Recommended

Recommended

More Related Content

Viewers also liked

Viewers also liked (9)

Similar to A comparison of three methods for selecting values of input variables in the analysis

Similar to A comparison of three methods for selecting values of input variables in the analysis (20)

More from Phuong Dx

More from Phuong Dx (20)

Recently uploaded

Recently uploaded (20)

A comparison of three methods for selecting values of input variables in the analysis

- 1. American Society for Quality A Comparison of Three Methods for Selecting Values of Input Variables in the Analysis of Output from a Computer Code Author(s): M. D. Mckay, R. J. Beckman, W. J. Conover Source: Technometrics, Vol. 42, No. 1, Special 40th Anniversary Issue (Feb., 2000), pp. 55-61 Published by: American Statistical Association and American Society for Quality Stable URL: http://www.jstor.org/stable/1271432 Accessed: 18/09/2010 22:32 Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at http://www.jstor.org/action/showPublisher?publisherCode=astata. Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact support@jstor.org. American Statistical Association and American Society for Quality are collaborating with JSTOR to digitize, preserve and extend access to Technometrics. http://www.jstor.org

- 2. A Comparison of Three Methods for Selecting Values of Input Variables in the Analysis of Output From a Computer Code M. D. MCKAYAND R. J. BECKMAN LosAlamosScientificLaboratory P.O.Box 1663 LosAlamos,NM87545 W. J. CONOVER Departmentof Mathematics TexasTechUniversity Lubbock,TX79409 Two types of sampling plans are examined as alternatives to simple random sampling in Monte Carlo studies. These plans areshown to be improvementsover simple randomsamplingwith respect to variancefor a class of estimators which includes the sample mean andthe empirical distribution function. KEY WORDS: Latin hypercubesampling;Sampling techniques;Simulation techniques;Variance reduction. 1. INTRODUCTION Numerical methods have been used for years to provide approximatesolutions to fluid flow problems that defy ana- lytical solutions because of their complexity. A mathemati- cal model is constructedto resemble the fluid flow problem, and a computer program (called a "code"), incorporating methods of obtaining a numerical solution, is written.Then for any selection of input variables X = (X,..., XK) an output variable Y = h(X) is produced by the computer code. If the code is accurate the output Y resembles what the actualoutputwould be if an experimentwere performed under the conditions X. It is often impractical or impossi- ble to perform such an experiment.Moreover,the computer codes are sometimes sufficiently complex so that a single set of input variables may require several hours of time on the fastest computers presently in existence in orderto pro- duce one output. We should mention that a single output Y is usually a graph Y(t) of output as a function of time, calculated at discrete time points t, to < t < tl. When modeling real world phenomena with a computer code one is often faced with the problem of what values to use for the inputs. This difficulty can arise from within the physical process itself when system parametersare not constant, but vary in some manner about nominal values. We model our uncertainty about the values of the inputs by treating them as random variables. The information de- sired from the code can be obtained from a study of the probability distribution of the output Y(t). Consequently, we model the "numerical"experiment by Y(t) as an un- known transformationh(X) of the inputs X, which have a known probability distribution F(x) for x c S. Obviously several values of X, say XI,..., XN, must be selected as successive inputs sets in order to obtain the desired infor- mation concerning Y(t). When N must be small because of the runningtime of the code, the input variables should be selected with great care. The next section describes three methods of selecting (sampling) input variables. Sections 3, 4 and 5 are devoted to comparing the three methods with respect to their per- formance in an actual computer code. The computer code used in this paper was developed in the Hydrodynamics Group of the Theoretical Division at the Los Alamos Scientific Laboratory, to study reac- tor safety (Hirt and Romero 1975). The computer code is named SOLA-PLOOP and is a one-dimensional version of anothercode SOLA (Hirt,Nichols, and Romero 1975). The code was used by us to model the blowdown depressuriza- tion of a straightpipe filled with water at fixed initial tem- perature and pressure. Input variables include: X1, phase change rate;X2, dragcoefficient for driftvelocity; X3, num- berof bubblesperunitvolume;andX4, pipe roughness.The inputvariablesareassumedto be uniformly distributedover given ranges. The output variable is pressure as a function of time, where the initial time to is the time the pipe rup- tures and depressurizationinitiates, and the final time tl is 20 milliseconds later.The pressure is recorded at 0.1 milli- second time intervals.The code was used repeatedly so that the accuracy and precision of the three sampling methods could be compared. 2. A DESCRIPTIONOF THE THREE METHODS USED FOR SELECTINGTHE VALUES OF INPUTVARIABLES From the many different methods of selecting the values of input variables, we have chosen three that have consid- erable intuitive appeal. These are called random sampling, stratifiedsampling, and Latin hypercube sampling. RandomSampling. Let the input values XI,..., XN be a random sample from F(x). This method of sampling is perhaps the most obvious, and an entire body of statistical literaturemay be used in making inferences regarding the distributionof Y(t). ? 1979 American Statistical Association and the American Society for Quality TECHNOMETRICS,FEBRUARY2000, VOL.42, NO. 1 55

