Islamabad Escorts | Call 03274100048 | Escort Service in Islamabad

0Underpayment of Estimated Tax by Individuals

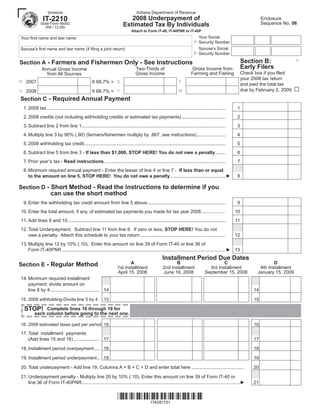

1. Indiana Department of Revenue

Schedule

IT-2210 2008 Underpayment of Enclosure

Sequence No. 06

Estimated Tax By Individuals

State Form 46002

(R8 / 12-08)

Attach to Form IT-40, IT-40PNR or IT-40P

Your Social

Your first name and last name

A Security Number

Spouse’s Social

Spouse’s first name and last name (if filing a joint return)

B Security Number

Section B: X

Section A - Farmers and Fishermen Only - See Instructions

Early Filers

Gross Income from

Two-Thirds of

Annual Gross Income

Check box if you filed

Farming and Fishing

Gross Income

from All Sources

your 2008 tax return

R 2007 X 66.7% = S T

and paid the total tax

□

due by February 2, 2009.

U 2008 X 66.7% = V W

Section C - Required Annual Payment

1. 2008 tax......................................................................................................................................... 1

2. 2008 credits (not including withholding credits or estimated tax payments) ................................. 2

3. Subtract line 2 from line 1.............................................................................................................. 3

4. Multiply line 3 by 90% (.90) (farmers/fishermen multiply by .667, see instructions) ...................... 4

5. 2008 withholding tax credit ............................................................................................................ 5

6. Subtract line 5 from line 3 - If less than $1,000, STOP HERE! You do not owe a penalty........ 6

7. Prior year’s tax - Read instructions ............................................................................................. 7

8. Minimum required annual payment - Enter the lesser of line 4 or line 7 - If less than or equal

to the amount on line 5, STOP HERE! You do not owe a penalty ..........................................► 8

Section D - Short Method - Read the instructions to determine if you

can use the short method

9. Enter the withholding tax credit amount from line 5 above............................................................ 9

10. Enter the total amount, if any, of estimated tax payments you made for tax year 2008................... 10

11. Add lines 9 and 10......................................................................................................................... 11

12. Total Underpayment. Subtract line 11 from line 8. If zero or less, STOP HERE! You do not

owe a penalty. Attach this schedule to your tax return ................................................................. 12

13. Multiply line 12 by 10% (.10). Enter this amount on line 39 of Form IT-40 or line 36 of

Form IT-40PNR .............................................................................................................................► 13

Installment Period Due Dates

A B C D

Section E - Regular Method 1st Installment 2nd Installment 3rd Installment 4th Installment

April 15, 2008 June 16, 2008 September 15, 2008 January 15, 2009

14. Minimum required installment

payment: divide amount on

line 8 by 4 ...................................... 14 14

15. 2008 withholding-Divide line 5 by 4 . 15 15

STOP! Complete lines 16 through 19 for

each column before going to the next one.

16. 2008 estimated taxes paid per period 16 16

17. Total installment payments

(Add lines 15 and 16) .................... 17 17

18. Installment period overpayment .... 18 18

19. Installment period underpayment .. 19 19

20. Total underpayment - Add line 19, Columns A + B + C + D and enter total here ........................................ 20

21. Underpayment penalty - Multiply line 20 by 10% (.10). Enter this amount on line 39 of Form IT-40 or

line 36 of Form IT-40PNR.........................................................................................................................► 21

*174081101*

174081101

2. Indiana Department of Revenue

Schedule

IT-2210 Underpayment of Estimated Tax by Individuals

WHAT is the purpose of Schedule IT- Line 1: 2008 Tax: Enter the state

Section D - Short Method instruc-

2210? This schedule is used for two tions on page 2. adjusted gross income tax, county

reasons: income tax, Indiana advance earned

• All taxpayers need to know about income credit payment and recapture

1. To help you figure any penalty you the short method of figuring the of Indiana’s CollegeChoice 529 credit

owe for not paying enough income tax penalty in Section D. from your individual income tax return.

throughout the year; or Add lines 16, 17, 20 and 21 from the

• If you received seasonal income (i.e.

