This document analyzes tax increment financing (TIF) debt in the United States between 2000-2013. It finds that TIF debt issuance grew steadily until peaking in 2006, but then declined sharply during and after the Great Recession. Total TIF debt issued was over $37 billion, with about 75% issued before the recession. California was historically the largest issuer of TIF debt but eliminated redevelopment agencies in 2011. The recession significantly limited how local governments structured and sold TIF debt due to constrained capital markets and increased risk aversion by investors.

N a tio n a l Tax J o u rn a l, S e p te m b e r2 0 1 4 , 6 7 .docx

1. N a tio n a l Tax J o u rn a l, S e p te m b e r2 0 1 4 , 6 7 (3), 6

7 5 - 6 9 6

TA X IN C R E M E N T D E B T F IN A N C E A N D

T H E G R E A T R E C E S S IO N

Martin J. Luby and Tima Moldogaziev

This paper explores U.S. local government debt finance

activities related to Tax

Increment Financing (T1F) between 2000 and 2013. We gather

comprehensive data

about debt that is serviced through TIF, document changes in

several variables

related to the amount, use, and structural features o f such debt,

and evaluate the

impact o f the Great Recession on these variables. Our results

indicate that the

Great Recession limited how local governments could sell and

structure TIF debt.

We suggest that these limitations were the result o f the limited

capital available

during and immediately after thefinancial crisis, structural

changes in the financial

industry caused by the financial crisis, and increased risk

aversion by investors.

Keywords: Tax Increment Financing (TIF), property tax,

economic development,

Great Recession

JEL Codes: H71

2. I. INTRODUCTION

By design, tax increment financing (TIF) involves a delay

between the redevelopment costs paid and the project benefits

received. Because o f the mismatch between the

time o f incurring development costs and the receipt o f benefits

o f greater property or

sales tax revenues associated with economic development, TIF

naturally lends itself to

the use o f debt finance. Over the last several decades, many

local governments have used

debt instruments to securitize future tax revenues in order to

pay for current costs related

to the economic development o f the TIF district (Johnson,

1999). Such securitization

often involves the selling o f securities in the U.S. municipal

bond market. However,

the financial crisis o f 2007-2008 greatly affected the use and

structure o f the municipal

securities market (Johnson, Luby, and Moldogaziev, 2014). In

addition, the financial

crisis deflated the value o f one o f the primary repayment

pledges o f these TIF securities

M a rtin J. Luby: School o f P ublic Service, DePaul U

niversity, and In s titu te fo r G o v e rn m e n t and P ublic

Affairs,

U niversity o f Illinois, C hicago, IL, USA (m lu b y l @

depau!.edu)

T im a M o ld o g a z ie v : S chool o f P u b lic & In te rn a tio

n a l Affairs, U n iv e rs ity o f G eorgia, A th e n s, GA, USA

(tim atm @ u g a .ed u )

3. 676 National Tax Journal

in most areas o f the United States, namely the local property

tax base. For example,

the city o f Louisville, Kentucky recently nearly defaulted on its

2006 TIF bonds sold

to finance the KFC Yum! Center. TIF property tax revenues in

2012 amounted to $3.5

million with the expectation just a few years earlier that the TIF

district would generate

$8.2 million to pay the principal and interest payments on the

bonds in 2012 (Boyd,

2013). It is likely that the Great Recession’s impact on property

values significantly

contributed to the shortfall between expected and realized TIF

revenues in Louisville.

Given the extensive use o f municipal securities to finance TIF

capital projects over

the last several decades and the changes in the municipal

securities market and local

property tax base as a result o f the recent financial crisis, this

paper explores the use of

TIF debt finance before and after the Great Recession (i.e.,

during the period 2000-2013).

We gather data about debt that is serviced through TIF and

document changes in sev-

eral variables related to the amount, use and structural features

of such debt, focusing

our analysis on the impact the Great Recession had on these

variables. We also offer a

brief discussion on the possible future o f TIF debt finance in

the post-Great Recession

world.

4. II. TIF DEBT FINANCE MECHANICS

Before presenting data on the entire TIF industry from 2000-

2013, this section o f the

paper briefly details the purpose and mechanics o f TIF debt

finance. Local governments

generally use TIF debt finance, which often entails the sale of

municipal securities, for

three reasons (Johnson, 1999). First, as mentioned above, the

sale o f municipal securi-

ties allows the local government to quickly raise a large amount

o f financial resources

for TIF redevelopment projects. In the absence o f municipal

bonds, the local govern-

ment would have to rely on loans from banks and/or developers

or to significantly

decelerate the pace o f the redevelopment projects to be in line

with annual increases

in the tax base. In addition, municipal securities are generally

tax-exempt so the local

government receives the benefit o f lower cost financing with

municipal securities vis-

a-vis bank or developer loans. Second, TIF debt allows

municipalities to circumvent

constitutional or statutory debt restrictions, since TIF bonds are

generally not subject to

general obligation bond debt limitations or public referendum

requirements (Johnson,

1999; Briffault, 2010). Thus, local governments can access

redevelopment resources

without seeking legislative and/or public approval. Finally, TIF

provides local govern-

ments an opportunity to raise off-balance sheet capital financing

since the issuer o f TIF

bonds, generally a redevelopment agency, is usually not

considered part of the general

5. government. This serves to preserve the local government’s

borrowing capacity for

future capital projects. In essence, the basic pros and cons o f

pay-as-you-go financing

versus pay-as-you-use financing are present in the decision to

use TIF debt finance.

