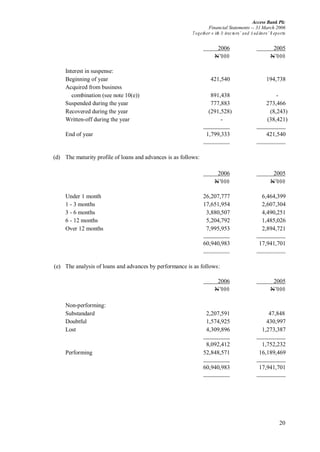

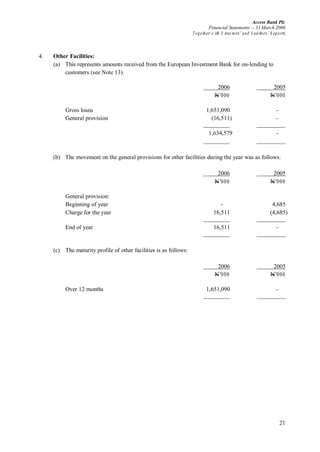

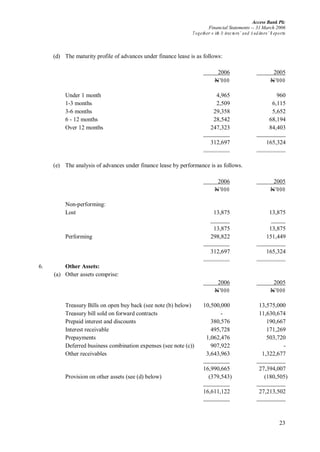

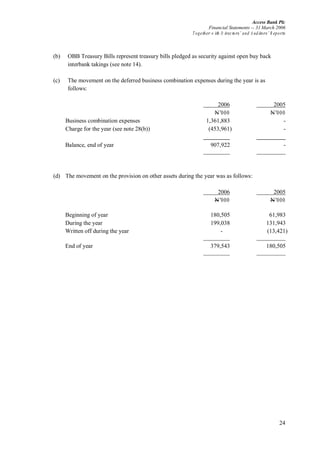

Downloaded 43 times

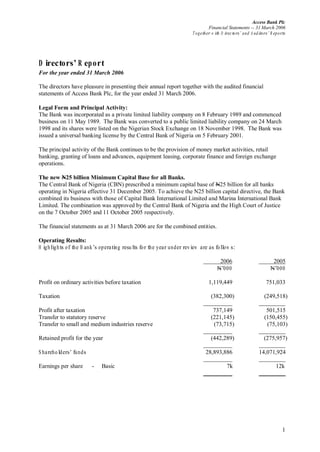

- Access Bank Plc combined its business with two other banks, Capital Bank International Limited and Marina International Bank Limited, to achieve the Central Bank of Nigeria's new minimum capital requirement of N25 billion. - For the year ended 31 March 2006, the bank reported a profit after tax of N737.1 million, up from N501.5 million the previous year. - The directors are responsible for preparing the financial statements to give a true and fair view of the bank's financial position and for ensuring appropriate internal controls and compliance with accounting standards.