup the amount based on the best reasonable estimate. Even if the lawsuit is dismissed

this event will have a substantial negative effect on the company’s financial position.

2. No entry

B&B Industrial provided a guarantee on a loan for the company’s owner. The owner needed

to obtain a large loan for medical purposes. No entry needed to account for the loan

guarantee.

3. No entry

No entry needed to setup the reduction in wages that may be incurred due to employees

going on strike.

4. Loss from decline in sales............................................................. $150,000

Sales Revenue....................................................................... $150,000

To record the decline in sales due to a recession

20.

5. Gain onLawsuit ............................................................................ $365,000

Accounts Receivable.............................................................. $365,000

To setup the amount that will be received when we win our lawsuit.

6. No Entry

No entry created for a lawsuit that we will most likely lose because a reasonable amount

cannot be estimated.

Instructions

For each transaction, determine if the accounting clerk correctly recorded the transaction. If you

disagree, provide the correct transaction or disclosure requirement.

Solution Exercise 16

1. Incorrect. No entry should be created. It is recommended to reverse the current entry and

disclose the lawsuit due to the fact that the event could have a substantial negative effect

on the company’s financial position.

2. Correct. No entry is needed, however a loan guarantee should be disclosed even if the

chances of having to pay is small.

3. Correct. No entry or disclosure is required for general risk contingencies that can affect

anyone who is operating a business, such as strike, war or recession.

4. Incorrect. No entry or disclosure is required for general risk contingencies that can affect

anyone who is operating a business, such as strike, war or recession.

5. Correct. No entry can be created if the amount cannot be reasonable estimated.

6. Correct. No entry will be recorded. Since the amount cannot be reasonably estimated it is

only necessary to disclose the contingency in the notes to the financial statements.

Exercise 17

Taylor Company's payroll for the week ending January 15 amounted to $72,000 for Office

Salaries and $136,500 for Store Wages. The following deductions were withheld from

employees' salaries and wages:

Federal and Provincial Income Taxes ........................................... $60,320

CPP .............................................................................................. 5,420

EI .................................................................................................. 4,590

Union Dues ................................................................................... 1,800

United Way ................................................................................... 1,900

Instructions

Prepare the journal entry to record the weekly payroll ending January 15 and also the

employer’s benefits expense on the payroll.

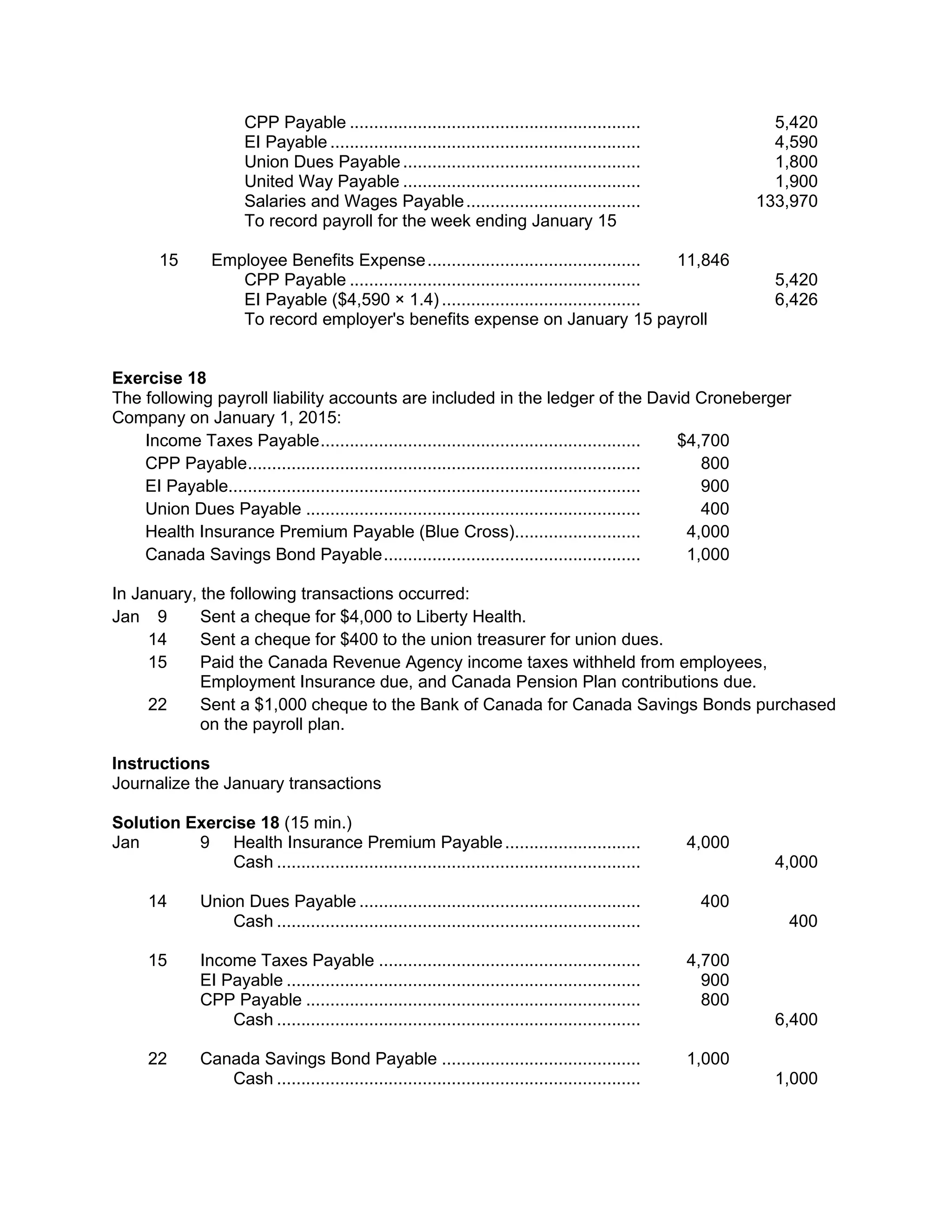

Solution Exercise 17 (10 min.)