2. To show you paid enough tax IT-40 or lines 12, 13, 16 and 17 from the

you had fireworks sales, you worked

throughout the year to be exempt from IT-40PNR and enter the total here.

during a Christmas season, etc.) that

the penalty.

is not evenly distributed throughout Line 2: 2008 Credits: Enter all your

WHY is a penalty charged? The In- the year, you might want to complete credits except withholding and estimat-

diana income tax system is a “pay Schedule IT-2210A, Annualized ed tax payments. Add lines 26 through

as you go” system. Many taxpayers Income Schedule. Annualization and including 31 from the IT-40 or lines

have enough taxes withheld from their could possibly reduce your required 22 through and including 28 from the

income throughout the year to cover installment tax payments. Contact IT-40 PNR and enter the total here.

their year-end total tax due. However, if the Department at (317) 615-2581 to

Line 4: To determine 90 percent of your

you don’t have taxes withheld from your get Schedule IT-2210A, or download

income, or if you don’t have enough it from the following Web address: total expected tax, multiply line 3 by 90

www.in.gov/dor/3910.htm

tax withheld from your income, you percent (.90).

may owe a penalty for underpaying

Note: If at least 2/3 of your gross in-

SECTION A -

estimated tax.

come is from farming or fishing, multi-

Farmers and Fishermen

ply line 3 by 66 2/3 percent (.667).

WHO should use Schedule IT-2210? If at least two-thirds of your gross

You should complete this schedule if : income for 2007 or 2008 was from

Line 5: 2008 Withholding: Your 2008

farming or fishing, you have only one

Indiana state and county income taxes

• the amount you owe for tax year payment due date for 2008 estimated

withheld from your earnings should

2008, after credits, is $1,000 or more tax - Jan. 15, 2009.

equal the combined line 23 (Indiana

for the year. The amount you owe is

state tax withheld) and line 24 (county

from IT-40, line 33 minus line 34, or To meet an exception to the underpay-

tax withheld) amounts from the IT-40

IT-40PNR, line 30 minus line 31; or ment penalty for 2008, you may use

or lines 19 and 20 from the IT-40PNR.

option 1 or 2:

Enter the total here.

• you underpaid the minimum amount

Option 1 - Pay all your estimated tax

due for one or more of the install-

Line 6: Subtract line 5 from line 3. If

ment periods. by Jan. 15, 2009, and file your Form

this amount is less than $1,000, you

IT-40 by April 15, 2009, OR

do not owe a penalty. Stop here and

Note: Form IT-40P filers must see

attach a copy of this schedule to your

Option 2 - File your Form IT-40 by

special instructions on page 3.

individual income tax return.

March 2, 2009, and pay all the tax

HOW much is the penalty? The penalty due. You are not required to make an Line 7: Prior Year’s Tax Exception:

is 10% of the underpayment for each estimated tax payment if you choose • If you filed a 2007 IT-40, add lines

installment period underpaid. That is this second option. If you pay all the 16 and 17 (your state and county

why Section E of this schedule is set tax due, you will not be penalized for income tax) from that return and

up by periods and should be filled out failure to pay estimated tax. subtract the total of lines 26, 27, 28,

one column at a time.

29 and 30 from that return. Enter the

SECTION B - Early Filers

result here. Note: See Caution box

WHAT DO I NEED to complete this If you file your individual income tax

on Page 2.

form? You’ll need a copy of: return and pay the tax due by Feb. 2,

2009, you will not be required to make

• If you filed a 2007 IT-40PNR as a

• your completed 2008 IT-40 or IT- a fourth installment estimated tax pay-

full-year nonresident, add lines 12

40PNR; ment. For additional information see

and 13 from that return and subtract

• your 2007 IT-40 or IT-40PNR; and the instructions for line 16.

the total of the lines 22, 23, 24, 25

• records of actual estimated tax pay-

and 26 from that return. Enter the

ments you made for 2008. SECTION C - Required Annual

result here. Note: See CAUTION

Payments

WHAT ELSE do I need to know about box on page 2.

