Report Date, 200xPage 2

Objectives, Scope & Procedures Performed 2

Executive Summary 3

Detailed Issues & Observations 5

Appendices

Appendix A: General Background 20

Appendix B: Internal Control Scorecard 22

Appendix C: Best Practices Scorecard 23

Appendix D: Best Practices Details 24

Appendix E: Testing Summary 29

Appendix F: Performance Measures 32

Appendix G: Process Flowcharts 33

Table of Contents

This report provides management with information about the condition of risks and internal controls at a specific point in time. Future changes

in environmental factors and actions by personnel will impact these risks and internal controls in ways that this report cannot anticipate.

3.

Report Date, 200xPage 3

The scope of this audit includes a review of Accounts Payable

processes, focusing on the following areas:

• Invoice receipt.

• Invoice approval process.

• Matching of invoice to purchase order and to receiving

information.

• Prioritization of payments.

• Use of early payment discounts.

• Payment processing.

• Record retention.

• Reconciliations between general ledger, AP sub-ledger,

and bank accounts.

• Determine if key financial and business controls exist and are

operating effectively.

• Assess the operating efficiency of the process.

• Compare Company’s practices to “Best Practices,” including

performance measures.

• Review performance measures used to monitor and improve

the process.

• Assess compliance with applicable corporate policies and

procedures.

• Identify opportunities for internal control and process

improvements.

• Interviewed key management and personnel regarding the accounts payable processes.

• Reviewed existing documentation of relevant policies and procedures.

• Obtained an understanding of procedures and internal controls.

• Discussed existing management plans to improve operations or internal controls.

• Performed analysis on accounts payable transactions for the period (Month) 200X through (Month) 200X.

• Documented the accounts payable process through high-level process maps.

• Evaluated the effectiveness and efficiency of business processes against “Best Practices.”

• Summarized observations and management action plans.

Objectives, Scope & Procedures Performed

Summary of Procedures Performed

Objectives Scope

4.

Report Date, 200xPage 4

Executive Summary

Internal audit reviewed the Accounts Payable function in (Month) of 200X. The objectives of this review were to obtain an understanding of

the key administrative, operational and financial processes relating to these functions, evaluate the adequacy and effectiveness of the

associated internal controls and to identify opportunities for process improvements.

Overall, the control environment was in need of improvement. At the time of our review, Management had identified weaknesses in

controls and had begun to implement plans to improve the control environment as well as the efficiency and business effectiveness of the

process. These plans are summarized on page 6. We noted some additional areas where controls could be enhanced or added - these

are summarized below.

See the Detailed Issues & Observations section of this report (pages 7 - 20) for a detailed discussion of all issues identified in this review

and the management implementation plan to address each issue.

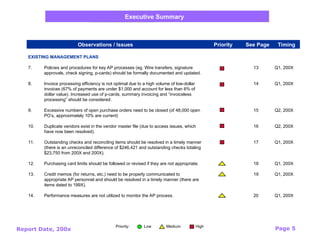

Observations / Issues Priority See Page Timing

Q1, 200X

Q2, 200X

Q1, 200X

Q2, 200X

Q4, 200X

Q4, 200X

Low Medium High

Priority:

1. Purchase requisition approval process is not consistently followed (9 of 25

approvals examined were completed by personnel not authorized in the “Approval

List”).

2. Review of purchasing card transactions should be strengthened (we noted

numerous exceptions in our testing).

3. Invoices should be recorded and processed on a timely basis (we noted numerous

exceptions in our testing).

4. Not all receipts to support reimbursement of T&E expenses were submitted as

required by corporate policy (3 reports out of 20 tested did not contain all

documentation).

5. Password security for check printing applications does not conform to the

Computer Security, Audit and Control Policy.

6. Unit A’s petty cash ($3,000) balance is larger than necessary (management

subsequently decided to eliminate the fund).

7

8

9

10

11

12

5.

Report Date, 200xPage 5

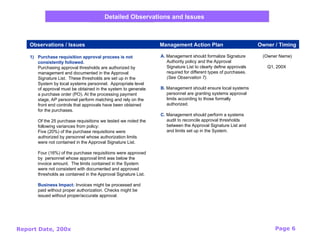

Low Medium High

Priority:

Executive Summary

EXISTING MANAGEMENT PLANS

7. Policies and procedures for key AP processes (eg. Wire transfers, signature

approvals, check signing, p-cards) should be formally documented and updated.

8. Invoice processing efficiency is not optimal due to a high volume of low-dollar

invoices (67% of payments are under $1,000 and account for less than 6% of

dollar value). Increased use of p-cards, summary invoicing and “invoiceless

processing” should be considered.

9. Excessive numbers of open purchase orders need to be closed (of 48,000 open

PO’s, approximately 10% are current)

10. Duplicate vendors exist in the vendor master file (due to access issues, which

have now been resolved).

11. Outstanding checks and reconciling items should be resolved in a timely manner

(there is an unreconciled difference of $246,421 and outstanding checks totaling

$23,750 from 200X and 200X).

12. Purchasing card limits should be followed or revised if they are not appropriate.

13. Credit memos (for returns, etc.) need to be properly communicated to

appropriate AP personnel and should be resolved in a timely manner (there are

items dated to 199X).

14. Performance measures are not utilized to monitor the AP process.

Observations / Issues Priority See Page Timing

Q1, 200X

Q1, 200X

Q2, 200X

Q2, 200X

Q1, 200X

Q1, 200X

Q1, 200X

Q1, 200X

13

14

15

16

17

18

19

20

6.

Report Date, 200xPage 6

1) Purchase requisition approval process is not

consistently followed.