Local governments sell TIF bonds in the national municipal

bond market. The prevail-

ing feature o f this market is tax exemption. That is, the interest

on municipal securities

is generally exempt from federal income taxation. However,

federal tax regulations

specify that in order to qualify for such tax exemption, at least

95 percent o f the TIF

bond proceeds must be used for redevelopment purposes in a

“blighted” area, the issuer

T a x I n c r e m e n t D e b t F in a n c e a n d t h e G r e a t

R e c e s s io n 677

must have a redevelopment plan, and the pledge o f repayment

must be from general

taxes o f the government or from incremental taxes associated

with the project (Johnson,

1999). If these conditions are not met, the local government will

incur higher interest

costs as it will have to sell the debt on a taxable rather than tax-

exempt basis. As it

relates to amortization structure, local governments sell the debt

with a bond structure

that approximates the expected size o f the future incremental

tax revenues associated

with the redevelopment. That is, the local government amortizes

6. the TIF bonds over a

time period during which incremental revenues are expected to

be sufficient to pay the

principal and interest payments on the debt.

In the parlance o f the municipal bond market, TIF bonds

essentially represent a hybrid

general obligation/revenue bond credit structure (Geheb, 2009).

TIF debt appears to be

general obligation in nature in that ad-valorem property taxes

often secure repayment

on the bonds. However, TIF debt also carries a revenue bond

feature in that there is a

specific, identifiable revenue repayment source (i.e., the

incremental tax revenues) that

would not exist in the absence o f the redevelopment project.

Moreover, redevelopment

agencies, rather than the general government, are often the

issuer o f the TIF debt just as

other types o f government authorities are often issuers of

revenue bonds. This hybrid

structure has raised some constitutional issues related to the

level o f responsibility that

the general government has in “making whole” TIF bond

investors in the event o f a

default (Geheb, 2009). In the past, local governments have sold

much (although not all)

o f their TIF debt using a revenue bond structure (Johnson,

1999).

III. T H E T IF M U N IC IPA L SECURITIES MARKET, 2 0 0

0 -2 0 1 3

In this section o f the paper we discuss the data — the trends,

use, and structure of

TIF debt securities issued between January 1,2000 and

7. December 3 1 ,2 0 1 3 — with an

emphasis on the impact o f the Great Recession. This covers

several years before and

after the financial crisis of 2007-2008, including the years

before and after the Great

Recession. The database includes a list o f all TIF debt

securities sold during this time

period ( N= 2,478) as well as a spectrum o f features o f these

bond transactions. The data

for this descriptive analysis come from the Securities Data

Corporation (SDC).' This is

a fee-for-service database company that collects information on

all municipal securities

sales. Our review considers TIF market trends, the issuers and

uses o f TIF securities,

and the structure o f TIF securities. As such, the analysis

provides a complete picture of

the TIF municipal securities market over the last 14 years for

the period January 2000

through December 2013. We assess the distribution o f TIF

securities issuance data for

goodness-of-fit using Pearson’s and log-likelihood Chi-squared

tests o f independence,

which test the likelihood o f whether the observed annual

distributions for variables of

interest in this study are due to chance or whether there are

significant shifts in their

annual distributions during the period under examination. The

tests compare the observed

distributions in the data to the expected distributions based on

the assumption that the

variables are independent. While these tests do not provide

evidence o f the direction o f

These data are available at http://thomsonreuters.com/sdc-

platinum/.

8. 678 N ational Tax Journal

association between the variables o f interest, in our case, they

provide evidence on the

probability o f independence between each o f our variables o f

interest and annual TIF

bond issuance activity in 39 U.S. states and the District o f

Columbia.

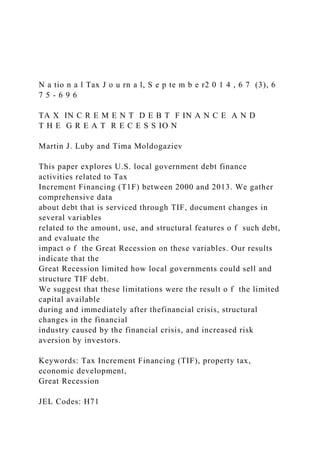

A. TIF M arket Trends

In the period, almost $37.6 billion in 2,478 separate TIF issues

were sold in the

municipal bond market. As seen Figure 1, the least TIF

issuance, both in terms o f

monetary volume and the number o f individual issues, was in

calendar year 2012. Only

65 TIF issues for a combined volume o f $449 million were

recorded in the municipal

market during that year. The largest volume o f TIF securities is

observed in 2006 with

almost $5 billion sold in 238 individual issues. Overall trends

show that TIF issuance

Figure 1

TIF Issuance Volume (SMillion) and Frequency in 39 U.S.

States and

the District o f Columbia, 2000-2013

6,000 300

5,000 250

9. = 4,000 200

3,000 150

~ 2,000 100

1,000 50

Year

SSSS! Frequency of TIF Issues ■ Grand Total

Source: Securities D ata C orpo ra tio n

T a x I n c r e m e n t D e b t F in a n c e a n d t h e G r e a t

R e c e s s io n 679

volume grew from under $2 billion in 2000 and 2001, to about

$2.7 billion in 2002, to

more than $4.8 billion in 2003, before declining to about $3.4

billion in 2004. In the

three years immediately before the Great Recession, years 2005,

2006, and 2007, TIF

issuance remained significantly above $4 billion. We find that

about 75 percent of all

TIF-related securities, more than $28 billion, were issued before

the Great Recession.

