Recommended

More Related Content

Similar to Problem 9-171.Collections on salesJulyAugustSept.Qua.docx

Similar to Problem 9-171.Collections on salesJulyAugustSept.Qua.docx (20)

More from sleeperharwell

More from sleeperharwell (20)

Recently uploaded

Recently uploaded (20)

Problem 9-171.Collections on salesJulyAugustSept.Qua.docx

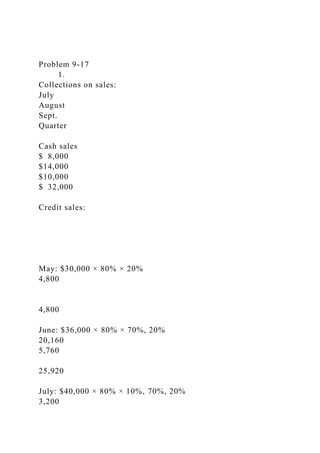

- 1. Problem 9-17 1. Collections on sales: July August Sept. Quarter Cash sales $ 8,000 $14,000 $10,000 $ 32,000 Credit sales: May: $30,000 × 80% × 20% 4,800 4,800 June: $36,000 × 80% × 70%, 20% 20,160 5,760 25,920 July: $40,000 × 80% × 10%, 70%, 20% 3,200

- 2. 22,400 6,400 32,000 Aug.: $70,000 × 80% × 10%, 70% 5,600 39,200 44,800 Sept.: $50,000 × 80% × 10% 4,000 4,000 Total cash collections $36,160 $47,760 $59,600 $143,520 2. a. Merchandise purchases budget: July August Sept. Oct. Budgeted cost of goods sold $24,000 $42,000 $30,000 $27,000 Add desired ending inventory* 31,500

- 3. 22,500 20,250 Total needs 55,500 64,500 50,250 Less beginning inventory 18,000 31,500 22,500 Required inventory purchases $37,500 $33,000 $27,750 *75% of the next month’s budgeted cost of goods sold. b. Schedule of expected cash disbursements for merchandise purchases: July August Sept. Quarter Accounts payable, June 30 $11,700 $11,700 July purchases

- 4. 18,750 $18,750 37,500 August purchases 16,500 $16,500 33,000 September purchases 13,875 13,875 Total cash disbursements $30,450 $35,250 $30,375 $96,075 3. Janus Products, Inc. Cash Budget For the Quarter Ended September 30 July August Sept. Quarter Cash balance, beginning $ 8,000 $ 8,410 $ 8,020

- 5. $ 8,000 Add collections from sales 36,160 47,760 59,600 143,520 Total cash available 44,160 56,170 67,620 151,520 Less disbursements: For inventory purchases 30,450 35,250 30,375 96,075 For selling expenses 7,200 11,700 8,500 27,400 For administrative expenses 3,600 5,200 4,100

- 6. 12,900 For land 4,500 0 0 4,500 For dividends 0 0 1,000 1,000 Total disbursements 45,750 52,150 43,975 141,875 Excess (deficiency) of cash available over disbursements (1,590) 4,020 23,645 9,645 Financing: Borrowings 10,000 4,000

- 7. 14,000 Repayment 0 0 (14,000) (14,000) Interest 0 0 (380) (380) Total financing 10,000 4,000 (14,380) (380) Cash balance, ending $ 8,410 $ 8,020 $ 9,265 $ 9,265 * $10,000 × 1% × 3 = $300 $4,000 × 1% × 2 = 80 $380

- 8. Problem 9-19 1. The sales budget for the third quarter: July Aug. Sept. Quarter Budgeted sales (pairs) 6,000 7,000 8,000 18,000 Selling price per pair × $50 × $50 × $50 × $50 Total budgeted sales $300,000 $350,000 $400,000 $900,000 The schedule of expected cash collections from sales: July Aug. Sept. Quarter Accounts receivable, beginning balance $130,000 $130,000

- 9. July sales: $300,000 × 40%, 50% 120,000 $150,000 270,000 August sales: $350,000 × 40%, 50% 140,000 $175,000 315,000 September sales: $400,000 × 40% 160,000 160,000 Total cash collections $250,000 $290,000 $335,000 $875,000 2. The production budget for July through October: July Aug. Sept. Oct. Budgeted sales (pairs) 6,000 7,000 8,000 4,000

- 10. Add desired ending inventory 700 800 400 300 Total needs 6,700 7,800 8,400 4,300 Less beginning inventory 600 700 800 400 Required production (pairs) 6,100 7,100 7,600 3,900 3. The direct materials budget for the third quarter: July Aug. Sept. Quarter Required production—pairs (above) 6,100 7,100 7,600

- 11. 20,800 Raw materials needs per pair × 2lbs. × 2lbs. × 2lbs. × 2lbs. Production needs (lbs.) 12,200 14,200 15,200 41,600 Add desired ending inventory 2,840 3,040 1,560 * 1,560 Total needs 15,040 17,240 16,760 49,040 Less beginning inventory 2,440