Purchasing approval thresholds are authorized by

management and documented in the Approval

Signature List. These thresholds are set up in the

System by local systems personnel. Appropriate level

of approval must be obtained in the system to generate

a purchase order (PO). At the processing payment

stage, AP personnel perform matching and rely on the

front end controls that approvals have been obtained

for the purchases.

Of the 25 purchase requisitions we tested we noted the

following variances from policy:

Five (20%) of the purchase requisitions were

authorized by personnel whose authorization limits

were not contained in the Approval Signature List.

Four (16%) of the purchase requisitions were approved

by personnel whose approval limit was below the

invoice amount. The limits contained in the System

were not consistent with documented and approved

thresholds as contained in the Approval Signature List.

Business Impact: Invoices might be processed and

paid without proper authorization. Checks might be

issued without proper/accurate approval.

(Owner Name)

Q1, 200X

A. Management should formalize Signature

Authority policy and the Approval

Signature List to clearly define approvals

required for different types of purchases.

(See Observation 7).

B. Management should ensure local systems

personnel are granting systems approval

limits according to those formally

authorized.

C. Management should perform a systems

audit to reconcile approval thresholds

between the Approval Signature List and

and limits set up in the System.

Observations / Issues Management Action Plan Owner / Timing

Detailed Observations and Issues

7.

Report Date, 200xPage 7

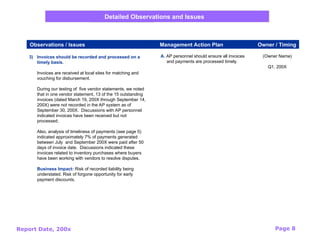

2) Review of purchasing card transactions should be

strengthened.

Approximately 220 company employees use purchasing

cards (p-card) for the acquisition of lower cost goods and

services. The process to review p-card expenditures

currently resides with local office managers .

The Purchasing Manager of US Contracts and Agreements

sends p-card transaction reports to local managers for

review monthly. Managers are not required to sign and

return reports evidencing review and approval. Negative

confirmation serves as approval.

Although cardholders are responsible for sending

reconciled monthly p-card activity logs to supervisors for

review and signature, our testing of 10 logs indicated the

following:

• Two activity logs were not submitted for approval.

• One supervisor approval was verbal and not

documented.

• One approval was typed in by employee without actual

approval from supervisor.

• Three had missing receipts.

• One had a transaction over the $1,500 per transaction

limit.

Also see Observation 12 regarding non-compliance with p-

card procedures and disbursement policy.

Business Impact: Increased risk of inaccurate and

unauthorized processing of P-card expenditures.

(Owner Name)

Q2, 200X

A. Management should require managers to

sign and return p-card transaction reports

evidencing review and approval.

B. Management should review all

transactions and receipts and then sign

activity logs to document review for

accuracy, completeness and

appropriateness of expenditures.

Observations / Issues Management Action Plan Owner / Timing

Detailed Observations and Issues

8.

Report Date, 200xPage 8

3) Invoices should be recorded and processed on a

timely basis.

Invoices are received at local sites for matching and

vouching for disbursement.

During our testing of five vendor statements, we noted

that in one vendor statement, 13 of the 15 outstanding

invoices (dated March 19, 200X through September 14,

200X) were not recorded in the AP system as of

September 30, 200X. Discussions with AP personnel

indicated invoices have been received but not

processed.

Also, analysis of timeliness of payments (see page 5)

indicated approximately 7% of payments generated

between July and September 200X were paid after 50

days of invoice date. Discussions indicated these

invoices related to inventory purchases where buyers

have been working with vendors to resolve disputes.

Business Impact: Risk of recorded liability being

understated. Risk of forgone opportunity for early

payment discounts.

(Owner Name)

Q1, 200X

A. AP personnel should ensure all invoices

and payments are processed timely.

Observations / Issues Management Action Plan Owner / Timing

Detailed Observations and Issues

9.

Report Date, 200xPage 9

4) Not all of the receipts to support T&E reimbursement

of expenses were submitted as required by

corporate policy.

Travel and Entertainment (T&E) Expenses

Travel Policy (Finance Policy XX) states the company’s

requirements for the submission of supporting

documentation and receipts. It also requires employees

to file T&E expense reports no later than 30 days after

completion of each trip.

In our testing of 20 expense reports, we noted three

expense reports that did not contain all required receipts.

Petty Cash Expenses

As of September 200X, only 5 plants have petty cash.

Personnel at sites with no petty cash are requesting

reimbursements via expense reports. The current

practice for expense reports is to review for receipts if

report total (excluding airfare and mileage) exceeds $40.

Management should revise the current policy and

procedures to ensure receipts are submitted, proper

approvals are obtained, and adequate review is

performed for petty cash items submitted via expense

reports.

Business Impact: Unauthorized expense

reimbursements. Potential for reimbursement of non-

business expenses. Potential tax-related issues due to

lack of documentation.

(Owner Name)

Q2, 200X

A. The Expense Report Processor should

review expense reports for all required

receipts.

B. Management should determine

appropriate procedures for reviewing petty

cash items submitted via expense reports.

New procedures should be documented

in the formal policy.

Observations / Issues Management Action Plan Owner / Timing

Detailed Observations and Issues

10.

Report Date, 200xPage 10

5) Password security for check printing applications

does not conform to the Computer Security, Audit

and Control Policy.

The current Computer Security, Audit and Control

Policy requires unique user IDs and passwords.

Passwords are to be a minimum of six characters and

must be a combination of alpha and numeric

characters. Passwords are to be changed at least

every 60 days.

The AP department uses (3rd

Party Software) for

printing AP checks. Two users of the AP group share a

user ID and password. The password is not required to

be changed on a regular basis.

