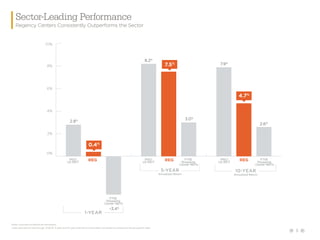

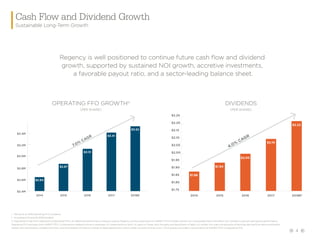

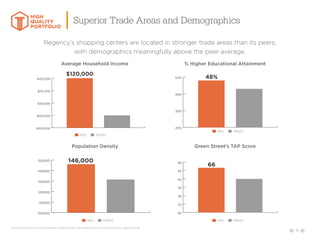

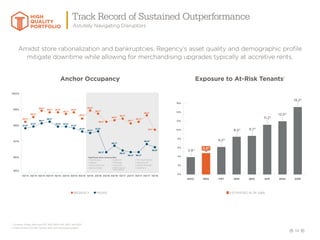

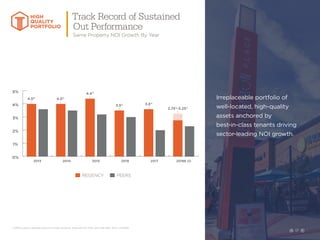

Regency Centers is a leading national shopping center REIT with 428 properties strategically located in affluent markets, focused on growth through high-quality tenant relationships and a disciplined financial approach. The company continues to outperform its sector, demonstrating resilience to store closures, while emphasizing a balanced portfolio anchored by necessity, service, and convenience-oriented retailers. With a strong balance sheet and robust cash flow growth strategies, Regency is well-positioned for future investments and sustained NOI growth of over 3% annually.