- 12. 2,840 3,040 2,440 Raw materials to be purchased 12,600 14,400 13720 40,720 Cost of raw materials to be purchased at $2.50 per lb. $31,500 $36,000 $34,300 $101800 *3,900 pairs (October) × 2 lbs. per pair= 7,800 lbs.; 7,800 lbs. × 20% = 1,560 lbs. The schedule of expected cash disbursements: July Aug. Sept. Quarter Accounts payable, beginning balance $11,400

- 13. $11,400 July purchases: $31,500 × 60%, 40% 18,900 $12,600 31,500 August purchases: $36,000 × 60%, 40% 21,600 $14,400 36,000 September purchases: $34,300 × 60% 20,850 20,850 Total cash disbursements $30,300 $34,200 $35,250 $99,750 Problem 9-26 1. Schedule of expected cash collections: January February March Quarter Cash sales $28,000

- 14. $32,000 $34,000 $ 94,000 Credit sales* 36,000 42,000 48,000 126,000 Total collections $64,000 $74,000 $82,000 $220,000 *60% of the preceding month’s sales. 2. Merchandise purchases budget: January February March Quarter Budgeted cost of goods sold (70% of sales) $49,000 $56,000 $59,500 $164,500 Add desired ending inventory* 11,200 11,900 7,700 7,700 Total needs 60,200 67,900

- 15. 67,200 172,200 Less beginning inventory 9,800 11,200 11,900 9,800 Required purchases $50,400 $56,700 $55,300 $162,400 *At March 30: April sales $55,000 × 70% × 20% = $7,700. Schedule of expected cash disbursements— merchandise purchases January February March Quarter December purchases $32,550 $ 32,550 January purchases 12,600 $37,800 50,400 February purchases

- 16. 14,175 $42,525 56,700 March purchases 13,825 13,825 Total disbursements $45,150 $51,975 $56,350 $153,475 3. Schedule of expected cash disbursements—selling and administrative expenses January February March Quarter Commissions $12,000 $12,000 $12,000 $36,000 Rent 1,800 1,800 1,800 5,400 Other expenses 5,600 6,400

- 17. 6,800 18,800 Total disbursements $19,400 $20,200 $20,600 $60,200 4. Cash budget: January February March Quarter Cash balance, beginning $ 6,000 $ 5,450 $ 5,275 $ 6,000 Add cash collections 64,000 74,000 82,000 220,000 Total cash available 70,000 79,450 87,275 226,000 Less cash disbursements: For inventory 45,150

- 18. 51,975 56,350 153,475 For operating expenses 19,400 20,200 20,600 60,200 For equipment 3,000 8,000 0 11,000 Total disbursements 67,550 80,175 76,950 224,675 Excess (deficiency) of cash 2,450 (725) 10,325 1,325 Financing: Borrowings 3,000 6,000 0 9,000 Repayments 0 0

- 19. (5,000) (5,000) Interest* 0 0 (210) (210) Total financing 3,000 6,000 (5,210) 3,790 Cash balance, ending $ 5,450 $ 5,275 $ 5,115 $ 5,115 * $3,000 × 1% × 3 = $ 90 $6,000 × 1% × 2 = 120 Total interest $210 5. Picanuy Corporation Income Statement For the Quarter Ended March 31 Sales ($70,000 + $80,000 + $85,000) $235,000

- 20. Cost of goods sold: Beginning inventory (Given) $ 9,800 Add purchases (Part 2) 162,400 Goods available for sale 172,200 Less ending inventory (Part 2) 7,700 164,500 Gross margin 70,500 Selling and administrative expenses: Commissions (Part 3) 36,000 Rent (Part 3) 5,400 Depreciation (Given) 2,400 Other expenses (Part 3) 18,800 62,600 Net operating income 7,900

- 21. Less interest expense 210 Net income $ 7,690 6. Picanuy Corporation Balance Sheet March 31 Assets Current assets: Cash (Part 4) $ 5,115 Accounts receivable ($85,000 × 60%) 51,000 Inventory (Part 2) 7,700 Total current assets 63,815 Fixed assets—net ($110,885 + $3,000 + $8,000 – $2,400) 119,485 Total assets $183,300 Liabilities and Equity

- 22. Accounts payable (Part 2: $55,300 × 75%) $ 41,475 Bank loan payable 4,000 Stockholders’ equity: Capital stock (Given) $100,000 Retained earnings* 37,825 137,825 Total liabilities and equity $183,300 * Retained earnings, beginning $30,135 Add net income 7,690 Retained earnings, ending $37,825 Problem 10-20 1. The activity variances are shown below: SecuriDoor Corporation Activity Variances For the Month Ended April 30