The Expense Report Processor uses (3rd

Party

Software) for printing expense checks. The password is

not required to be changed on a regular basis.

Business Impact: Lack of individual accountability.

Risk for unauthorized access to (3rd

Party Software).

Potential financial losses due to AP check frauds.

(Owner Name)

Q4, 200X

A. Administrators for the applications should

determine if the software has the

capability of required password changes.

B. Management should ensure compliance

with corporate policy or otherwise

document and obtain approval for

exceptions.

Observations / Issues Management Action Plan Owner / Timing

Detailed Observations and Issues

11.

Report Date, 200xPage 11

6) Unit A’s petty cash balance appears to be larger

than necessary.

As of September 200X, only five units have petty cash.

All locations have between $500 and $1,000 in their

petty cash fund with the exception Unit A. Discussions

with the Accounting Assistant indicated Unit A has

$3,000 in petty cash. This amount appears to be

excessive when compared to other locations.

Additionally, the Accounting Assistant indicated that

$500 to $1,000 would be sufficient for monthly petty

cash needs.

Business Impact: Increased exposure of cash theft.

(Owner Name)

Q4, 200X

A. After management’s assessment of the

need for a petty cash fund in Unit A, a

decision was made to eliminate the petty

cash fund by (Month, 200X)

Observations / Issues Management Action Plan Owner / Timing

Detailed Observations and Issues

12.

Report Date, 200xPage 12

Existing Management Plans

Observations / Issues Existing Management Plan Owner / Timing

7) Policies and procedures for key AP processes

should be formally documented and updated.

There is no formal AP policy. Certain policies and

procedures used by the AP department exist but are

not formally documented. These include the following:

• Draft policy – Disbursement (Wires).

• – Disbursement (Checks and Other).

• – Signature Authority.

• Informal procedures – Purchasing Cards.

• Informal policy – Approval Signature List.

The Corporate Travel policy contains outdated

information (e.g. mileage reimbursement amount).

Also, it does not specify the dollar threshold ($75 per

IRS) for submitting receipts other than meal expenses.

In our testing, we noted five (20%) purchase

requisitions were not properly authorized. These were

signed by local employees whose authorities are not

documented in the Approval Signature List. (see also

issue number 1)

Business Impact: Lack of clearly defined roles and

responsibilities. Loss of knowledge in the event of

employee illness or turnover. Difficulty in training new

personnel. Difficulty in assessing accountability.

Inconsistent understanding and application of policies

and procedures.

(Owner Name)

Q1, 200X

A. The Financial Systems Manager is aware

of the issue. Senior management is in the

process of drafting and issuing these

policies as part of the “Corporate Policy

Initiative”. Senior management has plans

to complete this initiative by the end of Q2,

200X.

B. Management should communicate the

formal policies to all related personnel.

C. The Financial Systems Manager plans to

update the Corporate Travel policy and

instructions in the standard expense

reporting Excel worksheet.

D. Management should post relevant policies

and procedures on the intranet for

accessibility by all personnel.

E. Management should implement a periodic

review process to ensure policies and

procedures are being consistently

followed by AP personnel.

13.

Report Date, 200xPage 13

Existing Management Plans

Existing Management Observations / Issues Existing Management Plan Owner / Timing

8) Invoice processing efficiency is not optimal due to

a high volume of low-dollar invoices.

In the period of July through September 200X, 67% of

all payments processed were less than $1,000, but

accounted for less than 6% of the total dollar value of

invoices. See appendix “A” for the results of the data

analysis.

Approximately 220 employees use purchasing cards

(p-cards). The use of p-cards is a proven best practice

that has been successfully used to reduce costs and

cycle times for low dollar transactions. Opportunities

exist to increase the efficiency of the procurement

function by expanding the utilization of p-cards and/or

requesting summary invoicing from vendors with whom

a large volume of transactions occur at low dollar

amounts.

Business Impact: Inefficient processing. Increased

processing costs related to issuing, reviewing and

clearing checks.

(Owner Name)

Q1, 200X

A. Management is aware of the issue and

plans to increase the use of p-cards to

decrease volume of low-dollar invoices.

B. Consider benchmarking performance by

quantifying the percentage of items or

dollars expensed to p-cards and

volume/value of invoices processed.

C. Consider increasing the use of summary

invoicing with key vendors on a larger

scale in order to combine numerous

invoices for efficient payment purposes.

D. Consider implementing “invoiceless

processing” with key vendors. Payment

will be based upon receipt of goods and

merchandise at agreed-upon prices rather

than receipt of an invoice. Invoiceless

processing requires extensive employee

training, upfront system edits, accurate

purchase order and receiving processes

and clear exemption reporting. The

benefits could be lower payable

transaction costs, simplified material

controls, fewer AP personnel per 100

million of disbursements and improved

control over AP.

14.

Report Date, 200xPage 14

Existing Management Plans

Existing Management Observations / Issues Existing Management Plan Owner / Timing

9) Excessive numbers of open purchase orders need

to be closed.

Review of open commitments report indicate excessive

purchase orders are currently open. Some of these

date back to 199X.

Discussions with the Financial Systems Manager

indicated he is aware of the issue and there appears to

be 48,000 open POs, of which only approximately 10%

are current.

Business Impact: Risk of potential liability from

purchase order commitments. Complications for

management in deleting duplicate vendors (see

Observation 10).

(Owner Name)

Q2, 200X

A. Financial Systems Manager indicated he

is aware of the issue and that research will

be performed to close the open POs.

15.

Report Date, 200xPage 15

Existing Management Plans

Existing Management Observations / Issues Existing Management Plan Owner / Timing

10) Duplicate vendors exist in the vendor master file.