Jan. 15 Office Salaries Expense .................................................. 72,000

Store Wages Expense..................................................... 136,000

Federal and Provincial Income Taxes Payable ......... 60,320

21.

CPP Payable ............................................................5,420

EI Payable ................................................................ 4,590

Union Dues Payable................................................. 1,800

United Way Payable ................................................. 1,900

Salaries and Wages Payable.................................... 133,970

To record payroll for the week ending January 15

15 Employee Benefits Expense............................................ 11,846

CPP Payable ............................................................ 5,420

EI Payable ($4,590 × 1.4) ......................................... 6,426

To record employer's benefits expense on January 15 payroll

Exercise 18

The following payroll liability accounts are included in the ledger of the David Croneberger

Company on January 1, 2015:

Income Taxes Payable.................................................................. $4,700

CPP Payable................................................................................. 800

EI Payable..................................................................................... 900

Union Dues Payable ..................................................................... 400

Health Insurance Premium Payable (Blue Cross).......................... 4,000

Canada Savings Bond Payable..................................................... 1,000

In January, the following transactions occurred:

Jan 9 Sent a cheque for $4,000 to Liberty Health.

14 Sent a cheque for $400 to the union treasurer for union dues.

15 Paid the Canada Revenue Agency income taxes withheld from employees,

Employment Insurance due, and Canada Pension Plan contributions due.

22 Sent a $1,000 cheque to the Bank of Canada for Canada Savings Bonds purchased

on the payroll plan.

Instructions

Journalize the January transactions

Solution Exercise 18 (15 min.)

Jan 9 Health Insurance Premium Payable............................ 4,000

Cash ........................................................................... 4,000

14 Union Dues Payable .......................................................... 400

Cash ........................................................................... 400

15 Income Taxes Payable ...................................................... 4,700

EI Payable ......................................................................... 900

CPP Payable ..................................................................... 800

Cash ........................................................................... 6,400

22 Canada Savings Bond Payable ......................................... 1,000

Cash ........................................................................... 1,000

22.

Exercise 19

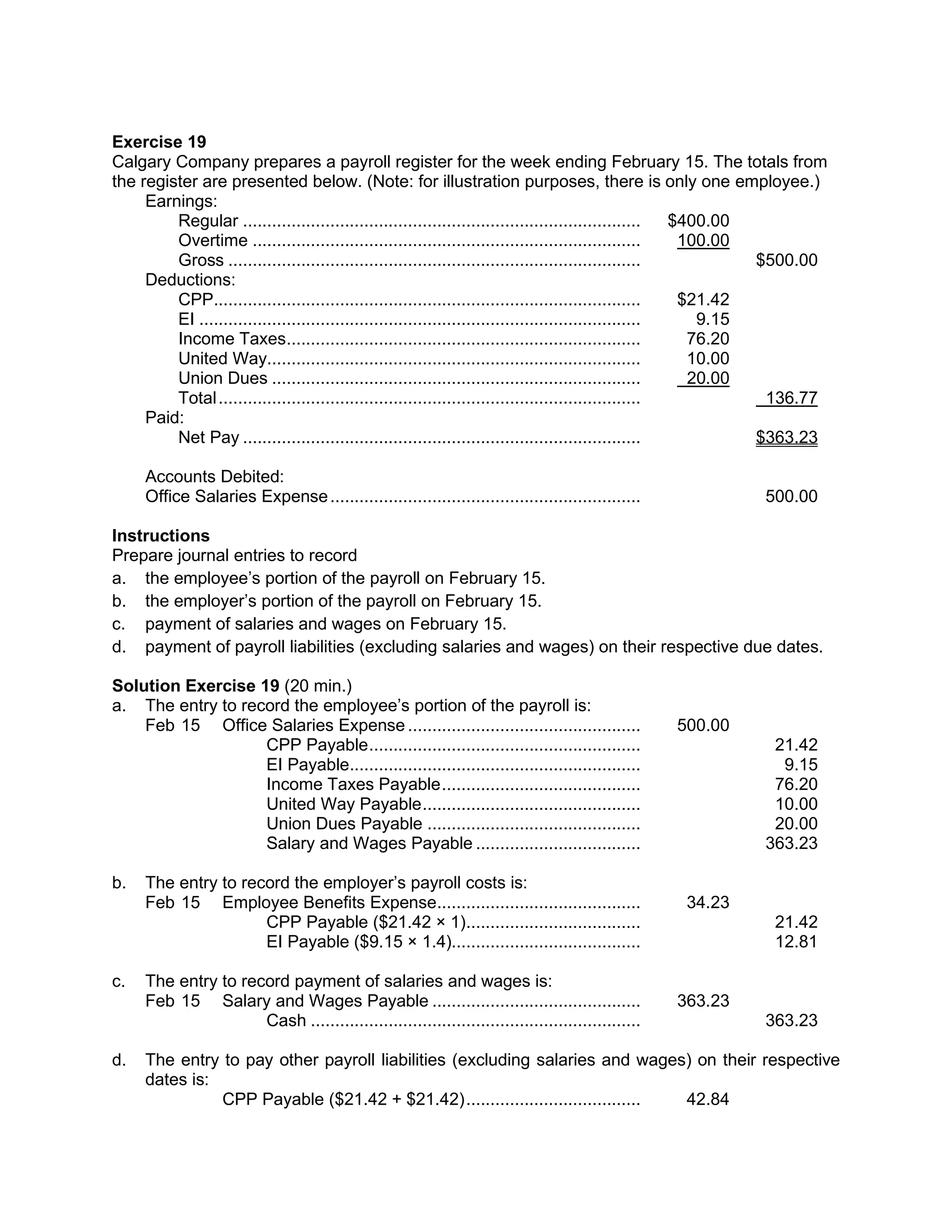

Calgary Companyprepares a payroll register for the week ending February 15. The totals from

the register are presented below. (Note: for illustration purposes, there is only one employee.)

