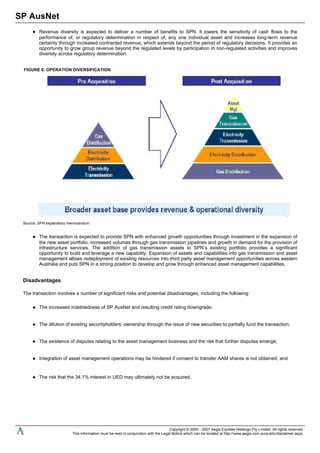

The Australian share market ended higher on Friday, led by gains in the financials and materials sectors. Coates Hire upgraded its guidance for FY08 operating earnings growth to 20%, while Babcock and Brown Infrastructure acquired interests in three overseas ports. US stocks ended little changed after mixed economic data, with jobs growth stronger than expected but consumer credit growth weaker. European stocks gained on hopes for US rate cuts, while commodities were mixed with copper hitting a one-week high.