TIF volume, however, dropped dramatically during and after the

Great Recession.

Thus, in 2008 TIF issuance volume fell almost by half to about

$2.1 billion from the

pre-recession year’s level o f $4.2 billion. TIF volumes further

10. fell to about $1.5 billion

in 2009, climbed back to $ 1.8 and $2 billion in 2010 and 2011,

respectively, but shrunk

to less than half a billion in 2012. The TIF volume in 2013

appears to be about $1.5

billion. Only $9.5 billion was issued in TIF securities since the

Great Recession from

2008-2013. Consequently, it appears that there was a significant

decrease in TIF debt

activity in the municipal securities market since the Great

Recession. The volume o f

TIF bond sales decreased by 49 percent between 2007 and 2008

with every subsequent

year lower than the 2008 level, which suggests the detrimental

impact the financial crisis

may have had on the size o f the TIF bond market. Indeed, the

measures o f association

between the number o f TIF bond issues and the year o f

issuance provide evidence of

statistically significant changes in issuance trends in our sample

period. For the period

o f January 1, 2000 to December 31, 2013, Pearson’s Chi-

squared and log-likelihood

Chi-squared statistics are 818.1 and 730.1, respectively.

The State o f California has been the “market leader” in TIF

securities, except in 2012.

The dramatic decline in 2012 was a result of California’s

dissolution of its redevelopment

authorities in late 2011, which prohibited California local

governments from issuing any

new TIF bonds (Lefcoe and Swenson, 2014). California was a

pioneer in the use o f TIF

debt finance and was perennially the largest seller o f TIF bonds

prior to the elimination

in its redevelopment agencies. The steep drop between 2011 and

11. 2012 in the volume and

number of TIF transactions reflects this statutory change. In

2013 California returned as

the largest issuer o f TIF securities with 21 separate TIF issues

for a combined value of

$618 million. However, these municipal securities represented

refinancing o f existing

TIF securities, which were allowed under Assembly Bill 1484.

Refinancing of outstand-

ing TIF securities was allowable as long as the amount o f the

refinancing bond issue

was not greater than the amount o f refinanced bonds, and the

refinancing bond interest

costs were less than refinanced bond interest costs.2 In the

period under study, California

municipalities are directly responsible for over $25 billion in

TIF securities, which is

roughly about two-thirds o f the entire TIF activity in the

municipal securities market. A

total o f 59 municipal issuers from California appear to have

delivered at least $ 100 mil-

lion o f TIF securities each to the market, with the San Jose

City Redevelopment Agency

leading the way with almost $2.5 billion in 20 separate TIF

issues.

The data indicate a similar impact o f the Great Recession on

overall TIF debt finance

activity even if California is removed from the database. As

shown in Figure 2, the largest

2 County of Los Angeles Redevelopment Refunding Authority,

Tax Allocation Revenue Refunding Bonds,

Series 2013DEF, Official Statement, available at

http://emma.msrb.org/ER733654-ER569382-ER970689.pdf.

12. 680 N ational Tax Journal

F ig u re 2

TIF Issuance V olum e ($M illion) and Frequency 38 U.S. States

(Excluding

California) and th e D istrict o f C olum bia, 2000-2013

1,800

1,600

~ 1,400

C0

1 1,200

CD

§ 1,000

8 800 c

CO

I 600

LL

H 400

200

0

Year

Frequency of TIF Issues ■Grand Total

13. 180

160

140

120 |

=3

c r

<D

100 £

0)o

80 |

Uiu>

60 tfc I-

40

20

0

S o u rce : S e c u ritie s D a ta C o r p o r a tio n

and smallest volumes o f non-Califomia TIF issuance were in

2005 and 2012, respectively,

with a sharp decline in TIF transactions and volume between

2007 and 2008 and a steady

decline thereafter with an uptick in transaction frequency in

2013. Even after omitting

California issuers, the measures o f association between the

number o f TIF bond issues

and the year o f issuance provide evidence o f statistically

14. significant changes in issuance

trends in our sample period. For the period from 2000-2013,

Pearson’s Chi-squared

and log-likelihood Chi-squared statistics are 658.0 and 600.8,

respectively. Aside from

California, there are five states that have issued more than $ 1

billion each in TIF securi-

ties during the period under review. These states are Colorado,

Missouri, Minnesota,

Illinois, and Texas. In Figure 3, we depict aggregate annual

volumes in these top-five

TIF issuing states for 2000-2013. Though overall Colorado

leads the top-five list with

about $1.6 billion, its municipalities are the least frequent

market participants with only

41 separate TIF issues. Its biggest aggregate TIF issues o f $296

million and $266 million

Tax Increm ent Debt Finance and the Great Recession 681

682 N a tio n a l T a x J o u r n a l

are in 2004 and 2008, respectively. On the other hand,

Minnesota municipalities are the

most frequent TIF issuers with 410 separate TIF securities for a

combined volume of

$1.4 billion. Texas, Illinois, and Missouri appear to fall in

between Colorado and Min-

nesota in terms o f their transaction frequencies in the TIF

market.

B. Is s u e rs a n d U se s o f T IF S e c u r itie s

15. Not coincidentally, issuers from California dominate the TIF

market in the period.

O f the 10 largest issuers o f TIF securities (a combined volume

o f over $8 billion or

over 20 percent o f the entire industry in the period), eight are

in California. By far the

largest issuer o f TIFs in the US was the San Jose

Redevelopment Agency with almost

$2.5 billion in TIF securities (Table 1). The San Francisco City

& County Redevelop-

ment Agency issued over $1.1 billion during the same period.