Earnings:

Regular .................................................................................. $400.00

Overtime ................................................................................ 100.00

Gross ..................................................................................... $500.00

Deductions:

CPP........................................................................................ $21.42

EI ........................................................................................... 9.15

Income Taxes......................................................................... 76.20

United Way............................................................................. 10.00

Union Dues ............................................................................ 20.00

Total....................................................................................... 136.77

Paid:

Net Pay .................................................................................. $363.23

Accounts Debited:

Office Salaries Expense................................................................ 500.00

Instructions

Prepare journal entries to record

a. the employee’s portion of the payroll on February 15.

b. the employer’s portion of the payroll on February 15.

c. payment of salaries and wages on February 15.

d. payment of payroll liabilities (excluding salaries and wages) on their respective due dates.

Solution Exercise 19 (20 min.)

a. The entry to record the employee’s portion of the payroll is:

Feb 15 Office Salaries Expense ................................................ 500.00

CPP Payable........................................................ 21.42

EI Payable............................................................ 9.15

Income Taxes Payable......................................... 76.20

United Way Payable............................................. 10.00

Union Dues Payable ............................................ 20.00

Salary and Wages Payable .................................. 363.23

b. The entry to record the employer’s payroll costs is:

Feb 15 Employee Benefits Expense.......................................... 34.23

CPP Payable ($21.42 × 1).................................... 21.42

EI Payable ($9.15 × 1.4)....................................... 12.81

c. The entry to record payment of salaries and wages is:

Feb 15 Salary and Wages Payable ........................................... 363.23

Cash .................................................................... 363.23

d. The entry to pay other payroll liabilities (excluding salaries and wages) on their respective

dates is:

CPP Payable ($21.42 + $21.42).................................... 42.84

23.

EI Payable ($9.15+ $12.81).......................................... 21.96

Income Tax Payable...................................................... 76.20

United Way Payable...................................................... 10.00

Union Dues Payable...................................................... 20.00

Cash .................................................................... 171.00

Exercise 20

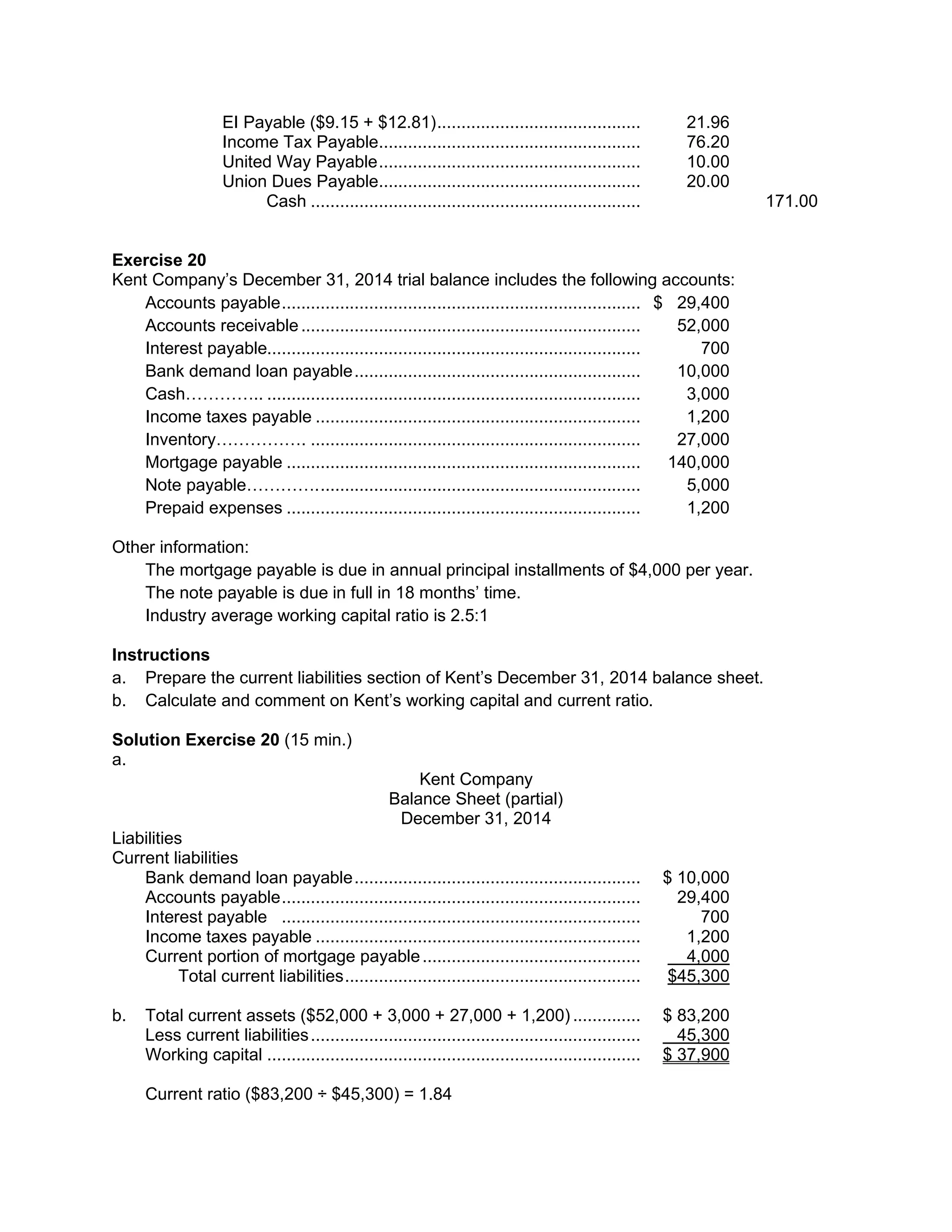

Kent Company’s December 31, 2014 trial balance includes the following accounts:

Accounts payable.......................................................................... $ 29,400

Accounts receivable...................................................................... 52,000

Interest payable............................................................................. 700

Bank demand loan payable........................................................... 10,000

Cash………….. ............................................................................. 3,000

Income taxes payable ................................................................... 1,200

Inventory……………. .................................................................... 27,000

Mortgage payable ......................................................................... 140,000

Note payable…………................................................................... 5,000

Prepaid expenses ......................................................................... 1,200

Other information:

The mortgage payable is due in annual principal installments of $4,000 per year.

The note payable is due in full in 18 months’ time.

Industry average working capital ratio is 2.5:1

Instructions

a. Prepare the current liabilities section of Kent’s December 31, 2014 balance sheet.

b. Calculate and comment on Kent’s working capital and current ratio.

Solution Exercise 20 (15 min.)

a.

Kent Company

Balance Sheet (partial)

December 31, 2014

Liabilities

Current liabilities

Bank demand loan payable........................................................... $ 10,000

Accounts payable.......................................................................... 29,400

Interest payable .......................................................................... 700

Income taxes payable ................................................................... 1,200

Current portion of mortgage payable............................................. 4,000

Total current liabilities............................................................. $45,300

b. Total current assets ($52,000 + 3,000 + 27,000 + 1,200) .............. $ 83,200

Less current liabilities.................................................................... 45,300

Working capital ............................................................................. $ 37,900

Current ratio ($83,200 ÷ $45,300) = 1.84

24.

Calculating Kent’s workingcapital of $37,900 does not provide significant meaningful

information since one cannot compare a monetary amount to those of companies of different

sizes. By using a ratio such as the current ratio, one can compare Kent to other companies and

to the industry average. Although Kent has a positive working capital, its current ratio is less

than the industry average, suggesting Kent has less liquidity than most of its competitors.

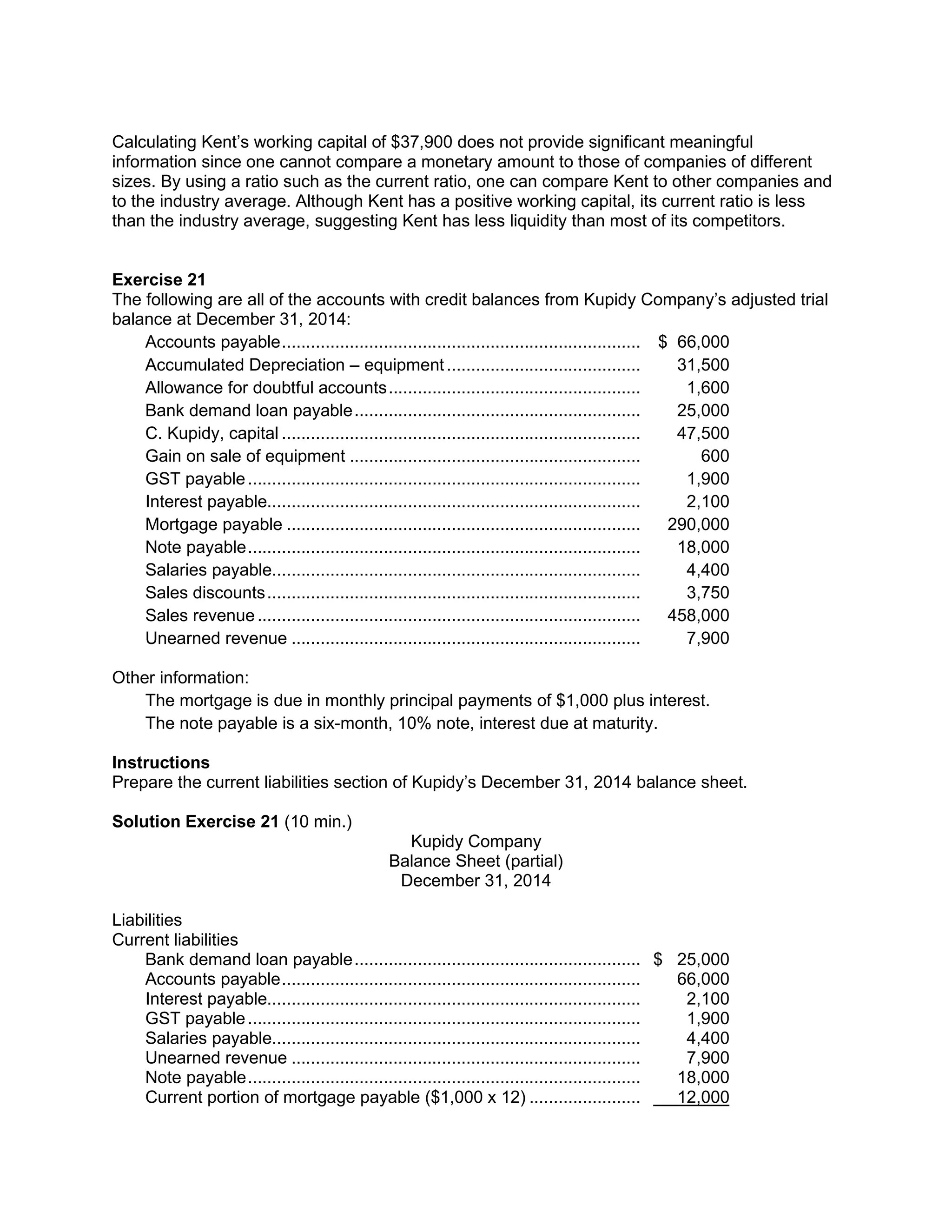

Exercise 21

The following are all of the accounts with credit balances from Kupidy Company’s adjusted trial

balance at December 31, 2014:

Accounts payable.......................................................................... $ 66,000

Accumulated Depreciation – equipment........................................ 31,500

Allowance for doubtful accounts.................................................... 1,600

Bank demand loan payable........................................................... 25,000

C. Kupidy, capital .......................................................................... 47,500

Gain on sale of equipment ............................................................ 600

GST payable................................................................................. 1,900

Interest payable............................................................................. 2,100

Mortgage payable ......................................................................... 290,000

Note payable................................................................................. 18,000

Salaries payable............................................................................ 4,400

Sales discounts............................................................................. 3,750

Sales revenue............................................................................... 458,000

Unearned revenue ........................................................................ 7,900

Other information:

The mortgage is due in monthly principal payments of $1,000 plus interest.

The note payable is a six-month, 10% note, interest due at maturity.

Instructions

Prepare the current liabilities section of Kupidy’s December 31, 2014 balance sheet.

Solution Exercise 21 (10 min.)

Kupidy Company

Balance Sheet (partial)

December 31, 2014

Liabilities

Current liabilities

Bank demand loan payable........................................................... $ 25,000

Accounts payable.......................................................................... 66,000

Interest payable............................................................................. 2,100

GST payable................................................................................. 1,900

Salaries payable............................................................................ 4,400

Unearned revenue ........................................................................ 7,900

Note payable................................................................................. 18,000

Current portion of mortgage payable ($1,000 x 12) ....................... 12,000

you and me.They think that I am part owner. I let them think so,

but you and I know better, Jack." He nodded his head looking

mighty cunning.

"She cannot be too wealthy or too prosperous, captain. I knew full

well that her prosperity only increases the gulf between us, but I

had long ago understood that such an heiress was not for a mate on

board a merchantman."

"She is not, Jack," the captain replied, gravely. "Already she is the

richest heiress in all Norfolk—perhaps in the whole country. Who is

to marry her? There, I confess, I am at a loss. I must find a husband

for her. There's the rub. She may marry any in the land: there is

none so high but he would desire a wife so rich and so virtuous.

Where shall I look for a husband fit for her? There are admirals, but

mostly too old for her: she ought to have a noble lord, yet, if all

tales be true, they are not fit, most of them to marry a virtuous

woman. Shall I give Molly to a man who gambles and drinks and

rakes and riots? No, Jack, no. Not for twenty coronets. I would

rather marry her to an honest sailor like yourself. Jack, my lad, find

me a noble lord, as like yourself as one pea is like another, and he

shall have her. He must be as proper a man; as strong a man; a

clean liver; moderate in his cups … find him for me, Jack, and he

shall have her."

"Well, but, captain, there are the gentlemen of Norfolk."

"Ay…. There are—as you say—the gentlemen. I have considered

them, Jack. Molly is not a gentlewoman by birth, I know that very

well: but her fortune entitles her to marry in a higher rank. Ay …

there are the gentlemen. They are good fox hunters: they are good

at horse racing, but they are hard drinkers, Jack: they are fuddled

most evenings: my little maid must not have a husband who is put

to bed drunk every night."

"You must take her to London, captain, and let her be seen."

27.

"Ay—ay … ifI only knew where to go and how to begin."

"She is young; there is no need for hurry: you can wait awhile,

captain."

"Ay … we can wait a while. I shall be loth to let her go, God knows

—— Come to-morrow, Jack. She was always fond of you: she talks

about you: 'tis a loving little maid: you played with her and ran

about with her. She never forgets. The next command that falls in—

but I talk too fast. Well—when there is a ship in her fleet without a

captain—— But come, my lad."

He led the way, still talking of his ward and her perfections, through

the narrow street they call Stath Lane into the great market place,

where stands the Crown Inn.

The room appropriated to the "Society of Lynn," which met every

evening all the year round, was that on the ground floor looking

upon the market place. The "society," or club, which is never

dissolved, consists of the notables or better sort of the town: the

vicar of St. Margaret's; the curate of St. Nicholas; the master of the

school—my own father: Captain Crowle and other retired captains;

the doctor; some of the more substantial merchants; with the mayor,

some of the aldermen, the town clerk, and a justice of the peace or

two. This evening most of these gentlemen were already present.

Captain Crowle saluted the company and took his seat at the head

of the table. "Gentlemen," he said, "I wish you all a pleasant

evening. I have brought with me my young friend Jack Pentecrosse

—you all know Jack—the worthy son of his worthy father. He will

take a glass with us. Sit down beside me, Jack."

"With the permission of the society," I said.

Most of the gentlemen had already before them their pipes and their

tobacco. Some had ordered their drink—a pint of port for one: a

Brown George full of old ale for another; a flask of Canary for a

28.

third: and soon. But the captain, looking round the room, beckoned

to the girl who waited. "Jenny," he said, "nobody calls for anything

to-night except myself. Gentlemen, it must be a bowl—or a half

dozen bowls. Tell your mistress, Jenny, a bowl of the biggest and the

strongest and the sweetest. Gentlemen, you will drink with me to

the next voyage of The Lady of Lynn."