Prior to April 200X, Local plant personnel had access to

the vendor master file to add, change, and delete

vendors. This open access led to duplicate vendors

being set up.

Discussions with the Financial Systems Manager

indicated management is aware of duplicate vendors in

the system. As of April 200X, access to the vendor

master database had been restricted to four personnel.

All new vendor requests must be approved by the

Financial Systems Manager and added by AP

personnel.

Business Impact: Inefficiency in processing payments.

Difficulty in analyzing vendor-specific AP data.

Potential for inconsistent contract terms with same

vendor.

(Owner Name)

Q2, 200X

A. Upon closing of the non-current open POs

(see Observation 9), the AP department

will go through the vendor master file and

delete duplicate vendors.

16.

Report Date, 200xPage 16

Existing Management Plans

Existing Management Observations / Issues Existing Management Plan Owner / Timing

11) Outstanding checks and reconciling items should

be resolved in a timely manner.

AP accounts, disbursements, and bank accounts are

reconciled by the accountant on a monthly basis.

In the August 200X bank reconciliation, $246,421 (17%

of bank balance) was identified as prior unknown

variances that require further research. Also, there

were outstanding checks of $23,750 (1% of AP bank

balance) from 200X and 200X.

Business Impact: Potential for inaccurate cash

balances. Risk for undetected AP check fraud.

(Owner Name)

Q1, 200X

A. Management is aware of the issue. The

Legal department is performing research

to determine the legality of voiding

outstanding checks that are over six

months old.

B. The Accountant is performing research on

the unreconciled balance.

17.

Report Date, 200xPage 17

Existing Management Plans

Existing Management Observations / Issues Existing Management Plan Owner / Timing

12) Purchasing card limits should be followed or

revised if they are not appropriate.

The draft policy on Disbursements (Checks and Other)

states spending limits on purchasing cards (p-cards)

are $1,500 per transaction and $10,000 per month.

The P-Card procedures also states the $1,500 per

transaction limit.

Per review of the American Express billing summary,

we noted numerous employees have spending limits

over the policy amounts. During our testing of ten

activity logs, we noted one log that had a transaction

over the $1,500 per transaction limit.

Discussions with the Purchasing Manager of US

Contracts and Agreements indicated the limits are

determined by employees’ supervisors based on actual

needs in relation to job positions.

Business Impact: Increased risk of unauthorized

spending.

(Owner Name)

Q1, 200X

A. The Purchasing Manager of US Contracts

and Agreements indicated the p-card

procedure and each employees limits are

scheduled to be reviewed in November.

The procedure will be changed to reflect

"exceptions" and limits will be adjusted

based on actual use.

18.

Report Date, 200xPage 18

Existing Management Plans

Existing Management Observations / Issues Existing Management Plan Owner / Timing

13) A process should be established to communicate

Credit memos to AP personnel.

Discussions indicated that returns are not always

communicated to AP and there is no individual formally

designated the responsibility to follow up with vendors to

ensure returns and credits are properly and timely

processed. Hence, credits may not be applied

appropriately.

For credit memos that have been applied, the Financial

Systems Manager sends a summary of aged credit

balances to local management requesting follow up. As of

September 30, 200X, there is a net debit balance of

$268,510 (4% of total AP balance) for invoices

outstanding and credit balances over 90 days. A number

of these items date to 199X.

It has been communicated and recommended that for

vendors where the credit memo is aged and that the

company has not done business within the past 12

months, a request should be sent to vendor for payment.

It has also been noted that certain credit balances are with

vendors who have gone bankrupt; hence, reserves should

be booked against those amounts.

Business Impact: Risk of inaccurate AP balance. Cash

balance is not maximized.

(Business Owner)

Q1, 200X

A. Continue to work with local management

and vendors to resolve credit balances.

19.

Report Date, 200xPage 19

Existing Management Plans

Existing Management Observations / Issues Existing Management Plan Owner / Timing

14) Performance measures are not utilized to monitor

the AP process.

The AP department has not identified a clear set of

key performance measures to monitor AP activities

and to facilitate process improvements.

Periodically, AP aging reports, check registers, and

account reconciliations are reviewed by management.

The Financial Systems Manager is also developing

tools to analyze the timeliness of invoice processing.

Discussions indicated plans to work with the Treasury

department to estimate outgoing cash flows related to

disbursements to facilitate proper cash management.

See Appendix F for a list of key performance

measures.

Business Impact: Lack of accountability. Difficulty in

identifying root causes of issues. Lack of relevant

information to improve performance. Opportunity cost

for improved cash management.

(Owner Name)

Q1, 200X

A. Management is working with Treasury with

a focus on outgoing cash flow aging.

B. Management should develop performance

measures and standardized reports to

monitor and improve the AP process.

C. Management should communicate

performance measure goals to all

employees and include them as part of the

annual employee goal setting / and review

process.

D. Management should review actual

performance against goals on a regular

basis and make adjustments or changes

to goals as needed.

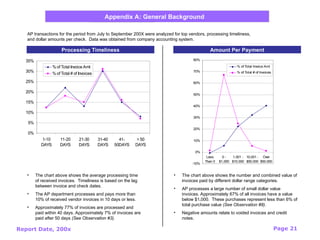

Report Date, 200xPage 21

• The chart above shows the number and combined value of

invoices paid by different dollar range categories.

• AP processes a large number of small dollar value

invoices. Approximately 67% of all invoices have a value

below $1,000. These purchases represent less than 6% of

total purchase value (See Observation #8).

• Negative amounts relate to voided invoices and credit

notes.

Appendix A: General Background

AP transactions for the period from July to September 200X were analyzed for top vendors, processing timeliness,

and dollar amounts per check. Data was obtained from company accounting system.