Three remaining major

issuers in California were the Oakland Redevelopment Agency,

the San Diego Rede-

velopment Agency, and the Riverside County Public Finance

Authority — all with

TIF volumes exceeding $600 million. These top-5 issuers in

California accounted for

about 8 percent o f all TIFs in the state in 2001 and about 40

percent in 2009, with their

shares in other years falling somewhere between these extremes.

Nevertheless, despite

the continued activity in the TIF market by San Francisco City

& County-, Oakland-,

and San Diego Redevelopment Agencies since the Great

Recession, it is evident that

most o f the TIF activity for these top-5 California issuers

occurred before the Great

Recession.

As shown in Table 2, apart from California jurisdictions, the

Denver Urban Renewal

Authority is the largest issuer o f TIFs by volume in our sample.

It issued more than

$800 million in TIFs (or more than half o f all TIF securities

16. issued by Colorado

municipalities), with $171 million sold as recently as 2013.

Atlanta and Chicago are

next with $657 million (more than 96 percent o f TIF securities

in Georgia) and $476

million (over 37 percent o f the entire TIF issues in Illinois),

respectively. Minneapolis

and the Unified Government o f Wyandotte County & Kansas

City have sold $344 mil-

lion and $270 million in TIF securities each. These latter two

issuers accounted for a

significant fraction o f TIF securities from their states; about 26

percent for Minneapolis

and over 76 percent for Wyandotte County/Kansas City. The

Unified Government of

Wyandotte County & Kansas City has not returned to the TIF

market since 2005, how-

ever. When combined, these top-5 non-California issuers o f

TIF securities accounted

for about 2 percent o f all non-California issues in 2012, but

about 40 percent in

2000.

We classify the over thirty categories o f TIF debt uses

identified in the data into seven

broad categories. As Table 3 shows, general purpose/public

improvements are by far

the biggest share o f the TIF market in our sample with about

$20 billion in proceeds

(or about 53 percent o f all TIF volumes). Almost 80 percent o f

general purpose/public

improvements TIF securities were issued before the Great

Recession, however. Eco-

nomic development and industrial development TIFs are next in

volume. Over $13.5

billion were issued for these uses as TIF obligations. TIF

17. proceeds for these three major

T a x I n c r e m e n t D e b t F in a n c e a n d t h e G r e a t

R e c e s s io n 683

684 National Tax Journal

Tax Increm ent D ebt Finance and the Great Recession 685

686 N a tio n a l Tax J o u rn a l

uses accounted on average for 89 percent o f all TIF securities

in the m unicipal market.

The TIF m arket has thus been predom inantly a m arket for

general purpose/public

im provem ent and econom ic and industrial developm ent

projects.

The remaining annual volumes (on average roughly 11 percent o

f all TIF debt proceeds)

are used for transportation, housing, education and health, and

utilities, w ith housing,

both single and multifamily structures, adding up to more than

$2 billion. Transportation

uses, such as overland infrastructure, airports, and seaports,

accounted for more than

$1.6 billion o f TIF proceeds. Education TIFs, and to a lesser

extent healthcare related

18. uses, absorbed about $330 m illion o f debt proceeds. A very

small fraction o f the TIF

m arket ($ 184 m illion in our sample) is related to water,

sewer, and gas purposes, electric

and public pow er purposes, solid waste and recycling uses, as

well as hybrids o f these.

The economic development category generally shows a steady

decline in issuance

volume for the period from 2000 to the Great Recession period.

Increases in the general

purpose/public improvement category initially offset this

decline, but eventually decline

between 2007 and 2008. After 2008, the economic development

category increases while

the general purpose/public improvement category continues to

fall. W hile these category

names are somewhat generic (especially “general purpose/public

improvement”) and one

must use caution when drawing conclusions, the decline in

economic development TIF

bonds and the increase in general purpose/public improvement

TIF bonds suggests that

local governments no longer use TIF only for economic

development but also to finance

general governmental purposes. The uptick in economic

development bonds after 2009

and the decline in general purpose bonds may be the result o f

demands by municipal

bond investors for more specific details on the development

projects being financed rather

than loaning money for “general purpose projects” that are

financed by incremental tax

revenues. However, this conclusion is speculative and warrants

further systematic analysis.

19. A nother w ay to explore the use o f TIF proceeds is to look at

trends in the tax status

o f TIF securities. As stipulated in federal tax statute, typically

at least 95 percent o f the

use o f proceeds m ust be pledged for redevelopm ent purposes

in a “blighted” area to

attain tax exemption. Thus, analyzing the com position o f

bonds sold tax-exem pt versus

taxable m ay provide m ore insight into the purposes that local

governm ents have used

TIF debt, that is, w hether local governments have expanded

their use o f TIF debt finance

tools to fund redevelopm ent in non-blighted areas or not.

Figure 4 illustrates the volume

and percentage o f TIF bonds sold on a taxable basis. For m ost

years betw een 2000 and

2014, local governm ents consistently sold their TIF debt on a

tax-exem pt basis about

80 percent o f the tim e w ith the heaviest use o f taxable TIFs

in 2010, 2011, and 2013.

However, the overall volum es o f taxable bonds dropped dram

atically since the Great

Recession (i.e., taxable bond volum es in each year post-

recession w ere less than h a lf o f

the immediately pre-recession year levels). Private activity TIFs

generally are sponsored

by corporate sponsors and are alm ost always taxable securities.

