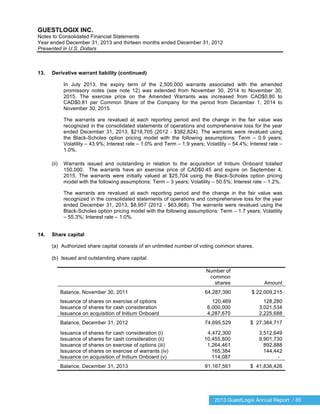

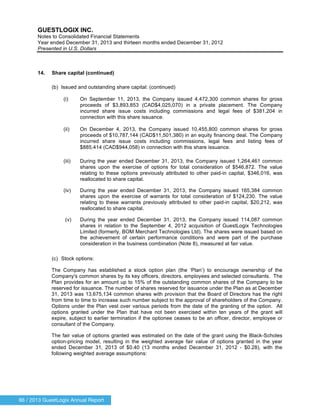

GuestLogix provides ancillary revenue processing solutions for the global travel industry. In 2013, the company experienced significant growth and transitioned its strategy to focus on expanding into new travel verticals, access points, and touch points. GuestLogix processed a record $917 million in transactions in 2013 and added 13 new customers. It also increased its payment and operational certifications to 82 total, solidifying its position as the most certified payment processor for onboard environments. Going forward, GuestLogix aims to leverage partnerships to transition from hardware-based to more software-based processing and continue delivering solutions to capture opportunities in ancillary revenue.