- 23. Planning Budget Flexible Budget Activity Variances Machine-hours (q) 20,000 18,000 Utilities ($16,500 + $0.15q) $ 19,500 $ 19,200 $ 300 F Maintenance ($38,600 + $1.80q) 74,600 71,000 3,600 F Supplies ($0.50q) 10,000 9,000 1,000 F Indirect labor ($94,300 + $1.20q) 118,300 115,900

- 24. 2,400 F Depreciation ($68,000) 68,000 68,000 0 Total $290,400 $283,100 $7,300 F The activity variances are all favorable because the actual activity was less than the planned activity and therefore all of the variable costs should be lower than planned in the original budget. 2. The spending variances are computed below: SecuriDoor Corporation Spending Variances For the Month Ended April 30 Flexible Budget Actual Results Spending Variances Machine-hours (q) 18,000 18,000

- 25. Utilities ($16,500 + $0.15q) $ 19,200 $ 21,300 $2,100 U Maintenance ($38,600 + $1.80q) 71,000 68,400 2,600 F Supplies ($0.50q) 9,000 9,800 800 U Indirect labor ($94,300 + $1.20q) 115,900 119,200 3,300 U Depreciation ($68,000) 68,000 69,700 1,700 U Total $283,100 $288,400 $5,300 U

- 26. An unfavorable spending variance means that the actual cost was greater than what the cost should have been for the actual level of activity. A favorable spending variance means that the actual cost was less than what the cost should have been for the actual level of activity. While this makes intuitive sense, sometimes a favorable variance may not be good. For example, the rather large favorable variance for maintenance might have resulted from skimping on maintenance. Since these variances are all fairly large, they should all probably be investigated. Problem 10-21 1. Verona Pizza Flexible Budget Performance Report For the Month Ended October 31 Planning Budget Activity Variances Flexible Budget Spending Variances Actual Results Pizzas (q1) 1,500 1,600 1,600 Deliveries (q2)

- 27. 200 180 180 Revenue ($13.00q1) $19,500 $1,300 F $20,800 $540 F $21,340 Expenses: Pizza ingredients ($4.20q1) 6,300 420 U 6,720

- 28. 130 U 6,850 Kitchen staff ($5,870) 5,870 0 5,870 60 F 5,810 Utilities ($590 + $0.10q1) 740 10 U 750 125 U 875 Delivery person ($2.90q2) 580 58 F 522 0 522 Delivery vehicle ($610 + $1.30q2) 870 26 F 844 138 U 982 Equipment depreciation ($384)

- 29. 384 0 384 0 384 Rent ($1,790) 1,790 0 1,790 0 1,790 Miscellaneous ($710 + $0.05q1) 785 5 U 790 12 F 778 Total expense 17,319 351 U 17,670 321 U 17,991 Net operating income $ 2,181 $ 949 F $ 3,130

- 30. $219 F $ 3,349 2. Some of the activity variances are favorable and some are unfavorable. This occurs because there are two cost drivers (i.e., measures of activity) and one is up and the other is down. The actual number of pizzas delivered is greater than budgeted, so the activity variance for revenue is favorable, but the activity variances for pizza ingredients, utilities, and miscellaneous are unfavorable. In contrast, the actual number of deliveries is less than budgeted, so the activity variances for the delivery person and the delivery vehicle are favorable. Problem 10-22 1. Performance should be evaluated using a flexible budget performance report. In this case, the report will not include revenues. KGV Blood Bank Flexible Budget Performance Report For the Month Ended September 30 Planning Budget Activity Variances Flexible Budget Spending Variances Actual Results Liters of blood collected (q) 600

- 31. 780 780 Medical supplies ($11.85q) $ 7,110 $2,133 U $ 9,243 $ 9 U $ 9,252 Lab tests ($14.35q) 8,610 2,583 U 11,193 411 F 10,782 Equipment depreciation ($1,900) 1,900 0 1,900 200 U

- 32. 2,100 Rent ($1,500) 1,500 0 1,500 0 1,500 Utilities ($300) 300 0 300 24 U 324 Administration ($13,200 + $1.85q) 14,310 333 U 14,643 68 F 14,575 Total expense $33,730 $5,049 U $38,779 $246 F $38,533 2. The overall unfavorable activity variance of $5,049 was caused by the 30% increase in activity. There is no reason

- 33. to investigate this particular variance. The overall spending variance is $246 F, which would seem to indicate that costs were well-controlled. However, the favorable $411 spending variance for lab tests is curious. The fact that this variance is favorable indicates that less was spent on lab tests than should have been spent according to the cost formula. Why? Did the blood bank get a substantial discount on the lab tests? Did the blood bank skimp on lab tests? If so, was this wise? In addition, the unfavorable spending variance of $200 for equipment depreciation requires some explanation. Was more equipment obtained to collect the additional blood?