However, during the

tim e period analyzed, only $347 m illion o f TIF issues (less

than 1 percent o f the entire

TIF market) were directly linked to corporate supporters as seen

in Figure 5. M ost o f

these were tied to pre-G reat R ecession years when private

funds w ere still relatively

abundant. Our data show that the frequencies o f issues for

taxable and corporate-backed

20. TIFs have decreased significantly, w ith P earson’s Chi-squared

and log-likelihood Chi-

squared statistics at 57.0 and 56.6 com pared to 17.8 and 17.6

respectively.

T ax I n c r e m e n t D e b t F in a n c e a n d t h e G r e a t

R e c e s s io n 687

C. Structure of TIF Securities

The overall volume o f TIFs has decreased since the Great

Recession and so did

average bond issue sizes. Mean bond sizes peaked in 2005-2007

and decreased

significantly by 2012 as reported in Figure 6. However, Figure

6 shows a larger

average bond size in 2013. Another typical measure o f bond

structure, length o f

maturity, is generally positively related to risk, with investors

demanding a higher

risk premium for longer term investments or generally deciding

to avoid longer-term

investments altogether in extreme circumstances. In this

context, one might expect

to see the average final maturity decline in the years after the

Great Recession as

TIF bonds became riskier in light of the financial crisis and its

effect on property

values. The results in Figure 7 show a decline in 2009, an

increase back to pre-recession

levels in 2010 and 2011, and then a significant decline in 2012

and 2013. However,

one needs to be careful in drawing any definitive conclusions

from final maturity data

21. without looking at times-to-call measures. As the measure o f

average years to call in

Figures 4 -7

Percentage o f Total TIF Issuance Volume and Select TIF

Features,

39 US States and the District o f Columbia, 2000-2013

30

25

P 20

CD

o 15

10o<D

CD

8 5

001

Figure 4 Taxable TIFs

i

1 :

ilI I

O CM ^ CD CO OO O O O O t-

O O O O O O

CM CM CM CM CM CM

Figure 5 Corporate Backed TIFs

120

22. C

O 100

80

<D

N

CO 60

0

=3

CD

(f)

40

LL

H

20

0 _ 1 - hi__

Figure 6 Average TIF Bond Issue Size

o CM CD 0 0 O CMo O O O Oo O O O O O O

CM CM CM CM CM CM CM

Figure 7 Average TIF Bond Final Maturity

O CM M - CD CO O CM

O O O O O

O O O O O O O

CM CM CM CM CM CM CM

23. 688 N a t io n a l T a x J o u r n a l

Figure 8 suggests, there was indeed a shortening o f time-to-call

that would fit such ex-

ante evaluations o f the market risk by the issuers o f TIF

securities.

The coupon interest rate sets the periodic interest payments on

local governments’

TIF bonds. In higher interest rate environments, coupon interest

rates are generally

higher and in lower interest rate environments, they are

generally lower. However, the

coupon interest rate is not the same as the yield that investors

will receive (issuers will

pay) because it does not take into account call provisions or the

price of the securities.

In Figure 9 the average highest coupon increases after 2007, and

moves downward in

2012. This is especially interesting because interest rates

generally declined after 2007

as a result o f the financial crisis, as the Federal Reserve Bank

cut its benchmark interest

rate several times and continued to maintain low interest rates

well into 2014. If there

was not an interest rate risk premium that investors were

building into TIF bond inter-

est rates, we would expect to see the average highest coupon

rate decline after 2007 in

line with the general decline in interest rates. In fact, the

average highest coupon rate is

materially larger in the four years after the financial crisis

(2008-2011) than the three

years previous to the financial crisis when interest rates were

generally higher. This lends

some support to the notion that TIF bond investors may have

24. viewed such securities

as relatively risky and thus demanded higher interest rates after

the Great Recession.

Many local governments sell their TIF debt as revenue bonds

with repayment solely

payable from the incremental tax revenues generated in the TIF

district (Johnson,

1999). However, some local governments sell TIF debt using a

general obligation bond

structure whereby repayment is ultimately backed by the full

faith and credit of the

general taxing body. Due to this more robust repayment pledge,

investors generally

view general obligation bonds as less risky than revenue bonds.

One might expect that

local governments would increase the sale o f TIF debt using a

general obligation bond

structure rather than a revenue bond structure in the years

during and after the Great

Recession. In Figure 10, we observe that immediately before the

Great Recession the

share o f general obligation TIF securities was between 2 and 5

percent, and the by early

2000s it was between 7 and 11 percent. Since the financial

crisis, however, the share of

general obligation TIFs increased to as high as 27 percent. It

appears that TIF issuers

are relying on their full faith and credit in more debt issues

after the recession than

on issues before the recession. We see statistically significant

changes in the number

o f general obligations TIFs in the market, with corresponding

Pearson’s Chi-squared

and log-likelihood Chi-squared statistics at 53.8 and 53.4. O f

course by pledging their

25. general obligation credit for TIFs, municipal issuers are

reducing their debt issuing

capacity for non-TIF issues.

The method by which local governments sell their bonds —

negotiated or competi-

tive — is an indicator o f whether local governments are using

financial intermediaries

to resolve information asymmetries. In a negotiated bond sale, a

local government

works directly with a pre-selected underwriter to pre-market

and market their bonds

tailoring the bond structure to market conditions and investor

demands. In a competi-

tive sale, local governments sell their bonds to an underwriter

or group o f underwriters

via an open auction with the lowest bidder receiving the bonds.