But then a thing happened—news came—which drove all thoughts

of The Lady of Lynn out of everybody's mind. That toast was

forgotten.

The news was brought by the doctor, who was the last to arrive.

It was an indication of the importance of our town that a physician

lived among us. He was the only physician in this part of the

country: he practised among the better sort, among the noble

gentlemen of the country round about Lynn and even further afield

in the northern parts of the shire, and among the substantial

merchants of the town. For the rest there were the apothecary, the

barber and blood-letter, the bone-setter, the herbalist and the wise

woman. Many there were even among the better sort who would

rather consult the woman, who knew the powers of every herb that

grows, than the physician who would write you out the prescription

of Mithridates or some other outlandish name composed of sixty or

seventy ingredients. However, there is no doubt that learning is a

fine thing and that Galen knew more than the ancient dames who sit

in a bower of dried herbs and brew them into nauseous drinks which

pretend to cure all the diseases to which mankind is liable.

Doctor Worship was a person who habitually carried himself with

dignity. His black dress, his white silk stockings, his gold shoe

buckles, the whiteness of his lace and linen, his huge wig, his gold-

headed cane with its pomander, proclaimed his calling, while the

shortness of his stature with the roundness of his figure, his double

chin, his thick lips and his fat nose all assisted him in the

maintenance of his dignity. His voice was full and deep, like the voice

29.

of an organand he spoke slowly. It has, I believe, been remarked

that dignity is more easily attained by a short fat man than by one of

a greater stature and thinner person.

At the very first appearance of the doctor this evening it was

understood that something had happened. For he had assumed an

increased importance that was phenomenal: he had swollen, so to

speak: he had become rounder and fuller in front. Everybody

observed the change: yes—he was certainly broader in the

shoulders: he carried himself with more than professional dignity: his

wig had risen two inches in the foretop and had descended four

inches behind his back: his coat was not the plain cloth which he

wore habitually in the town and at the tavern, but the black velvet

which was reserved for those occasions when he was summoned by

a person of quality or one of the county gentry, and he carried the

gold-headed cane with the pomander box which also belonged to

those rare occasions.

"Gentlemen," he said, looking around the room slowly and with

emphasis, so that, taking his change of manner and of stature—for

men so seldom grow after fifty—and the emphasis with which he

spoke and looked, gathering together all eyes, caused the company

to understand, without any possibility of mistake, that something

had happened of great importance. In the old town of Lynn Regis it

is not often that anything happens. Ships, it is true, come and go;

their departures and their arrivals form the staple of the

conversation: but an event, apart from the ships, a surprise, is rare.

Once, ten years before this evening, a rumour of the kind which, as

the journals say, awaits confirmation, reached the town, that the

French had landed in force and were marching upon London. The

town showed its loyalty by a resolution to die in the last ditch: the

resolution was passed by the mayor over a bowl of punch; and

though the report proved without foundation the event remained

historical: the loyalty and devotion of the borough—the king's own

borough—had passed through the fire of peril. The thing was

30.

remembered. Since thatevent, nothing had happened worthy of

note. And now something more was about to happen: the doctor's

face was full of importance: he clearly brought great news.

Great news, indeed; and news forerunning a time unheard of in the

chronicles of the town.

"Gentlemen," the doctor laid his hat upon the table and his cane

beside it. Then he took his chair, adjusted his wig, put on his

spectacles, and then, laying his hand upon the arms of the chair he

once more looked round the room, and all this in the most

important, dignified, provoking, interesting manner possible.

"Gentlemen, I have news for you."

As a rule this was a grave and a serious company: there was no

singing: there was no laughing: there was no merriment. They were

the seniors of the town: responsible persons; in authority and office:

substantial, as regards their wealth: full of dignity and of

responsibility. I have observed that the possession of wealth, much

more than years, is apt to invest a man with serious views. There

was little discourse because the opinions of every one were perfectly

well-known: the wind: the weather: the crops: the ships: the health

or the ailments of the company, formed the chief subjects of

conversation. The placid evenings quietly and imperceptibly rolled

away with some sense of festivity—in a tavern every man naturally

assumes some show of cheerfulness and at nine o'clock the

assembly dispersed.

Captain Crowle made answer, speaking in the name of the society,

"Sir, we await your pleasure."

"My news, gentlemen, is of a startling character. I will epitomise or

abbreviate it. In a word, therefore, we are all about to become rich."

Everybody sat upright. Rich? all to become rich? My father, who was

the master of the Grammar school, and the curate of St. Nicholas,

31.

shook their headslike Thomas the Doubter.

"All you who have houses or property in this town: all who are

concerned in the trade of the town: all who direct the industries of

the people—or take care of the health of the residents—will become,

I say, rich." My father and the curate who were not included within

these limits, again shook their heads expressively but kept silence.

Nobody, of course, expects the master of the Grammar school, or a

curate, to become rich.

"We await your pleasure, sir," the captain repeated.

"Rich! you said that we were all to become rich," murmured the

mayor, who was supposed to be in doubtful circumstances. "If that

were true——"

"I proceed to my narrative." The doctor pulled out a pocketbook

from which he extracted a letter. "I have received," he went on, "a

letter from a townsman—the young man named Samuel Semple—

Samuel Semple," he repeated with emphasis, because a look of

disappointment fell upon every face.

"Sam Semple," growled the captain; "once I broke my stick across

his back." He did not, however, explain why he had done so. "I wish

I had broken two. What has Sam Semple to do with the prosperity of

the town?"

"You shall hear," said the doctor.

"He would bring a book of profane verse to church instead of the

Common Prayer," said the vicar.

"An idle rogue," said the mayor; "I sent him packing out of my

countinghouse."