• The chart above shows the average processing time

of received invoices. Timeliness is based on the lag

between invoice and check dates.

• The AP department processes and pays more than

10% of received vendor invoices in 10 days or less.

• Approximately 77% of invoices are processed and

paid within 40 days. Approximately 7% of invoices are

paid after 50 days (See Observation #3).

0%

5%

10%

15%

20%

25%

30%

35%

1-10

DAYS

11-20

DAYS

21-30

DAYS

31-40

DAYS

41-

50DAYS

> 50

DAYS

% of Total Invoice Amt

% of Total # of Invoices

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Less

Than 0

0 -

$1,000

1,001 -

$10,000

10,001 -

$50,000

Over

$50,000

% of Total Invoice Amt

% of Total # of Invoices

Processing Timeliness Amount Per Payment

22.

Report Date, 200xPage 22

Appendix A: General Background

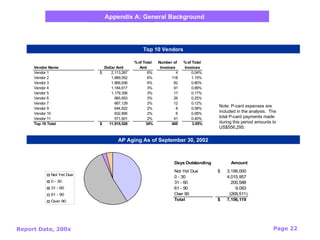

Note: P-card expenses are

included in the analysis. The

total P-card payments made

during this period amounts to

US$556,295.

Days Outstanding Amount

Not Yet Due 3,199,000

$

0 - 30 4,015,957

31 - 60 200,588

61 - 90 9,083

Over 90 (268,511)

Total 7,156,119

$

Not Yet Due

0 - 30

31 - 60

61 - 90

Over 90

Top 10 Vendors

AP Aging As of September 30, 2002

Vendor Name Dollar Amt

%of Total

Amt

Number of

Invoices

%of Total

Invoices

Vendor 1 2,113,267

$ 6% 4 0.04%

Vendor 2 1,989,052 6% 118 1.15%

Vendor 3 1,966,936 6% 82 0.80%

Vendor 4 1,184,617 3% 91 0.89%

Vendor 5 1,179,356 3% 17 0.17%

Vendor 6 965,853 3% 26 0.25%

Vendor 7 667,129 2% 12 0.12%

Vendor 9 644,822 2% 8 0.08%

Vendor 10 632,895 2% 6 0.06%

Vendor 11 571,601 2% 41 0.40%

Top 10 Total 11,915,528

$ 34% 405 3.95%

23.

Report Date, 200xPage 23

Appendix B: Internal Control Scorecard

The following matrix lists process controls present within the Accounts Payable process. An evaluation of the company’s process

is noted in each instance. Controls were evaluated as follows:

1. Policies and procedures are documented and followed.

2. Duties are adequately segregated.

3. AP and cash disbursements are properly matched to underlying documents and authorized.

4. Transactions (liabilities) are recorded on a timely basis.

5. Recorded AP balances are substantiated and evaluated.

6. AP records and cash disbursements are safeguarded and numerically controlled.

7. AP and cash disbursement transactions are reliably processed and reported.

8. General ledger accounts, AP accounts, disbursements and bank accounts are reconciled on

a timely basis, and reconciling differences resolved timely.

9. Costs are reduced as much as possible.

10. Processing time is minimized.

3, 4, 5, 7, 12

NA

1, 2, 4

3, 4, 13

9, 12, 13, 14

5, 6, 10

1, 2, 4, 9, 10

11

6, 8, 9, 10

8, 10

Adequate

Improvement Recommended

Not Adequate

Internal Control Practice Rating Issue Ref.

Where possible improvements can be made, a reference has been made to the Issues and Observations section, where

management’s change implementation plan is described, along with the responsible party and estimated implementation timing.

24.

Report Date, 200xPage 24

Appendix C: Best Practices Scorecard

As part of this review, the company’s practices were benchmarked against the “Best Practices.” An evaluation of the Accounts

Payable process is noted in each instance. Best Practices were evaluated as follows:

1. Strengthen cash flow by explicitly managing payment dates and terms.

2. Manage communication with suppliers to establish mutually agreeable practices.

3. Analyze money, quality and time in the current AP process.

4. Implement rigorous, pervasive policies to protect against disbursement fraud and

overpayments.

5. Establish controls appropriate to the risk and value of corresponding transactions.

6. Reduce the volume of AP transactions.

7. Reduce processing costs and cycle times for smaller, recurring invoices as well as T&E

report processing.

8. Integrate AP with related operations.

9. Process invoices and checks electronically.

10. Use performance measures to achieve overall AP efficiency improvements.

Best Practice Issue Ref.

Rating

Good - “Best Practice” currently in use.

Moderate Use - Improvement possible in order to achieve “Best Practice” status.

Limited/Some Use - Improvement recommended to improve process efficiency/effectiveness.

If improvement can be made, a reference has been made to the Issues & Observations section, where management’s change

implementation plan is described.

14

13

14

5, 7

1

8, 9

8, 10

1

8

14

25.

Report Date, 200xPage 25

Appendix D: Best Practices Detail

1. Strengthen cash flow by explicitly managing payment

dates and terms

• Negotiate lenient credit terms with supplier.

• Reduce late fees and interest charges with on-time

payments.

• Pay early to take advantage of prompt-payment

discounts.

• Define cash flow objectives and set specific targets e.g.

average days in accounts payable or accounts payable

turnover.

Benefits include:

• Provides more flexibility to the company.

• Maximize cash flows resulting from lower interest costs

and liquidity improvements.

2. Manage communication with suppliers to establish

mutually agreeable practices.

• Evaluate cash flow circumstances and agree to realistic

payment terms.

• Renegotiate the terms if previous ones cannot be met.