Among other things,

T a x I n c r e m e n t D e b t F in a n c e a n d t h e G r e a t

R e c e s s io n 689

previous research has shown that the additional certification

provided by underwriters

in a negotiated bond sale can be advantageous (i.e., it can lead

to lower interest costs

compared to competitive sales) when there is significant

volatility in the bond markets

(Leonard, 1994; Kriz, 2003; Peng and Brucato, 2003). The

financial crisis o f 2007-2008

created more volatility in the capital markets than in any other

period in decades. With

such volatility, all else equal, we might expect an upward spike

in negotiated sales of

26. TIF bonds. The TIF market was dominated by negotiated sales

even before the crisis,

but significantly more deals relied on negotiated sales since

then. As shown in Figure

11, since 2009 at least 87 percent o f TIF securities have been

sold in negotiated deals,

except for the anomalous year 2012 when California withdrew

from the TIF market.

This shift is statistically significant as the Pearson’s Chi-

squared and log-likelihood

Chi-squared statistics are equal to 53.9 and 52.9.

Figures 8 -1 1

Percentage of Total TIF Issuance Volume and Select TIF

Features,

39 US States and the District o f Columbia, 2000-2013 (c o n tin

u e d )

F ig u r e 8 A v e ra g e Y e a rs to C a ll

O CM ^ CD CO

O O O O O

O O O O O O O

CM CM CM CM CM CM CM

F ig u r e 9 A v e ra g e H ig h e s t C o u p o n

Y

e

a

rs

t

o

28. CM CM CM CM CM CM

0 F ig u r e 10 G e n e r a l O b lig a t io n T I F s

o

| 30

(/)

2 2 5

LL

H 20

CD

o 15

o 10

CD

O) d

CD O

O CM NT CD CO O CM

O O O O O

O O O O O O O

CM CM CM CM CM CM CM

I n i i . i m r

CD=3(/)0)

0

OH

M—

o

0

O)

CD

29. 0

Q_

F ig u r e 11 N e g o t ia t e d T IF s

O CM CD 00 O CM

O O O O O

O O O O O O O

CM CM CM CM CM CM CM

690 N ational Tax Journal

Prior research has also shown that the use o f financial advisors

on a municipal

security transaction can help deal with information

asymmetries. These financial

intermediaries help certify the true value o f the municipal

security and thus reduce the

borrowing costs of issuers (Johnson, 1994; Vijayakumar and

Daniels, 2006). Based on

this certification theory, we would expect the use o f financial

advisors on municipal

TIF securities to increase after the 2007-2008 financial crisis in

order to alleviate the

information asymmetries that increased at this time. Figure 12

shows the percent of

total TIF bonds that were sold without the use o f a financial

advisor. The share o f TIF

bonds issued without a financial advisor declined significantly

between 2007 and 2009

and stayed low throughout the entire post Great Recession

period, as compared to the

much higher shares observed in the pre-recession period. It

appears the local govern-

30. ments sought out this additional market certification more

frequently after 2007-2008

in light of the uncertainty created by the financial crisis. This

conclusion is supported

by highly significant Pearson’s Chi-squared and log-likelihood

Chi-squared statistics

of 78.6 and 84.2.

With more volatility in the capital markets and the collapse o f

credit enhancement

tools for TIF finance, better credit quality became important in

the post-recession years.

Figure 13 tracks the percentage o f TIF bond issues rated by at

least one o f the three

major credit rating agencies (Moody’s, Standard and Poor’s, or

Fitch) from 2000-2012.

Through their assignment o f credit ratings, these agencies are

financial intermediaries

that attempt to relieve the information asymmetries between the

issuer o f bonds and

investors especially with respect to the likelihood o f default.

Local governments seek

credit ratings to relieve these informational asymmetries as a

means o f reducing their

borrowing costs. Our results show that there was a general

upward trend in the extent

Figures 1 2 -1 3

Percentage o f Total TIF Issuance V olum e and Select TIF

Features,

39 US States and th e D istrict o f C olum bia, 2000-20 13

(continued)

00

§ 45

31. 1 40

LJL 35

H 30

3 25

t 20

° 15

2 10

m 5

Figure 12 TIFs without FA

0

Q_ O CM ^ CO CO O CMO O O O O t- t-

o o o o o o o

CM CM CM CM CM CM CM

Figure 13 TIFs without Rating

o CM CD 00 O CM

o O O O O

o O O O O O O

CM CM CM CM CM CM CM

Tax In c re m e n t D e b t F in a n c e a n d th e G re a t

Recession 691

to which local governments sought credit ratings on TIF bond

sales, which accelerated

after the financial crisis. In the years immediately before the

Great Recession, about

50 percent o f TIF transactions were rated. In the years

immediately after the Great

Recession, almost 75 percent o f TIF bond transactions received

32. credit ratings. This

upward trend is statistically supported by highly significant

Pearson’s Chi-squared

and log-likelihood Chi-squared statistics o f 62.2 and 59.0. This

is likely a combina-

tion o f local governments seeking additional certification o f

the value o f their TIF

bonds from a third party financial intermediary in the context of

the greater financial

uncertainty during these years and low credit quality issuers

staying out o f the market

altogether.

