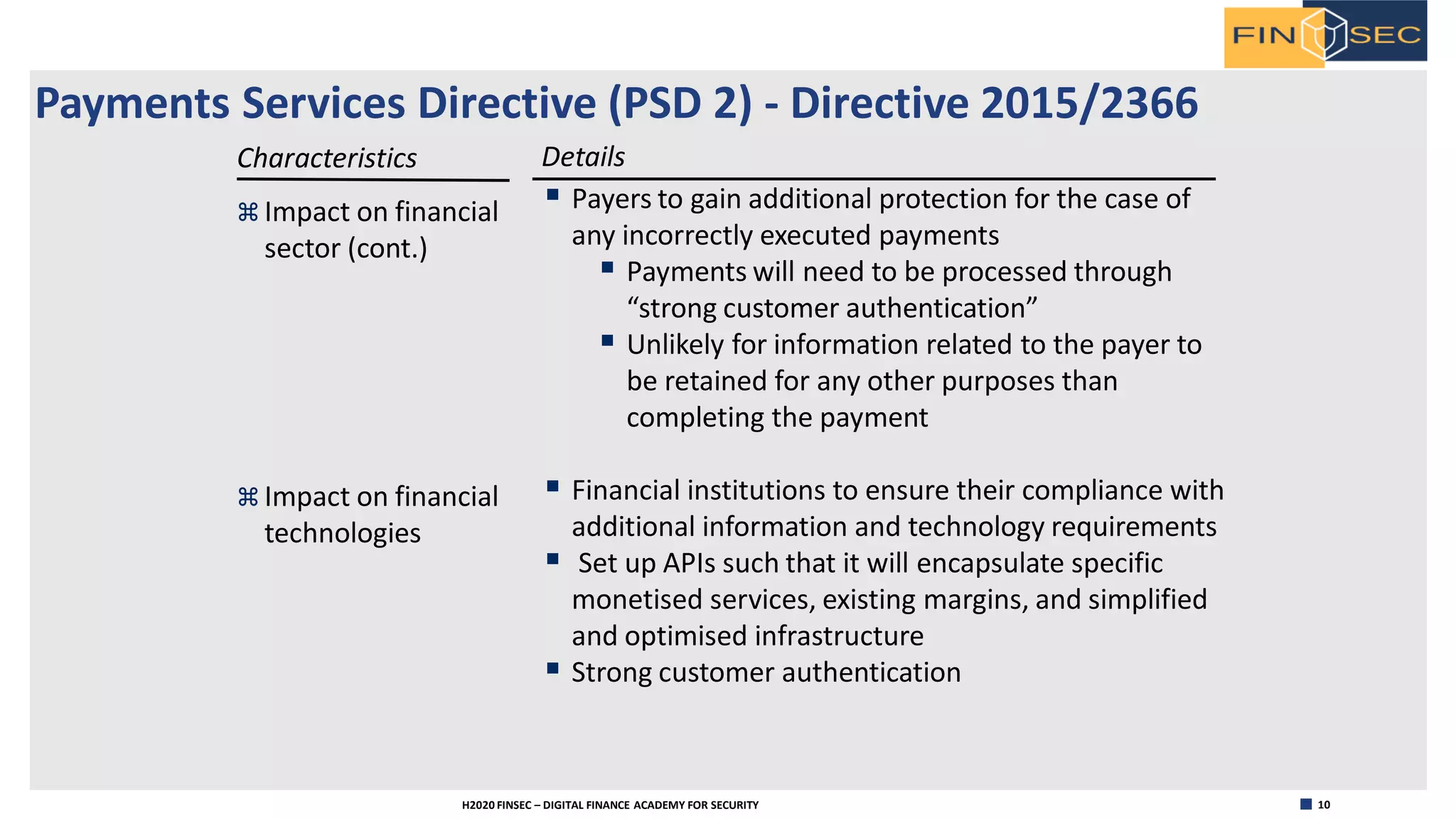

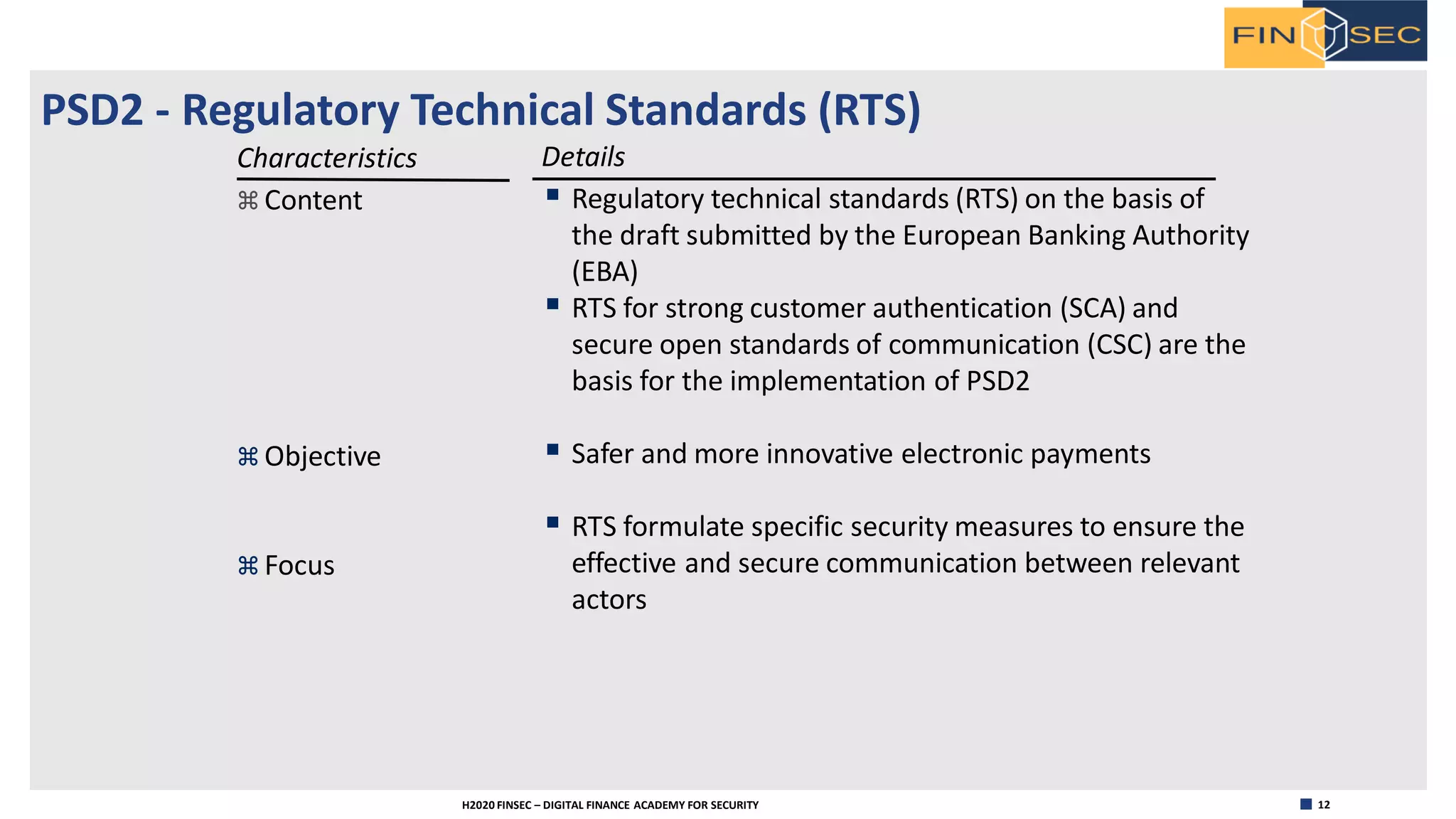

The document discusses various regulations that are relevant to the financial sector and their impact on financial technologies. It provides an overview of regulations such as MIFID II, PSD2, PCI DSS, and national regulatory bodies. For each regulation, it describes the objective, scope, and impact on the financial sector and financial technologies. The goal is to help learn about key financial regulations and understand how they influence the development of new financial technologies.

![[WSO2Con EU 2017] Fraud Prevention and Compliance in Financial Sector with WS...](https://cdn.slidesharecdn.com/ss_thumbnails/hgdjwoygqyqawlfcqfwy-signature-b521f0548f2a07c9bb75a715013744a23512b96bed5649fa80993361ce5d335a-poli-171107142024-thumbnail.jpg?width=640&height=640&fit=bounds)