• Solicit suppliers’ advice on AP improvements and

provide them with feedback on their role in the payment

process.

Benefits include:

• Enables quick and straightforward work of processing

payment.

• The reciprocal arrangement works well for all parties.

The company has negotiated standard

payment terms and discounts with major

vendors.

As of October 200X, the AP department

has implemented new system functions to

enable printing of checks that have been

processed and are eligible for early

payment discounts.

The company does not calculate monthly

cost or savings resulting from AP functions.

The AP group does not use specific

performance measures, such as average

days in AP and AP-turnover, to improve the

process.

Purchasing determines payment terms up

front when contracting with a vendor. In

most cases, standard terms are negotiated

to be net 30 days.

Returns and potential credit memos are not

always communicated to AP. Credit

memos have not been resolved in a timely

manner.

Rating: Moderate Use

Good Limited/Some Use

14

13

Best Practice Company Practice Evaluation / Reference

26.

Report Date, 200xPage 26

Appendix D: Best Practices Detail

3. Analyze money, quality and time in the current AP

process

• Map the AP process and transaction volumes.

• Measure the company’s invoice-processing capacities,

pinpoint bottlenecks in the workflow to create plan for

process improvement.

Benefits include:

• Provides information on bottlenecks and repetitive errors

that would allow for process efficiency improvement.

4. Implement rigorous, pervasive policies to protect against

disbursement fraud and overpayments

• Adopt a code of ethics throughout organization.

• Secure sensitive financial property.

• Segregate duties in purchasing, receiving, and finance.

• Carefully test and monitor computer system changes and

passwords.

Benefits include:

• Reduces possibility of financial fraud.

The AP department understands on a high

level how many invoices and checks are

processed under the existing operational

procedures.

However, there are no performance

measures to allow for process efficiency

improvements.

Code of ethics are signed and renewed

annually.

Purchasing, receiving and finance duties

are segregated. The AP department also

keeps duties such as disbursing funds and

reconciling bank accounts segregated.

Physical limits to sensitive financial

properties such as check stock and check

printing facility are in place. The AP

department works in partnership with the IT

group to implement changes to AP

systems.

However, password changes for check

printing applications do not conform to

corporate policy. Also, there is no formal

AP policy.

14

5, 7

Best Practice Company Practice Evaluation / Reference

Rating: Moderate Use

Good Limited/Some Use

27.

Report Date, 200xPage 27

Appendix D: Best Practices Detail

5. Establish controls appropriate to the risk and value of

corresponding transactions

• Set appropriately high threshold for accounts payable

proofreading, that is, checking the arithmetic on invoices.

• Set appropriately high thresholds for supervisory

approvals.

• Some companies eliminate invoices relying on invoice

approval and match purchase orders with receiving

information to create of vouchers.

Benefits include:

• Reduction of non-value added activities in the process

e.g. error correction.

• Builds in quality and customer satisfaction.

6. Reduce the volume of accounts payable transactions

• Implement purchasing card programs.

• Reduce number of invoices per supplier by using

summary invoicing.

Benefits include:

• Reduces volumes of transactions and paperwork.

The company has set purchase requisition

approval thresholds according to nature of

purchase and personnel position.

However, thresholds need to be updated

and correspond to limits set up in system.

Also, Matching criteria are set up in system

when generating a purchase order.

Check registers are reviewed by AP

personnel and Financial Systems Manager

periodically.

The company has implemented a

purchasing card program. However, per

review of payment details, we noted

approximately 67% of payments generated

in three months were for invoices below

$1,000.

1

8, 9

Best Practice Company Practice Evaluation / Reference

Rating: Moderate Use

Good Limited/Some Use

28.

Report Date, 200xPage 28

Appendix D: Best Practices Detail

7. Reduce processing costs and cycle times for smaller,

recurring invoices as well as T&E report processing

• Reduce number of active vendors.

• Consolidate small invoices and process as bulks.

• Utilize electronic banking system for recurring costs.

• Streamline invoice processing procedures.

Benefits include:

• Reduction of AP processing costs.

• Allow more time for value adding activities.

8. Integrate accounts payable with related operations

• Centralize accounts payable operations.

• Integrate the accounts payable function with purchasing,

receiving, and treasury by using integrated software

programs and shared data files.

Benefits include:

• Process that operates with fewer people while handling a

large volume of transactions in all related areas.

• Eliminates duplication of functions.

There are duplicate vendors in the master

vendor database. The majority of

processed invoices are of small dollar

value. T&E reports are processed through

a third party program.

The company’s AP function is

decentralized. There are local AP

personnel at plants to process invoices.

The AP department is the central location

to generate disbursement checks.

Purchasing and receiving functions are in

the accounting system. Two / three way

matches are also performed in the System.

8, 10

1

Best Practice Company Practice Evaluation / Reference

Rating: Moderate Use

Good Limited/Some Use

29.

Report Date, 200xPage 29

Appendix D: Best Practices Detail

9. Process accounts payable electronically

• AP and purchasing periodically review vendor lists and

banks for EDI candidates.

• All AP personnel receive comprehensive training to

utilize EDI effectively.

• Feedback mechanisms are in place with EDI partners to

review goals/objectives and generate improvement

ideas.

Benefits include:

• Reduces non-value added steps in the process creating

a more efficient process.

• Electronic data transfers reduce the cost of generating

checks and protecting them from fraud.

• Eliminates the cost to store data in the files and improves

the efficiency of search.

10. Use performance measures to achieve overall Accounts

Payable efficiency improvements

• Measure AP process efficiency and effectiveness by

using appropriate performance measures.

• Reward employees demonstrating efficiency

improvements.

