accounts.pptx

•Download as PPTX, PDF•

0 likes•4 views

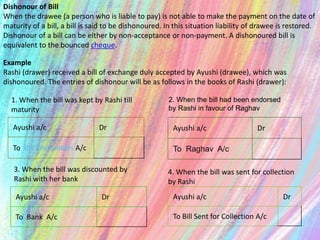

When a bill of exchange is not paid on the maturity date, it is considered dishonored. A dishonored bill results in the drawee's liability being restored and is equivalent to a bounced check. If a bill of exchange drawn by Rashi and accepted by Ayushi is dishonored, Rashi would make accounting entries debiting Ayushi's account and crediting various accounts depending on how the bill was held or transferred.

![Journal Entries in the books of Drawer

1. When the goods are Sold.

Debtor’s A/c……… Dr.

To Sales A/c

[the person who purchases the goods he is known as

debtor]

2. When the bill is drawn.

Bills Receivable A/c ……… Dr.

To Drawee’s A/c

3. Different ways of keeping Bill.

a. Kept with Drawer himself.

No entry

b. Discounted with the bank.

Cash / Bank A/c ……… Dr.

Discount A/c ………Dr.

To Bills Receivable A/c

c. Endorsed

Endorsee’s A/c ………Dr.

To Bills Receivable A/c

d. Sent to bank for collection.

Bank for collection A/c ………Dr.

To Bills Receivable A/c

4. When the Bill is Dishonoured.

a. Kept with Drawer himself.

Drawee’s a/c ……… Dr.

To Bills Receivable A/c

b. Discounted with the bank.

Drawee’s a/c ……… Dr.

To Cash / Bank A/c

c. Endorsed

Drawee’s a/c ……… Dr.

To Endorsee’s A/c

d. Sent to bank for collection.

Drawee’s a/c ……… Dr.

To Bank for collection A/c

5. When the Bill is Honoured.

a. Kept with Drawer himself.

Cash / Bank A/c ……… Dr.

To Bills receivable A/c

b. Discounted with the bank.

No entry

c. Endorsed

No entry

d. Sent to bank for collection.

Cash /Bank A/c ……… Dr.

To Bank for collection A/c

6. When the part payment is made

Cash / bank A/c ……… Dr.

To Drawee’s A/c

7. When the interest is charged.

Drawee’s A/c ……… Dr.

To Interest A/c

8. When the Bill is retired.

Cash / Bank A/c ……… Dr.

Rebate’s A/c ……… Dr

To Bill’s Receivable A/c

9. When the drawee become insolvent.

Cash / bank A/c ……… Dr.

Bad debts A/c ……… Dr.

To Drawee’s A/c

10. When the noting charge is charged.

The amount of noting charges will be added to the dishonoured

bill and no separate entry would be passed.](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

More Related Content

Similar to accounts.pptx

Similar to accounts.pptx (14)

More from Arun Gupta

More from Arun Gupta (20)

Recently uploaded

Recently uploaded (20)

accounts.pptx

- 1. Dishonour of Bill When the drawee (a person who is liable to pay) is not able to make the payment on the date of maturity of a bill, a bill is said to be dishonoured. In this situation liability of drawee is restored. Dishonour of a bill can be either by non-acceptance or non-payment. A dishonoured bill is equivalent to the bounced cheque. Example Rashi (drawer) received a bill of exchange duly accepted by Ayushi (drawee), which was dishonoured. The entries of dishonour will be as follows in the books of Rashi (drawer): Ayushi a/c Dr To Bill Receivables A/c Ayushi a/c Dr To Raghav A/c 2. When the bill had been endorsed by Rashi in favour of Raghav Ayushi a/c Dr To Bank A/c 1. When the bill was kept by Rashi till maturity Ayushi a/c Dr To Bill Sent for Collection A/c 3. When the bill was discounted by Rashi with her bank 4. When the bill was sent for collection by Rashi

