Download to read offline

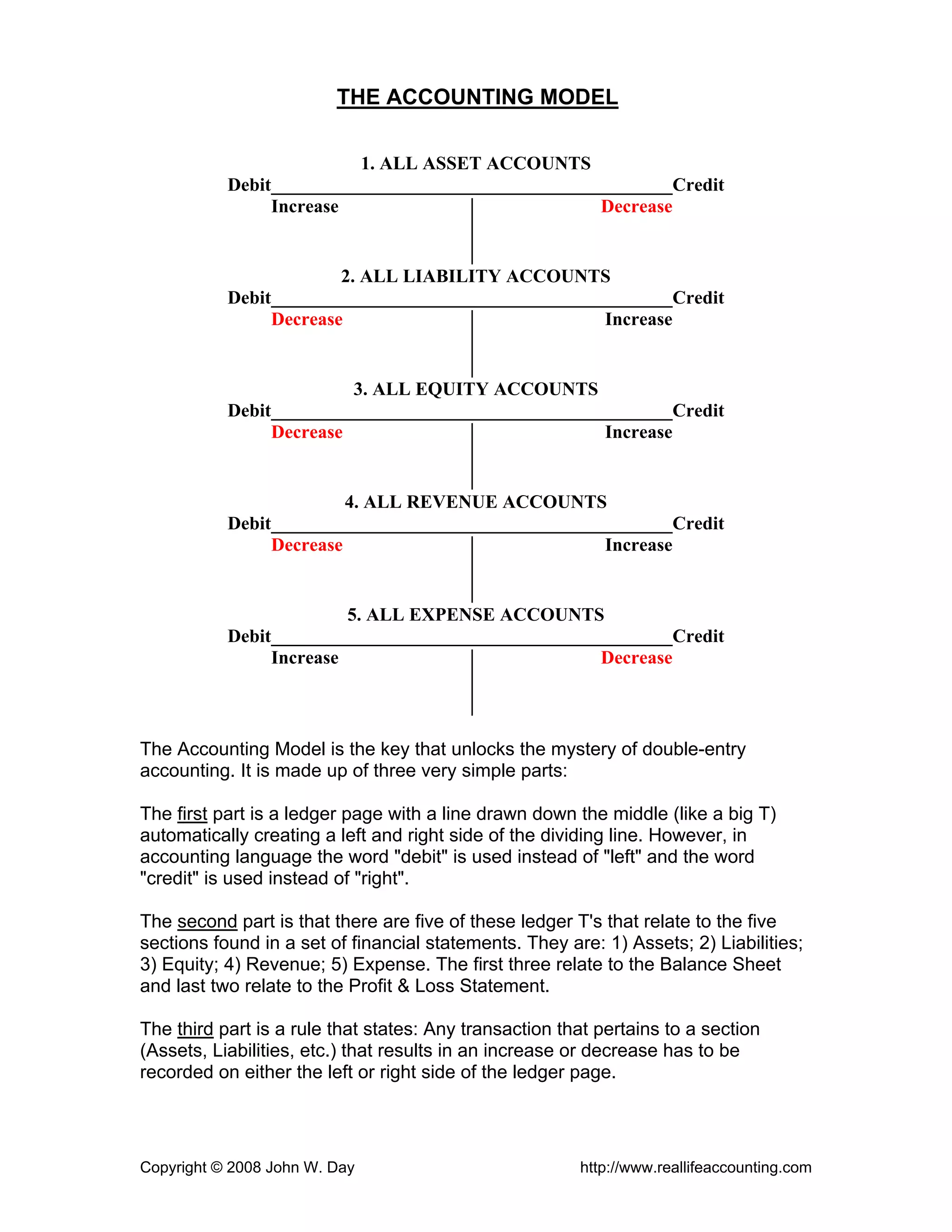

The accounting model outlines the basic rules for debit and credit entries for the five main accounts: 1) Assets are debited to increase and credited to decrease. 2) Liabilities are credited to increase and debited to decrease. 3) Equity is debited to decrease and credited to increase. 4) Revenue is credited to increase and debited to decrease. 5) Expenses are debited to increase and credited to decrease. It uses a T-account format with debit on the left and credit on the right to record transactions that increase or decrease the different accounts.