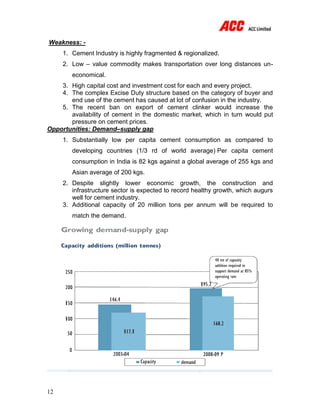

This document provides an overview and analysis of the Indian cement industry and the financial performance of ACC Ltd. It includes an introduction, objectives, methodology, industry analysis using Porter's five forces model and SWOT analysis. It also provides details about ACC Ltd such as its history, plants and capacity, vision, achievements and 5-year performance highlights. The document analyzes ACC's working capital management practices including inventory, cash, receivables and payables management. It presents various financial ratios and findings from the analysis. The summary aims to provide a high-level understanding of the document.