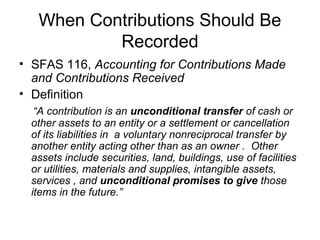

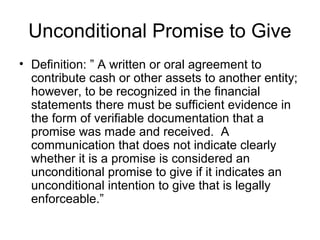

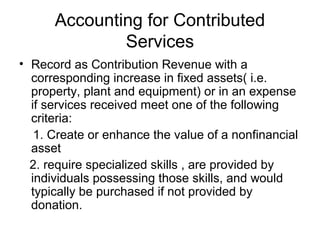

This document summarizes accounting standards for different types of contributions. It discusses when contributions should be recorded, the impact of donor restrictions, accounting for contributed services and non-cash contributions, and pass-through contributions. The key points are that contributions must be unconditional transfers, donor restrictions can be temporary or permanent, contributed services may be recorded if they create value or require specialized skills, non-cash contributions are recorded at fair market value, and pass-through contributions depend on the level of control the recipient organization has.