One o f the major calamities in the municipal market during the

Great Recession

was a collapse o f the bond insurance industry. O f the nine

active bond insurance firms

before the crisis, only two survived the crisis (Moldogaziev,

2013; Johnson, Luby,

and Moldogaziev, 2014). Prior to the financial crisis, almost 60

percent o f all new

long-term municipal securities were insured by monoline bond

insurers such as FSA,

AMBAC, and MBIA (Moldogaziev, 2013). As reported in

Tables 4A (2000-2007) and

4B (2008-2013), we find that there is a general increase in the

use o f insurance from

2000-2007 with 54 percent o f all TIF bonds insured in 2007.

However, there was dra-

matic decline in insured TIF bonds starting in 2008 (only 28

percent insured), which

continued through 2012. In 2013, the share o f insured TIFs

increased to 34 percent;

nevertheless, it is unlikely that bond insurance penetration in

the market will achieve

pre-crisis levels. Thus, while we would have expected to see an

33. increase in insured TIF

bonds after the Great Recession as a means of mitigating

investor concerns about bond

default, such credit enhancement is not as widely and cheaply

available in the capital

market as it used to be prior to the Great Recession. As the

relationship between the

frequency o f insured TIF securities and the year o f issuance

suggests (Tables 4A and

4B), there has been a statistically significant shift in the

distribution o f insured securi-

ties in the market; the Pearson’s Chi-squared and log-likelihood

Chi-squared statistics

are 317.9 and 381.0 respectively.

Another dramatic shift in the municipal market was the collapse

of the variable rate

bond market (Luby, 2012). State and local governments

generally have the ability to

sell their debt on a fixed interest rate basis where the interest

costs are set at issuance

or on a variable rate basis where interest rates fluctuate over the

term o f the issue. With

variable rate debt, state and local governments generally rely on

credit enhancement

devices such as bank letters o f credit and liquidity facilities to

successfully market the

bonds over the life o f the issue. Such credit enhancement

became very scarce during

and immediately after the financial crisis, which led to a

significant upward spike in

interest costs on these variable rate securities. This phenomenon

is shown in our data

in Tables 4 A and 4B. It is clear that the volume o f variable

rate TIF securities shrunk

dramatically after the Great Recession. More than 70 percent o f

34. all variable rate TIFs,

or $1.9 billion in our sample, were issued in 2000-2007. This

shift appears to be statisti-

cally significant, with Pearson’s Chi-squared and log-likelihood

Chi-squared statistics

of 27.7 and 33.4, respectively.

692 N ational Tax Journal

T a x I n c r e m e n t D e b t F in a n c e a n d t h e G r e a t

R e c e s s io n 693

694 N atio na l Tax Journal

As mentioned above, variable rate bonds and short-term

securities, in addition to

bond insurance, would also often be accompanied by letters o f

credit and/or liquidity

facilities. Though fluctuating before and after the Great

Recession, the volume o f TIFs

using these two forms o f credit enhancements fell after the

crisis. As shown in Tables

4A and 4B, the largest volume o f letter o f credit and/or

liquidity facility supported

securities was issued in 2005, but they have been largely under-

used in recent years. In

this case as well, the shift in letter of credit and/or liquidity

letter enhanced securities

is statistically significant. Our estimated Pearson’s Chi-squared

statistic is 25.4, while

35. the log-likelihood Chi-squared statistic is 25.6.

IV. D IS C U S S IO N

The Great Recession clearly affected TIF debt finance activity

by U.S. local govern-

ments. The volume and number o f TIF municipal securities

declined dramatically after

2007. This decline was seen across all states in both the number

o f annual transactions

and bond volume. Annual TIF bond issuance is now less than

half its size (as measured

by annual number o f transactions and volume) since its peak in

the mid to late 2000s. In

addition, the average transaction size o f TIF bond issues has

decreased since the Great

Recession. This decline in TIF debt activity is most likely the

result o f California, the

largest issuer o f TIF bonds, slowing down its issuance activity

after the recession and

ultimately exiting the market, but may also be a result o f other

issuers using less TIF

debt finance to fund their redevelopment projects given the

actual or projected decline

in growth o f property tax increments in many parts o f the

country.

It appears the type o f projects that TIF debt used to finance has

also changed since

the Great Recession. Economic development TIF projects rather

than general-purpose

TIF projects now constitute the great majority o f TIF debt

issued since the Great

Recession. In addition, the post-Great Recession period has

witnessed a total decline

in corporate-sponsored private-activity TIF bonds. Our findings

36. provide evidence that

bond investors may be demanding more specificity in their

investments. There is also

evidence o f a lack o f available private capital for government

development projects.

The TIF debt market experienced significant changes after the

Great Recession with

respect to the pricing, structure and sale process o f these

securities. Coupon interest rates

increased and call maturities declined, reflective o f a general

increase in the perceived

riskiness o f TIF securities. Local governments increased their

use o f general obligation

bond structures and independent financial advisors while more

often seeking credit rat-

ings on their TIF transactions as a way o f mitigating the

perceived increased riskiness

o f their municipal securities. Such actions to reduce

information asymmetries were

especially necessary as other risk mitigation tactics, such as

seeking third-party credit

enhancement, were not available to these local governments as

the monoline municipal

bond insurance market collapsed as a result o f the financial

crisis.

Given our findings regarding the impact o f the Great Recession

impact on TIF debt

finance, can we speculate how this financial market will look in

the future? Clearly,

local governments will continue to sell TIF securities as shown

by their continued issu-

37. T a x I n c r e m e n t D e b t F in a n c e a n d t h e G r e a t

R e c e s s io n 695

ance even during the recent global financial crisis. The market

is likely to be smaller

compared to its historical high since California local

governments will be prohibited

from selling TIF securities except for refinancing purposes. For

example, the year 2012

witnessed an even more dramatic drop than the years

immediately after the 2007-2008

financial crisis, as this was the first full year o f California’s

TIF debt prohibition. The

overall TIF municipal securities market may also be smaller if

the cost o f borrowing

using TIF debt finance stays higher than other modes o f

financing since such additional

interest costs will make redevelopment projects less feasible.