"A fellow afraid of the sea," said another. "He might have become a

supercargo by this time."

32.

"Yet not withoutsome tincture of Greek," said the schoolmaster; "to

do him justice, he loved books."

"He made us subscribe a guinea each for his poems," said the vicar.

"Trash, gentlemen, trash! My copy is uncut."

"Yet," observed the curate of St. Nicholas, "in some sort perhaps, a

child of Parnassus. One of those, so to speak, born out of wedlock,

and, I fear me, of uncertain parentage among the Muses and

unacknowledged by any. There are many such as Sam Semple on

that inhospitable hill. Is the young man starving, doctor? Doth he

solicit more subscriptions for another volume? It is the way of the

distressed poet."

The doctor looked from one to the other with patience and even

resignation. They would be sorry immediately that they had offered

so many interruptions. When it seemed as if every one had said

what he wished to say, the doctor held up his hand and so

commanded silence.

33.

CHAPTER IV

THE GRANDDISCOVERY

"Mr. Sam Semple," the doctor continued, with emphasis on the prefix

to which, indeed, the poet was not entitled in his native town, "doth

not ask for help: he is not starving: he is prosperous: he has gained

the friendship, or the patronage, of certain persons of quality. This is

the reward of genius. Let us forget that he was the son of a

customhouse servant, and let us admit that he proved unequal to

the duties—for which he was unfitted—of a clerk. He has now risen

—we will welcome one whose name will in the future add lustre to

our town."

The vicar shook his head. "Trash," he murmured, "trash."

"Well, gentlemen, I will proceed to read the letter."

He unfolded it and began with a sonorous hum.

"'Honoured Sir,'" he repeated the words. "'Honoured Sir,'—the letter,

gentlemen, is addressed to myself—ahem! to myself. 'I have recently

heard of a discovery which will probably affect in a manner so vital,

the interests of my beloved native town, that I feel it my duty to

communicate the fact to you without delay. I do so to you rather

than to my esteemed patron, the worshipful the mayor, once my

master, or to Captain Crowle, or to any of those who subscribed for

my volume of Miscellany Poems, because the matter especially and

peculiarly concerns yourself as a physician, and as the fortunate

owner of the spring or well which is the subject of the discovery'—

the subject of the discovery, gentlemen. My well—mine." He went

on. "'You are aware, as a master in the science of medicine, that the

curative properties of various spas or springs in the country—the

names of Bath, Tunbridge Wells, and Epsom are familiar to you, so

34.

doubtless are thoseof Hampstead and St. Chad's, nearer London. It

now appears that a certain learned physician having reason to

believe that similar waters exist, as yet unsuspected, at King's Lynn,

has procured a jar of the water from your own well—that in your

garden'—my well, gentlemen, in my own garden!—'and, having

subjected it to a rigorous examination, has discovered that it

contains, to a much higher degree than any other well hitherto

known to exist in this country, qualities, or ingredients, held in

solution, which make this water sovereign for the cure of

rheumatism, asthma, gout, and all disorders due to ill humours or

vapours—concerning which I am not competent so much as to speak

to one of your learning and skill.'"

"He has," said the schoolmaster, "the pen of a ready writer. He

balances his periods. I taught him. So far, he was an apt pupil."

The doctor resumed.

"'This discovery hath already been announced in the public journals.

I send you an extract containing the news.' I read this extract,

gentlemen."

It was a slip of printed paper, cut from one of the diurnals of

London.

"'It has been discovered that at King's Lynn in the county of Norfolk,

there exists a deep well of clear water whose properties, hitherto

undiscovered, form a sovereign specific for rheumatism and many

similar disorders. Our physicians have already begun to recommend

the place as a spa and it is understood that some have already

resolved upon betaking themselves to this newly discovered cure.

The distance from London is no greater than that of Bath. The

roads, it is true, are not so good, but at Cambridge, it is possible for

those who do not travel in their own carriages to proceed by way of

barge or tilt boat down the Cam and the Ouse, a distance of only

forty miles which in the summer should prove a pleasant journey.'

35.

"So far"—the doctorinformed us, "for the printed intelligence. I now

proceed to finish the letter. 'Among others, my patron, the Right

Honourable the Earl of Fylingdale, has been recommended by his

physician to try the newly discovered waters of Lynn as a preventive

of gout. He is a gentleman of the highest rank, fashion, and wealth,

who honours me with his confidence. It is possible that he may even

allow me to accompany him on his journey. Should he do so I shall

look forward to the honour of paying my respects to my former

patrons. He tells me that other persons of distinction are also going

to the same place, with the same objects, during the coming

summer.'

"You hear, gentlemen," said the doctor, looking round, "what did I

say? Wealth for all—for all. So. Let me continue. 'Sir, I would with

the greatest submission venture to point out the importance of this

event to the town. The nobility and gentry of the neighbourhood

should be immediately made acquainted with this great discovery;

the clergy of Ely, Norwich, and Lincoln; the members of the

University of Cambridge: the gentlemen of Boston, Spalding, and

Wisbech should all be informed. It may be expected that there will

be such a concourse flocking to Lynn as will bring an accession of

wealth as well as fame to the borough of which I am a humble

native. I would also submit that the visitors should find Lynn

provided with the amusements necessary for a spa. I mean music;

the assembly; a pump room; a garden; the ball and the masquerade

and the card room; clean lodgings; good wine; and fish, flesh and

fowl in abundance. I humbly ask forgiveness for these suggestions

and I have the honour to remain, honoured sir, your most obedient

humble servant, with my grateful service to all the gentlemen who

subscribed to my verses, and thereby provided me with a ladder up

which to rise, Samuel Semple.'"

