Downloaded 29 times

![34 A Starter’s Guide to Sustainability Reporting

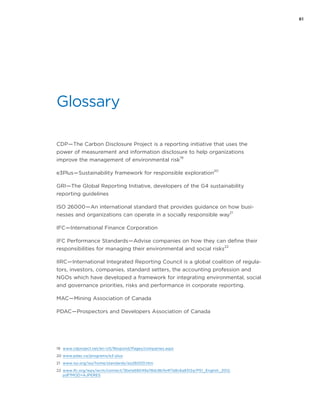

c) Suncor: Articulating a long-term strategy that aligns responsible

development with “unlocking its full potential”

http://sustainability.suncor.com/2013/en/about/vision-strategy.aspx[12/16/2013 2:58:46 PM]

Being our best. Giving our best. Showing we care.

Do the right thing

The right way, with integrity.

Raise the bar

Pursue with passion. Always add value.

Commitments matter

We are all connected and part of something bigger.

Strategy and responsible development

Suncor's long-term strategy leverages our competitive differentiators

and paves the way to unlocking the company's full potential for our

employees, our shareholders and our stakeholders.

Profitably operate and develop our oil sands resources

We are committed to getting the most value from our resources, which

include a significant position in the oil sands. Our operational excellence

focus is helping unlock the full value of these resources.

Optimize value through integration

From the ground to the gas station, we're focused on creating value for

our shareholders. The integration of our business, both financially and

physically, creates the conditions for our success.

Achieve industry-leading unit costs in each business segment

We aim to achieve the highest returns possible from our operations. Our

focus is on keeping costs down and increasing reliability. Our integrated

operating model also allows us to capture economies of scale.

Industry leader in sustainable development

We are focused on delivering triple bottom line sustainability. That

means leadership in:

environmental performance

social responsibility

creating a strong economy

One world. One future.

Actions speak louder than words. And while our vision statement has

evolved, our commitment to sustainable development remains

steadfast.

Here are a few concrete initiatives where we have put the principles of

sustainable development into practice:

Source: Suncor Report on Sustainability 2013 — online reporting](https://image.slidesharecdn.com/astartersguidetosustainabilityreporting-140331113323-phpapp01/85/A-Starters-Guide-to-Sustainability-Reporting-44-320.jpg)

The 'Starter's Guide to Sustainability Reporting' from CPA Canada aims to assist first-time and early-stage reporting companies in navigating their sustainability reporting journey, covering essential guidelines and practical examples. It highlights the increasing importance of transparency in sustainability performance among investors, customers, and other stakeholders, emphasizing the need for a structured approach to reporting. The guide also discusses reporting trends, methodologies, and the benefits of effective sustainability reporting for improving corporate performance and stakeholder engagement.