It is also likely that the structure and types o f projects financed

by TIF debt will

change. Local governments appeared to attempt to strengthen

the general credit char-

acteristics of their TIF securities after the financial crisis. Such

attempts will continue

and could take the form o f additional revenue pledges for bond

repayment other than

the tax increment, general obligation pledges for repayment in

addition to the increment,

greater use and size o f debt service reserve funds, and higher

debt service coverage

ratios (i.e., the minimum ratio o f expected tax increment

revenues to debt service).

Various market strategies related to financial intermediaries

may also flourish, includ-

ing the use o f financial advisors and more reputable

38. underwriters and the procurement

o f multiple credit ratings, to enhance the perceived credit o f

TIF debt. From the bond

investor perspective, local governments probably should expect

greater due diligence

of the credit characteristics o f their TIF securities, demand for

more “seasoned” TIF

districts, and greater scrutiny of feasibility analyses related to

the TIF district. All o f

these strategies and demands emanate from the desire o f the

investor community for

better and more carefully crafted TIF bond credits in an era o f

greater risk aversion

with respect to the general credit o f local governments.

V. CONCLUSION

Local governments have increasingly relied on the use o f debt

finance to raise

upfront redevelopment resources in their TIF districts. While

the Great Recession

certainly “changed the face” o f TIF debt finance, other factors

such as the collapse o f

the monoline bond insurance industry and the dissolution o f

TIF districts in California

contributed to the present state o f TIF debt finance. With local

governments in Cali-

fornia mostly exiting the TIF municipal securities market and

investors likely taking a

cautious view o f the issuers that remain in market, the future o

f TIF debt finance in the

United States is uncertain. However, as long as many local

government officials con-

tinue to believe that TIF is one o f their only economic

development tools, the financial

market should remain active, albeit taking on a significantly

39. different size and market

structure.

DISCLOSURES

The authors have no financial arrangements that might give rise

to conflicts of interest

with respect to the research reported in this paper.

696 National Tax Journal

REFERENCES

Boyd, Terry, 2013. “Insufficient Funds: Arena Debt Document

Reveals Struggle to Pay KFC

Yum! Center Bonds.” INSIDER Louisville, July 24,

http://insiderlouisville.com/news/arena-story/.

Briffault, Richard, 2010. “The Most Popular Tool: Tax

Increment Financing and the Political

Economy o f Local Government.” The University o f Chicago

Law Review 11 (1), 65-95.

Geheb, Philip J.F., 2009. “Tax Increment Financing Bonds as ‘D

ebt’ Under State Constitutional

Debt Limitations.” The Urban Lawyer 41 (4), 725-754.

Johnson, Craig L., 1994. “An Empirical Investigation o f the

Pricing o f Financial Advisor Ser-

vices.” Municipal Finance Journal 15 (3), 36-52.

Johnson, Craig L., 1999. “Tax Increment Debt Finance: An

Analysis o f the Mainstreaming o f a

Fringe Sector.” Public Budgeting & Finance 19(1), 47-67.

40. Johnson, Craig L, Martin J. Luby, and Tima M. Moldogaziev,

2014. State and Local Financial

Instruments: Policy Changes and Management. Edward Elgar

Publishing, Northampton, MA.

Kriz, Kenneth A., 2003. “Comparative Costs o f Negotiated

versus Competitive Bond Sales: New

Evidence from State General Obligation Bonds.” Quarterly

Review o f Economics and Finance

4 3 (2), 191-211.

Lefcoe, George, and Charles W. Swenson, 2014.

“Redevelopment in California: The Demise

o f TIF-Funded Redevelopment in California and Its

Aftermath.” National Tax Journal 67 (3),

719-744.

Leonard, Paul, 1994. “Negotiated Versus Competitive Bond

Sales: A Review o f the Literature.”

Municipal Finance Journal 15 (2), 12-36.

Luby, Martin J., 2012. “The Use o f Financial Derivatives in

State and Local Government Bond

Refinancings: Playing with Fire or Prudent Debt Management?”

Journal o f Public Budgeting,

Accounting & Financial Management 24 (1), 1-31.

Moldogaziev, Tima, 2013. “The Collapse o f the Municipal

Bond Insurance Market: How Did We

Get Here and Is There Life for the Monoline Industry beyond

the Great Recession?” Journal o f

Public Budgeting, Accounting, & Financial M a n a g e m e n ts

(1), 199-233.

Peng, Jun, and Peter Brucato, Jr., 2003. “Another Look at the

41. Effect o f Method o f Sale on the

Interest Costs in the Municipal Bond Market - A Certification

Model.” Public Budgeting &

Finance 23 (1), 73-95.

Vijayakumar, Jayaraman, and Kenneth N. Daniels, 2006. “The

Role and Impact o f Financial Advi-

sors in the Market for Municipal Bonds.” Journal o f Financial

Services Research 30 (1), 43-68.

Copyright of National Tax Journal is the property of National

Tax Association and its content

may not be copied or emailed to multiple sites or posted to a

listserv without the copyright

holder's express written permission. However, users may print,

download, or email articles for

individual use.