• Set up incentives for quality and efficiency

improvements.

Benefits include:

• Improved efficiency in AP process.

• Heightened employee morale.

Many aspects of the AP function are still

manually driven. The company pays most

of its suppliers with paper checks instead of

using an electronic system. There is also

no integrated procurement system linked to

their vendors (EDI).

The AP department has not established a

set of key performance measures to

monitor the AP activities.

8

14

Best Practice Company Practice Evaluation / Reference

Rating: Moderate Use

Good Limited/Some Use

30.

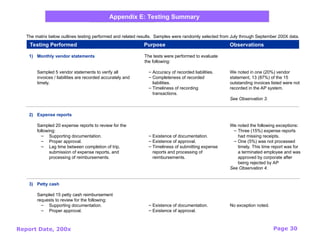

Report Date, 200xPage 30

1) Monthly vendor statements

Sampled 5 vendor statements to verify all

invoices / liabilities are recorded accurately and

timely.

2) Expense reports

Sampled 20 expense reports to review for the

following:

– Supporting documentation.

– Proper approval.

– Lag time between completion of trip,

submission of expense reports, and

processing of reimbursements.

3) Petty cash

Sampled 15 petty cash reimbursement

requests to review for the following:

– Supporting documentation.

– Proper approval.

The tests were performed to evaluate

the following:

– Accuracy of recorded liabilities.

– Completeness of recorded

liabilities.

– Timeliness of recording

transactions.

– Existence of documentation.

– Existence of approval.

– Timeliness of submitting expense

reports and processing of

reimbursements.

– Existence of documentation.

– Existence of approval.

Testing Performed Purpose Observations

Appendix E: Testing Summary

The matrix below outlines testing performed and related results. Samples were randomly selected from July through September 200X data.

We noted in one (20%) vendor

statement, 13 (87%) of the 15

outstanding invoices listed were not

recorded in the AP system.

See Observation 3.

We noted the following exceptions:

– Three (15%) expense reports

had missing receipts.

– One (5%) was not processed

timely. This time report was for

a terminated employee and was

approved by corporate after

being rejected by AP

See Observation 4.

No exception noted.

31.

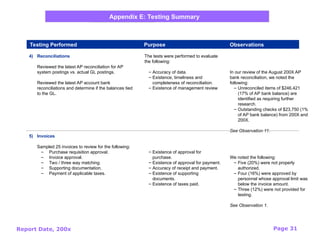

Report Date, 200xPage 31

4) Reconciliations

Reviewed the latest AP reconciliation for AP

system postings vs. actual GL postings.

Reviewed the latest AP account bank

reconciliations and determine if the balances tied

to the GL.

5) Invoices

Sampled 25 invoices to review for the following:

– Purchase requisition approval.

– Invoice approval.

– Two / three way matching.

– Supporting documentation.

– Payment of applicable taxes.

The tests were performed to evaluate

the following:

– Accuracy of data.

– Existence, timeliness and

completeness of reconciliation.

– Existence of management review

– Existence of approval for

purchase.

– Existence of approval for payment.

– Accuracy of receipt and payment.

– Existence of supporting

documents.

– Existence of taxes paid.

Testing Performed Purpose Observations

Appendix E: Testing Summary

In our review of the August 200X AP

bank reconciliation, we noted the

following:

– Unreconciled items of $246,421

(17% of AP bank balance) are

identified as requiring further

research.

– Outstanding checks of $23,750 (1%

of AP bank balance) from 200X and

200X.

See Observation 11.

We noted the following:

– Five (20%) were not properly

authorized.

– Four (16%) were approved by

personnel whose approval limit was

below the invoice amount.

– Three (12%) were not provided for

testing.

See Observation 1.

32.

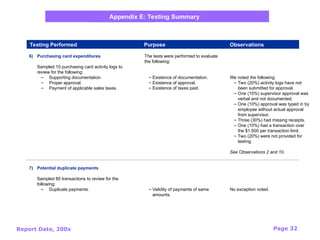

Report Date, 200xPage 32

6) Purchasing card expenditures

Sampled 10 purchasing card activity logs to

review for the following:

– Supporting documentation.

– Proper approval.

– Payment of applicable sales taxes.

7) Potential duplicate payments

Sampled 80 transactions to review for the

following:

– Duplicate payments.

The tests were performed to evaluate

the following:

– Existence of documentation.

– Existence of approval.

– Existence of taxes paid.

– Validity of payments of same

amounts.

Testing Performed Purpose Observations

Appendix E: Testing Summary

We noted the following:

– Two (20%) activity logs have not

been submitted for approval.

– One (10%) supervisor approval was

verbal and not documented.

– One (10%) approval was typed in by

employee without actual approval

from supervisor.

– Three (30%) had missing receipts.

– One (10%) had a transaction over

the $1,500 per transaction limit.

– Two (20%) were not provided for

testing.

See Observations 2 and 10.

No exception noted.

33.

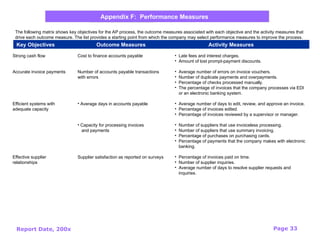

Report Date, 200xPage 33

Appendix F: Performance Measures

The following matrix shows key objectives for the AP process, the outcome measures associated with each objective and the activity measures that

drive each outcome measure. The list provides a starting point from which the company may select performance measures to improve the process.

Strong cash flow

Accurate invoice payments

Efficient systems with

adequate capacity

Effective supplier

relationships

• Late fees and interest charges.

• Amount of lost prompt-payment discounts.

• Average number of errors on invoice vouchers.

• Number of duplicate payments and overpayments.