At this moment the bowl of punch was brought in and placed before

the captain with a tray of glasses. The doctor folded his letter,

replaced it in his pocketbook and took off his spectacles.

36.

"Gentlemen, you haveheard my news. Captain Crowle, may I

request that you permit the society to drink with me to the

prosperity of the spa—the prosperity of the spa—the spa of Lynn."

"Let us drink it," said the captain, "to the newly discovered spa. But

this Samuel—the name sticks."

The toast was received with the greatest satisfaction, and then,

when the punch was buzzed about, there arose a conversation so

lively and so loud that heads looked out of windows in the square

wondering what in the world had happened with the society. Not a

quarrel, surely. Nay, there was no uplifting of voices: there was no

anger in the voices: nor was it the sound of mirth: there was no

note of merriment: nor was it a drunken loosening of the tongue:

such a thing with this company was impossible. It was simply a

conversation in which all spoke at the same time over an event

which interested and excited all alike. Everybody contributed

something.

"We must have a committee to prepare for the accommodation of

the visitors."

"We must put up a pump room."

"We must engage a dipper."

"We must make walks across the fields."

"There must be an assembly with music and dancing."

"There must be a card room."

"There must be a long room for those who wish to walk about and

to converse—with an orchestra."

"There must be public breakfasts and suppers."

"We shall want horns to play in the evening."

37.

"We must haveglass lamps of variegated colours to hang among the

trees."

"I will put up the pump room," said the doctor, "in my garden, over

the well."

"We must look to our lodgings. The beds in our inns are for the most

part rough hewn boards on trestles with a flock bed full of knobs

and sheets that look like leather. The company will look for

bedsteads and feather beds."

"The ladies will ask for curtains. We must give them what they are

accustomed to enjoy."

"We must learn the fashionable dance."

"We must talk like beaux and dress like the gentlefolk of

Westminster."

The captain looked on, meanwhile, whispering in my ear, from time

to time. "Samuel is a liar," he said. "I know him to be a liar. Yet why

should he lie about a thing of so much importance? If he tells the

truth, Jack—I know not—I misdoubt the fellow—yet—again—he may

tell the truth——And why should he lie, I say? Then—one knows not

—among the company we may even find a husband for the girl. As

for taking her to London—but we shall see."

So he shook his head, not wholly carried away like the rest, but with

a certain amount of hope. And then, waiting for a moment when the

talk flagged a bit, he spoke.

"Gentlemen, if this news is true—and surely Samuel would not

invent it, then the old town is to have another great slice of luck. We

have our shipping and our trade: these have made many of us rich

and have given an honest livelihood to many more. The spa should

bring in, as the doctor has told us, wealth by another channel. I

undertake to assure you that we shall rise to the occasion. The town

38.

shall show itselffit to receive and to entertain the highest company.

We tarpaulins are too old to learn the manners of fashion. But we

have men of substance among us who will lay out money with such

an object: we have gentlemen of family in the country round: we

have young fellows of spirit," he clapped me on the shoulder, "who

will keep up the gaieties: and, gentlemen, we have maidens among

us—as blooming as any in the great world. We shall not be ashamed

of ourselves—or of our girls."

These words created a profound sigh of satisfaction. The men of

substance would rise to the occasion.

Before the bowl was out a committee was appointed, consisting of

Captain Crowle, the vicar of St. Margaret's, the curate of St. Nicholas

—the two clergymen being appointed as having imbibed at the

University of Cambridge some tincture of the fashionable world—and

the doctor. This important body was empowered to make

arrangements for the reception and for the accommodation and

entertainment of the illustrious company expected and promised. It

was also empowered to circulate in the country round about news of

the extraordinary discovery and to invite all the rheumatic and the

gouty: the asthmatic and everybody afflicted with any kind of

disease to repair immediately to Lynn Regis, there to drink the

sovereign waters of the spa.

"It only remains, gentlemen," said the doctor in conclusion, "that I

myself should submit the water of my well to an examination." He

did not think it necessary to inform the company that he had

received from Samuel Semple an analysis of the water stating the

ingredients and their proportions as made by the anonymous

physician of London. "Should it prove—of which I have little doubt—

that the water is such as has been described by my learned brother

in medicine, I shall inform you of the fact."

It was a curious coincidence, though the committee of reception

were not informed of the fact, that the doctor's analysis exactly

39.

agreed with thatsent to him.

It was a memorable evening. For my own part,—I know not why—

during the reading of the letter my heart sank lower and lower. It

was the foreboding of evil. Perhaps it was caused by my knowledge

of Samuel of whom I will speak presently. Perhaps it was the

thought of seeing the girl whom I loved, while yet I had no hope of

winning her, carried off by some sprig of quality who would teach

her to despise her homely friends, the master mariners young and

old. I know not the reason. But it was a foreboding of evil and it was

with a heavy heart that I repaired to the quay and rowed myself

back to the ship in the moonlight.

They were going to drink to the next voyage of The Lady of Lynn.

Why, the lady herself, not her ship, was about to embark on a

voyage more perilous—more disastrous—than that which awaited

any of her ships. Cruel as is the ocean I would rather trust myself—

and her—to the mercies of the Bay of Biscay at its wildest—than to

the tenderness of the crew who were to take charge of that innocent

and ignorant lady.

40.

CHAPTER V

THE PORTOF LYNN

This was the beginning of the famous year. I say famous because, to

me and to certain others, it was certainly a year eventful, while to

the people of the town and the county round it was the year of the

spa which began, ran a brief course, and terminated, all in one

summer.

Let me therefore speak for a little about the place where these

things happened. It is not a mushroom or upstart town of yesterday

but on the other hand a town of venerable antiquity with many

traditions which may be read in books by the curious. It is important