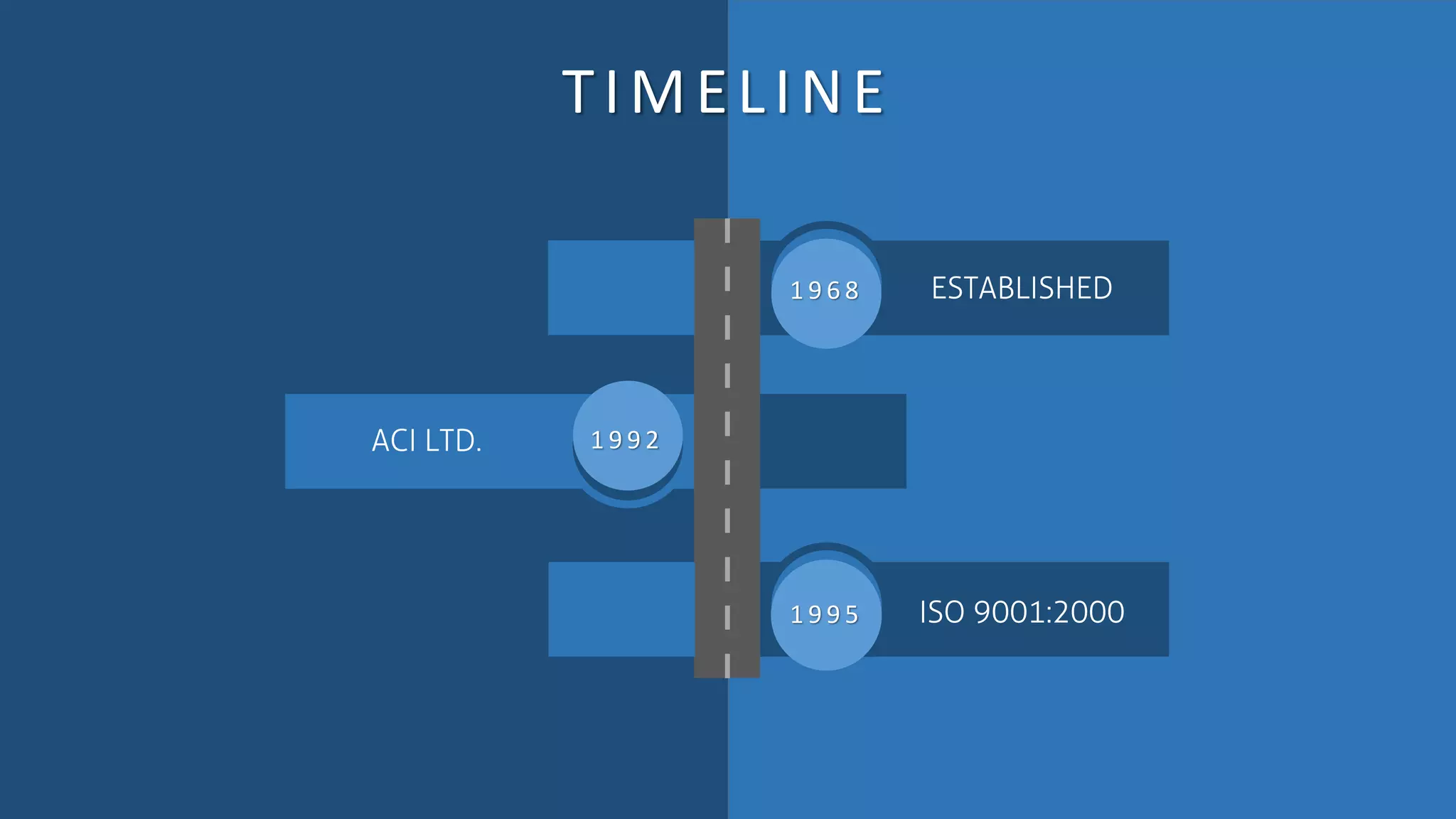

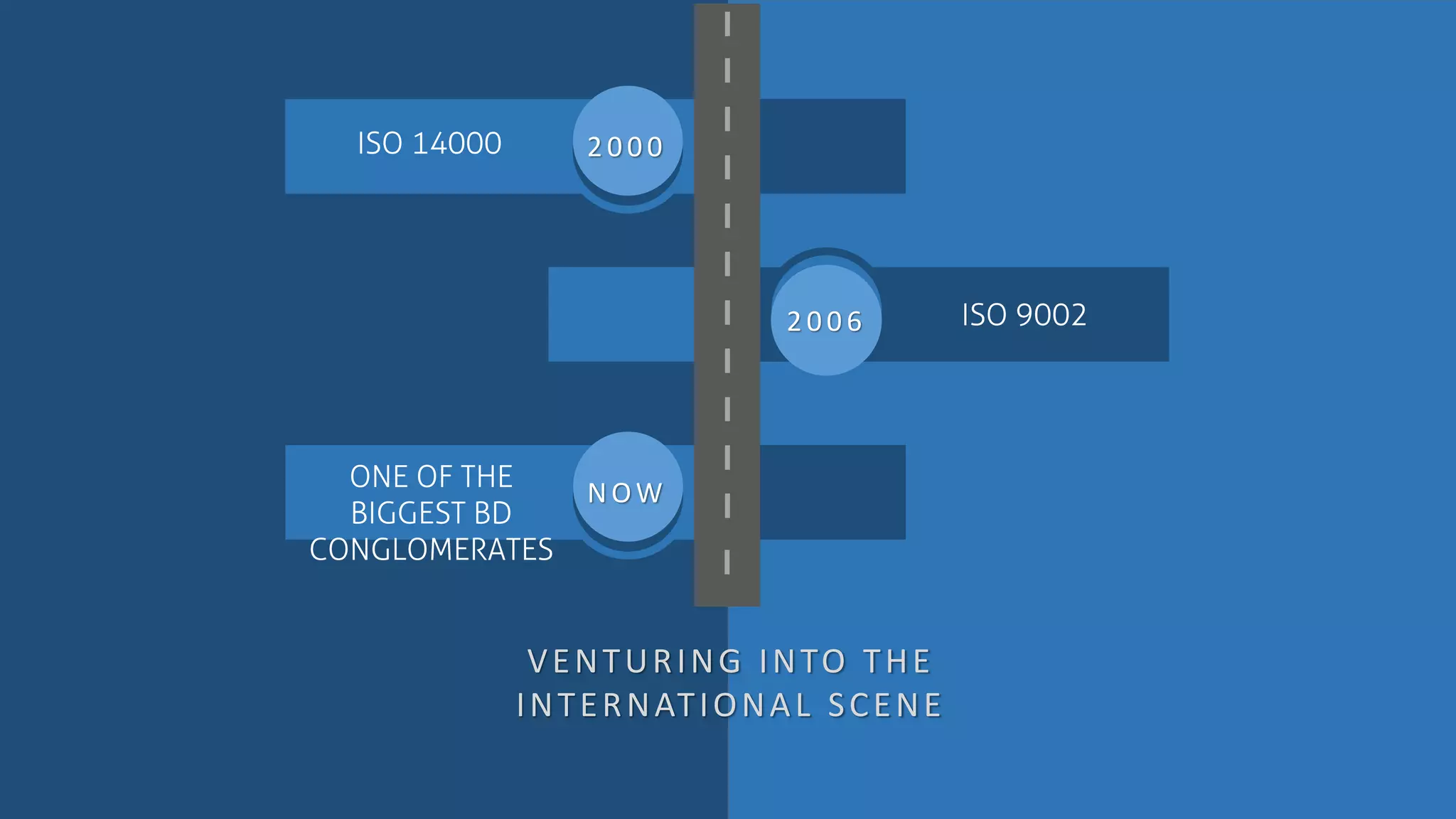

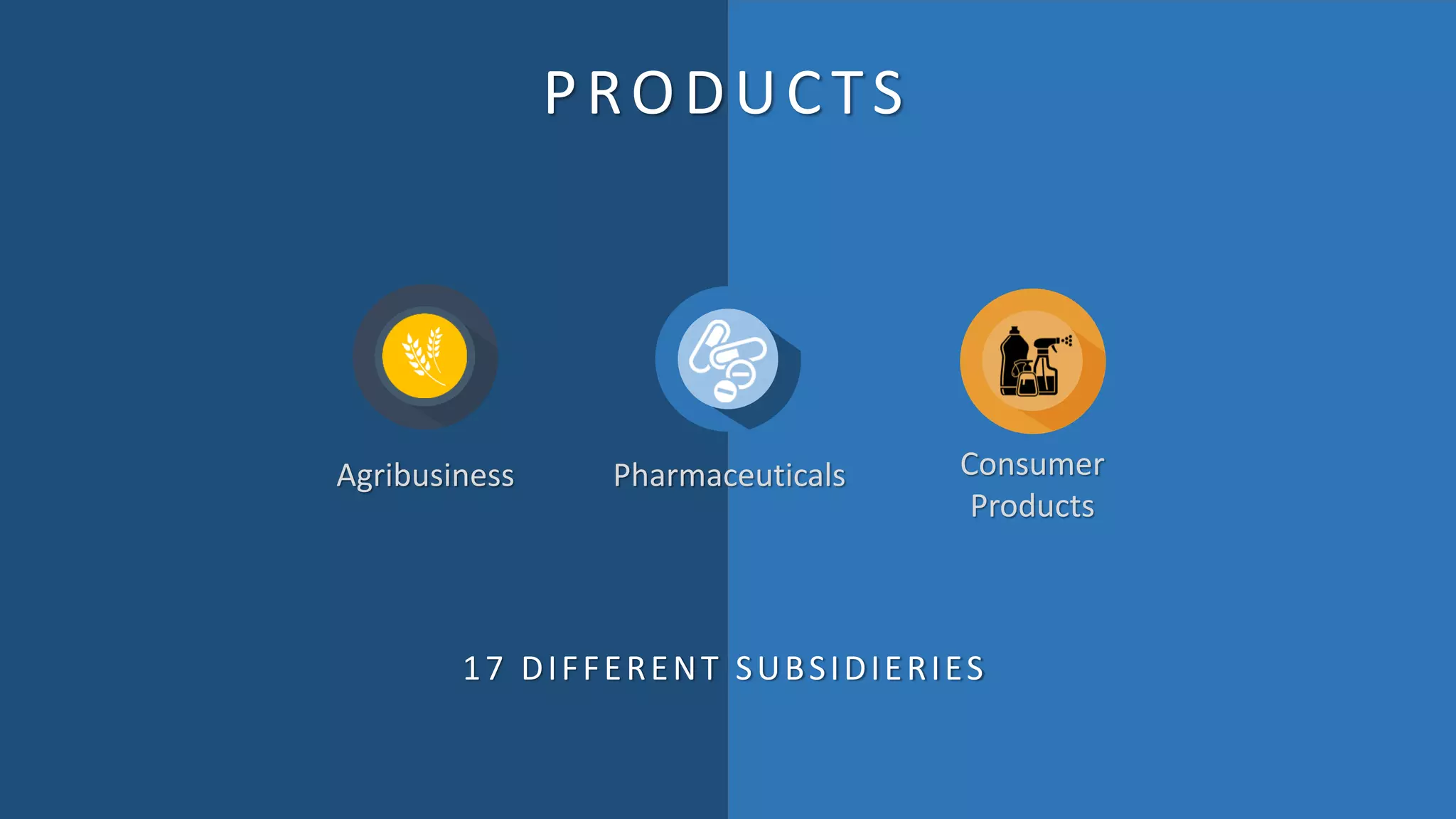

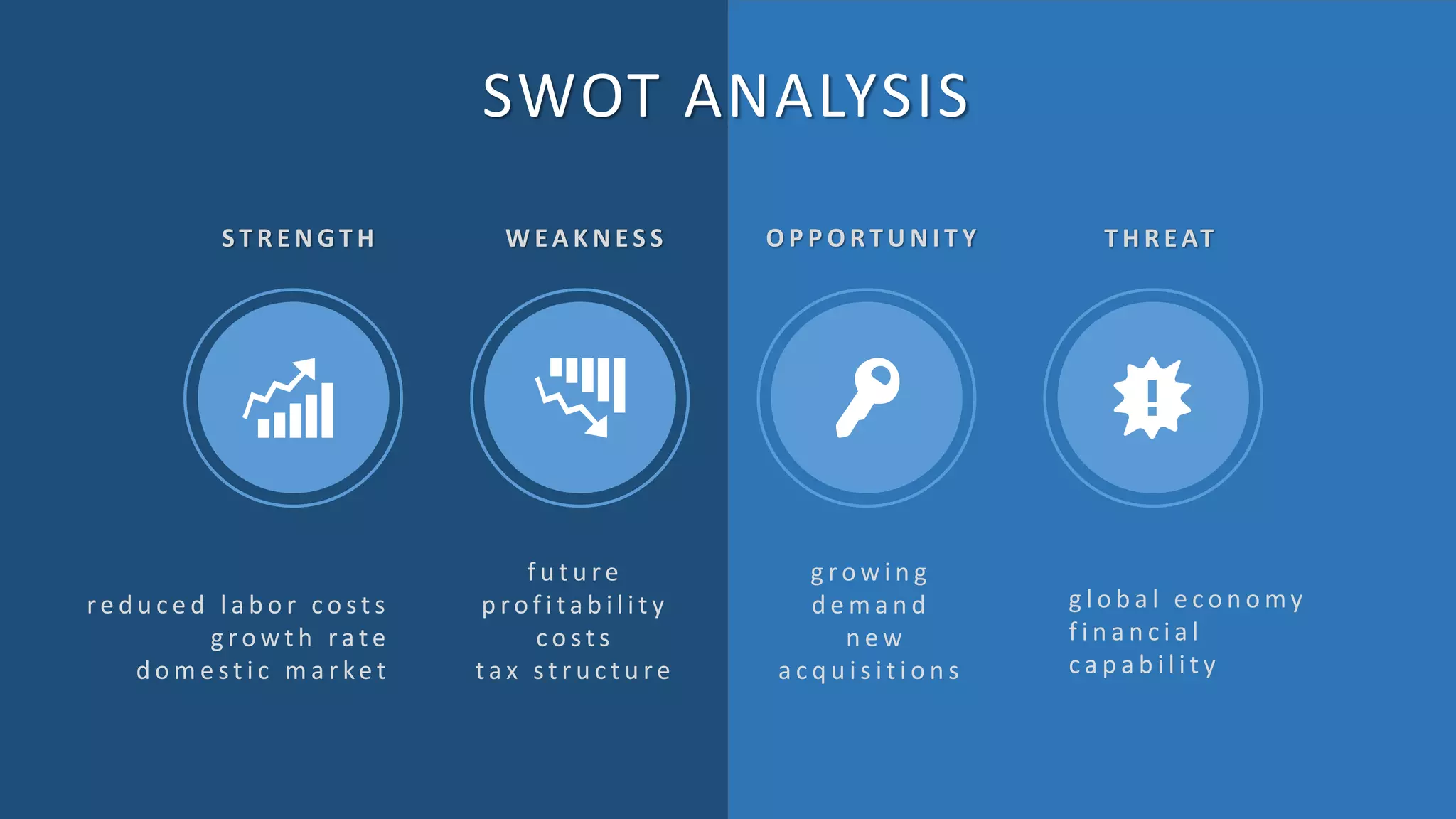

The document discusses the accounting practices of ACI Limited, a large Bangladeshi conglomerate. It outlines the company's history, objectives to analyze its accounting style, and lists group members. It also covers ACI's products, competitors, mission, vision and values. The document analyzes ACI's accounting standards, transactions recording, accounting system, error resolution, basis of accounting, accounts entries, inventory, costs, controls, fraud prevention, depreciation, and dividend policy.