• Percentage of checks processed manually.

• The percentage of invoices that the company processes via EDI

or an electronic banking system.

• Average number of days to edit, review, and approve an invoice.

• Percentage of invoices edited.

• Percentage of invoices reviewed by a supervisor or manager.

• Number of suppliers that use invoiceless processing.

• Number of suppliers that use summary invoicing.

• Percentage of purchases on purchasing cards.

• Percentage of payments that the company makes with electronic

banking.

• Percentage of invoices paid on time.

• Number of supplier inquiries.

• Average number of days to resolve supplier requests and

inquiries.

Cost to finance accounts payable

Number of accounts payable transactions

with errors

• Average days in accounts payable

• Capacity for processing invoices

and payments

Supplier satisfaction as reported on surveys

Key Objectives Outcome Measures Activity Measures

34.

Report Date, 200xPage 34

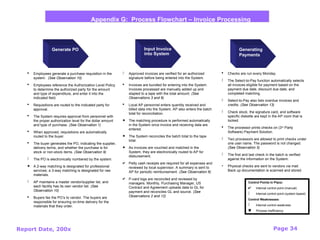

Input Invoice

into System

Generating

Payments

Generate PO

Employees generate a purchase requisition in the

system. (See Observation 10)

Employees reference the Authorization Level Policy

to determine the authorized party for the amount

and type of expenditure, and enter it into the

indicated field.

Requisitions are routed to the indicated party for

approval.

The System requires approval from personnel with

the proper authorization level for the dollar amount

and type of purchase. (See Observation 1)

When approved, requisitions are automatically

routed to the buyer.

The buyer generates the PO, indicating the supplier,

delivery terms, and whether the purchase is for

stock or non-stock items. (See Observation 9)

The PO is electronically numbered by the system.

A 2-way matching is designated for professional

services; a 3-way matching is designated for raw

materials.

AP maintains a master vendor/supplier list, and

each facility has its own vendor list. (See

Observation 10)

Buyers fax the PO’s to vendor. The buyers are

responsible for ensuring on-time delivery for the

materials that they order.

Approved invoices are verified for an authorized

signature before being entered into the System.

Invoices are bundled for entering into the System.

Invoices processed are manually added up and

stapled to a tape with the total amount. (See

Observations 3 and 8)

Local AP personnel enters quantity received and

billed data into the System. AP also enters the batch

total for reconciliation.

The matching procedure is performed automatically

in the System once invoice and receiving data are

entered.

The System reconciles the batch total to the tape

total.

As invoices are vouched and matched in the

System, they are electronically routed to AP for

disbursement.

Petty cash receipts are required for all expenses and

reviewed by local supervisor. A summary is sent to

AP for periodic reimbursement. (See Observation 6)

P-card logs are reconciled and reviewed by

managers. Monthly, Purchasing Manager, US

Contract and Agreement uploads data to GL for

payment and reconciles GL and source. (See

Observations 2 and 12)

Checks are run every Monday.

The Select-to-Pay function automatically selects

all invoices eligible for payment based on the

payment due date, discount due date, and

completed matching.

Select-to-Pay also lists overdue invoices and

credits. (See Observation 13)

Check stock, the signature card, and software

specific diskette are kept in the AP room that is

locked.

The processor prints checks on (3rd

Party

Software) Payment Solution.

Two processors are allowed to print checks under

one user name. The password is not changed.

(See Observation 5)

The first and last check in the batch is verified

against the information on the System.

• Physical checks are sent to vendors via mail.

Back up documentation is scanned and stored.

Control Points In Place:

Internal control point (manual)

Internal control point (system based)

Control Weaknesses:

Internal control weakness

Process Inefficiency

Appendix G: Process Flowchart – Invoice Processing

35.

Report Date, 200xPage 35

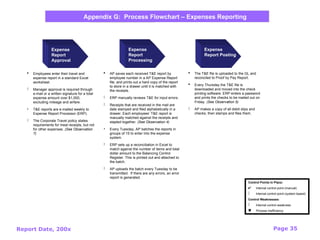

Expense

Report

Processing

Expense

Report Posting

Expense

Report

Approval

Employees enter their travel and

expense report in a standard Excel

worksheet.

Manager approval is required through

e-mail or a written signature for a total

expense amount over $1,000,

excluding mileage and airfare.

• T&E reports are e-mailed weekly to

Expense Report Processor (ERP).

The Corporate Travel policy states

requirements for meal receipts, but not

for other expenses. (See Observation

7)

AP saves each received T&E report by

employee number in a AP Expense Report

file, and prints out a hard copy of the report

to store in a drawer until it is matched with

the receipts.

ERP manually reviews T&E for input errors.

Receipts that are received in the mail are

date stamped and filed alphabetically in a

drawer. Each employees’ T&E report is

manually matched against the receipts and

stapled together. (See Observation 4)

• Every Tuesday, AP batches the reports in

groups of 15 to enter into the expense

system.

ERP sets up a reconciliation in Excel to

match against the number of items and total

dollar amount to the Balancing Control

Register. This is printed out and attached to

the batch.

AP uploads the batch every Tuesday to be

transmitted. If there are any errors, an error

report is generated.

The T&E file is uploaded to the GL and

reconciled to Proof by Pay Report.

Every Thursday the T&E file is

downloaded and moved into the check

printing software. ERP enters a password

and prints the checks to be mailed out on

Friday. (See Observation 5)

AP makes a copy of all debit slips and

checks, then stamps and files them.

Appendix G: Process Flowchart – Expenses Reporting

Control Points In Place:

Internal control point (manual)

Internal control point (system based)

Control Weaknesses:

Internal control weakness

Process Inefficiency