Section C will determine if you should

this schedule? have paid estimated taxes during the year

• If you are a farmer or fisherman, you • If you filed a 2007 IT-40PNR as a

and the minimum amount required.

part-year resident of Indiana, you

should review Section A below and

1

3. must figure the tax for that year on Example for when 2007 IT-40PNR was filed as a part-year resident: you can

an annualized basis. See the instruc- accomplish this by multiplying the IT-40PNR line 1 income by 12 and dividing the

tion and Example for when 2007 result by the number of months you were an Indiana resident. Then figure the state

tax and county tax, if applicable, by 1) subtracting your 2008 exemptions from the

IT-40PNR was filed as a part-year

resident in the right-hand column. result and 2) multiplying that total by the combined state and applicable county

tax rate(s) from your 2008 Indiana individual income tax return. See the example

Line 8: Minimum Required Annual below. Note: See CAUTION box below.

Payment: Enter the lesser of line 4 or

line 7. If the line 7 entry is N/A, enter

the amount from line 4 on this line. Example:

Continue to Section D or Section E, • Jane moved to Indiana on Sept. 15, 2007, so she was a resident for 3.5 months.

whichever applies. • Her 2007 IT-40PNR line 1 income is $10,000.

• Her 2008 total exemptions are $3,500.

SECTION D - Short Method • The 2008 adjusted gross income tax rate is 3.4% (.034). Her 2008 county tax rate is

You can use the short method only if:

1% (for a 4.4% [.044] combined state and county tax rate.)

• you made no estimated tax

Use Steps 1 - 4 below to figure her prior year’s tax exception for line 7 of the IT-2210.

payments, or

Step 1 $ 10,000 2007 Indiana income

• you paid estimated tax in four equal

x 12 months

amounts by the due dates, or

$ 120,000 annualized income

• at least two-thirds of your gross

income from 2007 or 2008 was from

Step 2 $ 120,000 annualized income

farming or fishing and an estimated

÷ 3.5 months of 2007 residency

tax payment (if any) was made by

34,286

Jan. 15, 2009.

You can’t use the short method if either

Step 3 $ 34,286

of the following applies:

- 3,500 2008 exemptions

30,786

• you made any estimated tax pay-

ments late, or

Step 4 $ 30,786

• you made estimated payments in

x 4.4% 2008 combined state and county tax rate

unequal amounts.

$ 1,355*

SECTION E - Regular Method

* The $1,355 Step 4 amount should be entered as an exception on line 7 of

Use the regular method if you aren’t

Jane’s Schedule IT-2210.

eligible to use the short method.

If you are a fiscal year taxpayer, you

must change the dates in Columns

CAUTION: If your 2008 state taxable income (line 15 of Form IT-40 or line 11 of Form

A through D to correspond with your

IT-40PNR) is more than $150,000 ($75,000 for married individuals filing separately), you

fiscal year.

must enter 110% of last year’s tax (instead of 100%) on line 7.

Line 14: Minimum Required Install-

Example: Chris and Kate’s 2008 state taxable income from line 15 of Form IT-40 is $158,000.

ment: Divide the amount on line 8

They must take the following steps to arrive at the exception amount for line 7:

by four and enter the result in each

column.

a) 2007 IT-40 total income tax (line 16 plus line 17) .......................$ 6,952

b) 2007 IT-40 credits (lines 26 through and including 31) ..............- 1,952

If you are filing this year as a part-year

c) Subtotal ......................................................................................$ 5,000

resident on Form IT-40PNR, you must

d) Exception to the penalty percentage ..........................................x 110%

divide line 8 by the number of install-

e) Amount for line 7 of Schedule IT-2210 .......................................$ 5,500

ment periods during which you were a

resident of Indiana.

Note: If Chris and Kate’s 2008 state taxable income is less than $150,000, they would

enter $5,000 instead of $5,500 on line 7.

