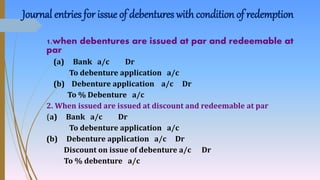

This document discusses accounting for debentures. It defines debentures as a written acknowledgment of debt issued by a company under its seal. The document then outlines six journal entries for issuing debentures under different terms, such as being issued at par/premium/discount and redeemed at par/premium. It also provides brief explanations of debentures, reasons for investing in them, how they can be categorized, the nature of premium on redemption accounts, and differences between debentures and shares.