Downloaded 38 times

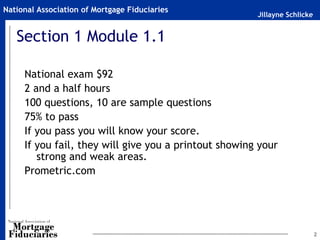

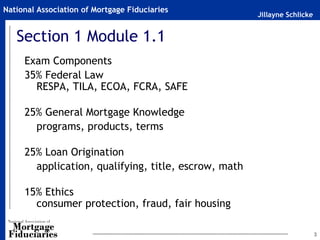

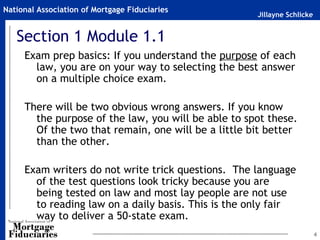

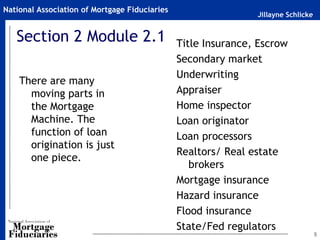

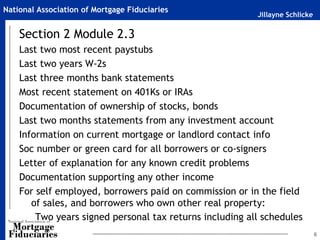

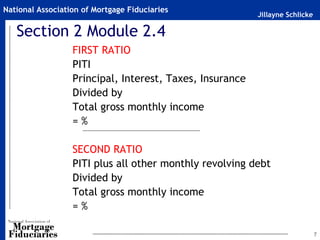

This document provides an overview of a 20-hour mortgage licensing course. It covers several key sections: 1. The national mortgage licensing exam costs $92, takes 2.5 hours, has 100 multiple choice questions including 10 sample questions, requires a 75% score to pass, and provides feedback on strong and weak areas. 2. The exam tests on federal law (35%), general mortgage knowledge (25%), loan origination (25%), and ethics (15%). 3. The document reviews important concepts like underwriting ratios, documentation requirements, title insurance, non-traditional lending guidelines, fiduciary duties, fair housing laws, consumer protection, and mortgage fraud. 4. Key laws covered include

![Caution Protect Yourself Report[1]](https://cdn.slidesharecdn.com/ss_thumbnails/cautionprotectyourselfreport1-1302618341-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)