Installment periods are:

1st Period ..... Jan. 1 to March 31

2

4. 2nd Period ..... April 1 to May 31 ment payment in Column B on line 15 should then be added to line 16 in the

next column after subtracting any

3rd Period ..... June 1 to Aug. 31 will be $400 ($200 + $200).

4th Period ..... Sept. 1 to Dec. 31 underpayment(s) shown on line 19 in

Note for Early Filers: If you file your the previous column(s).

Line 15: 2008 Withholding: To deter- individual income tax return and pay

Note: If, after subtracting any under-

mine your installment period withhold- the tax due by Feb. 2, 2009, you

ing credit, divide the amount on line will not be required to make a 4th payments, this amount is less than

5 by four and enter the result in each installment estimated tax payment. You zero, no overpayment will be available

column. should include on line 16, Column D, to carry over to the next installment pe-

riod. Also, do not carry over a negative

the amount of tax you paid with your

STOP: Complete lines 16 through 19 tax return (Form IT-40 or IT-40PNR) figure if this amount is less than zero.

for each column before going to the minus any household employment

next column. tax, use tax, advance earned income Example: Dana had a $100 underpay-

credit payments, recapture of Indiana’s ment on line 19, Column A. She had a

Line 16: 2008 Estimated Taxes Paid: CollegeChoice 529 credit and/or the $130 overpayment on line 18, Column

Enter the actual amount of estimated amount shown on the return to be B. The net overpayment from the first

tax you timely paid for each installment applied to your 2008 estimated tax two installment periods is $30 ($130

period. Payments made after the due account. minus $100). She will add this net

dates at the top of each column are to overpayment to any estimated tax paid

Line 17: Total Installment Payments:

be reported in the next column. for the third installment period on line

To determine your total installment 16, Column C.

Example: Joe paid $800 in estimated payments, add lines 15 and 16 in each

Line 19: Installment Period Underpay-

taxes for 2008. His first installment pay- column and enter that column’s total

ment of $200 was not made until May 1 here. ment: If the total payment (line 17) is

(after the April 15 due date). His second less than the required tax (line 14) for

Line 18: Installment Period overpay-

installment payment of $200 was made an installment period, enter the differ-

on time by the June 16 due date. The ment: If the total payment (line 17) is ence on this line.

first installment payment in Column A more than the required payment due

Line 20: Total Underpayment: Add the

on line 15 will be -0- and the 2nd install- (line 14) for an installment period, enter

the difference on this line. This amount amounts from line 19, Columns A, B, C,

and D, and enter the total here.

A special note to prior year tax filers ...

Line 21: Underpayment Penalty: To

Individuals filing an Indiana individual income tax return for tax years 1996 or determine the amount of underpayment

before must file using Form IT-40P. For tax years beginning before 1997, you penalty you owe, multiply line 20 by 10

should complete this schedule if: percent and enter the amount here.

• the amount you owed for the year, after credits, was $100* or more for the This amount must also be entered on

year; line 39 of your 2008 IT-40 or line 36 of

your 2008 IT-40PNR.

or

Attach a copy of Schedule IT-2210

• you underpaid the minimum amount due for one or more of the installment to your tax return.

periods.

The Schedule IT-2210 instructions address 2008 Form IT-40 and IT-40PNR line

references and due dates. You must adjust those line references and due dates

to correspond with the tax year for which you are filing. For example, if you are

completing Form IT-40P for the 1996 tax year, where the Section C line 7 instruc-

tion refers to “last year’s tax”, it is referring to tax from your 1995 tax return.

* The 2008 version, line 6, states: “If less than $1,000, SToP HERE!”

• For tax years 1997 through 2007, the instructions should say: “If less than

$400, SToP HERE!” Estimated payments were required for those years if

owing $400 or more.

• For tax years 1996 or before, the instructions should say: “If less than $100,

SToP HERE!” Estimated payments were required for those years if owing

$100 or more.

Important: You must attach a copy of Schedule IT-2210 to your tax return if you meet an exception to the penalty

for the underpayment of estimated tax.

3