- 2. Journal Entries in the books of Drawer 1. When the goods are Sold. Debtor’s A/c……… Dr. To Sales A/c [the person who purchases the goods he is known as debtor] 2. When the bill is drawn. Bills Receivable A/c ……… Dr. To Drawee’s A/c 3. Different ways of keeping Bill. a. Kept with Drawer himself. No entry b. Discounted with the bank. Cash / Bank A/c ……… Dr. Discount A/c ………Dr. To Bills Receivable A/c c. Endorsed Endorsee’s A/c ………Dr. To Bills Receivable A/c d. Sent to bank for collection. Bank for collection A/c ………Dr. To Bills Receivable A/c 4. When the Bill is Dishonoured. a. Kept with Drawer himself. Drawee’s a/c ……… Dr. To Bills Receivable A/c b. Discounted with the bank. Drawee’s a/c ……… Dr. To Cash / Bank A/c c. Endorsed Drawee’s a/c ……… Dr. To Endorsee’s A/c d. Sent to bank for collection. Drawee’s a/c ……… Dr. To Bank for collection A/c 5. When the Bill is Honoured. a. Kept with Drawer himself. Cash / Bank A/c ……… Dr. To Bills receivable A/c b. Discounted with the bank. No entry c. Endorsed No entry d. Sent to bank for collection. Cash /Bank A/c ……… Dr. To Bank for collection A/c 6. When the part payment is made Cash / bank A/c ……… Dr. To Drawee’s A/c 7. When the interest is charged. Drawee’s A/c ……… Dr. To Interest A/c 8. When the Bill is retired. Cash / Bank A/c ……… Dr. Rebate’s A/c ……… Dr To Bill’s Receivable A/c 9. When the drawee become insolvent. Cash / bank A/c ……… Dr. Bad debts A/c ……… Dr. To Drawee’s A/c 10. When the noting charge is charged. The amount of noting charges will be added to the dishonoured bill and no separate entry would be passed.

- 3. Journal Entries in the Books of Drawee 1. When the goods are purchased. Purchase A/c ……… Dr. To Creditor’s A/c [the person who sells the goods he is known as creditor] 2. When the bill is drawn. Drawer’s A/c ……… Dr. To Bills payable’s A/c 3. Different ways of keeping Bill. a. Kept with Drawer himself. No entry b. Discounted with the bank. No entry c. Endorsed No entry d. Sent to bank for collection. No entry 4. When the Bill is Dishonoured. a. Kept with Drawer himself. Bills payable a/c ……… Dr. To Drawer’s A/c b. Discounted with the bank. Bills payable a/c ……… Dr. To Drawer’s A/c c. Endorsed Bills payable a/c ……… Dr. To Drawer’s A/c d. Sent to bank for collection. Bills payable a/c ……… Dr. To Drawer’s A/c 5. When the Bill is Honoured. a. Kept with Drawer himself. Bills payable’s A/c ……… Dr. To Cash/ Bank A/c b. Discounted with the bank. Bills payable’s A/c ……… Dr. To Cash/ Bank A/c c. Endorsed Bills payable’s A/c ……… Dr. To Cash/ Bank A/c d. Sent to bank for collection. Bills payable’s A/c ……… Dr. To Cash/ Bank A/c 6. When the part payment is made Drawer’s A/c ……… Dr. To Cash/ Bank A/c 7. When the interest is charged. Interest A/c ……… Dr. To Drawer’s A/c 8. When the Bill is retired. Bills payable’s A/c ……… Dr. To Cash / Bank A/c To Discount A/c 9. When the drawee become insolvent. Drawer’s A/c ……… Dr. To Cash/ Bank A/c To Deficiency A/c 10. When the noting charge is charged. Noting charges a/c ……… Dr. To Drawer’s A/c

- 4. Bills of Exchange Example Let’s say that Mr. M has issued a bill of exchange for Mr. B who has purchased goods of $100,000 from Mr. M. The bill is issued on 05.10.2017. It is the same date when the goods are purchased on credit. But Mr. B didn’t accept the bill on the same date. Rather he accepted the bill on 10.10.2017. In this situation, we can see that Mr. M has issued a bill. Mr. M here is a creditor to Mr. B. Mr. B is a debtor who has purchased goods from Mr. M on credit. So when Mr. M has issued the bill, Mr. B didn’t accept it immediately. Mr. M has issued the bill on 05.10.2017 and Mr. B accepted it on 10.10.2017. During these 5 days till the 10th of October, 2017, we cannot call the bill issued by Mr. M as a bill of exchange. Rather we will only be able to call it a mere draft. But when Mr. B accepted the bill i.e. on 10.10.2017, that date onward we will call the bill, a bill of exchange.