Download to read offline

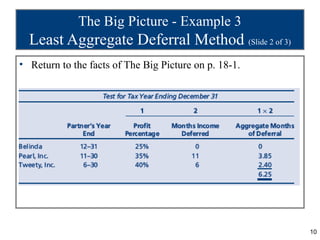

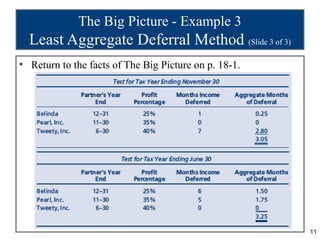

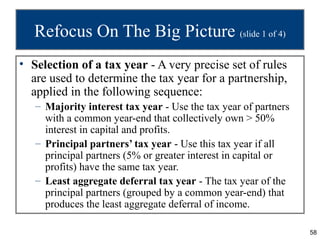

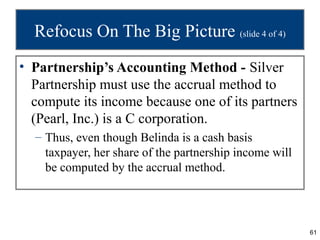

The document discusses accounting periods and methods for partnerships and partners. It addresses the following key points: - For the Silver Partnership example, the partnership tax year would end on November 30, as this results in the least aggregate deferral of income for the partners. - The partners would report their share of Silver's net income/loss on their tax returns for the year in which the partnership's tax year ends. - Belinda, as a cash-basis taxpayer, would report her share of partnership income using the cash method of accounting. - In general, a partnership tax year is determined based on the tax year of majority interest partners, then principal partners, and finally the method that results