- 3. M. D. MCKAY,R. J. BECKMAN,AND W. J. CONOVER StratifiedSampling. Using stratifiedsampling,all areas of the samplespaceof X arerepresentedby inputvalues. Let the samplespaceS of X be partitionedintoI disjoint strataSi. Let pi = P(X E Si) representthe size of Si. Obtain a random sample Xij, j = 1,..., ni from Si. Then of coursethe ni sum to N. If I = 1, we have random samplingoverthe entiresamplespace. LatinHypercubeSampling. The same reasoning thatled to stratifiedsampling,ensuringthatall portionsof S were sampled,couldleadfurther.If we wishto ensurealsothat each of the inputvariablesXk has all portionsof its dis- tributionrepresentedby inputvalues,we can divide the rangeof each Xk into N strataof equalmarginalproba- bility 1/N, and sampleonce from each stratum.Let this sample be Xkj, j = 1,..., N. These form the Xk compo- nent, k = 1,..., K, in Xi, i = 1,..., N. The components of the variousXk's are matchedat random.This method of selectinginputvaluesis anextensionof quotasampling (Steinberg1963),andcan be viewed as a K-dimensional extensionof Latinsquaresampling(Raj1968). One advantageof the Latinhypercubesampleappears when the output Y(t) is dominatedby only a few of the componentsof X. This methodensuresthateach of those componentsis representedin a fully stratifiedman- ner, no matterwhich componentsmight turn out to be important. WementionherethattheN intervalsontherangeof each componentof X combineto form NK cells whichcover the samplespaceof X. Thesecells, whicharelabeledby coordinatescorrespondingto the intervals,areused when findingthepropertiesof the samplingplan. 2.1 Estimators IntheAppendix(Section8),stratifiedsamplingandLatin hypercubesamplingareexaminedandcomparedtorandom samplingwithrespectto theclassof estimatorsof theform N T(Y1,..., YN) = (1/N) g(Yi), i=l whereg(.) = arbitraryfunction. If g(Y) = Y thenT representsthe samplemeanwhichis used to estimate E(Y). If g(Y) = yr we obtain the rth sample moment. By letting g(Y) = 1 for Y < y, 0 other- wise, we obtaintheusualempiricaldistributionfunctionat thepointy. Ourinterestis centeredaroundtheseparticular statistics. Let T denotetheexpectedvalueof T whentheYt'scon- stitutearandomsamplefromthedistributionof Y = h(X). We show in the Appendixthat both stratifiedsampling and Latinhypercubesamplingyield unbiasedestimators of r. If TR is theestimateof T froma randomsampleof size N, andTs is the estimatefroma stratifiedsampleof size N, thenVar(Ts)< Var(TR)whenthe stratifiedplanuses equalprobabilitystratawith one sampleper stratum(all pi = 1/N and nij = 1). No direct means of comparing the varianceof the correspondingestimatorfromLatinhyper- cube sampling,TL,to Var(Ts)has been found.However, TECHNOMETRICS,FEBRUARY2000, VOL.42, NO. 1 thefollowingtheorem,provedin theAppendix,relatesthe variances of TL and TR. Theorem. If Y = h(X1,... XK) is monotonic in each of its arguments,andg(Y) is a monotonicfunctionof Y, then Var(TL)< Var(TR). 2.2 The SOLA-PLOOP Example The three samplingplans were comparedusing the SOLA-PLOOPcomputercodewithN = 16.Firstarandom sampleconsistingof 16 valuesof X = (X1,X2,X3,X4) wasselected,enteredasinputs,and16graphsof Y(t) were observedas outputs.Theseoutputvalueswereusedin the estimators. Forthe stratifiedsamplingmethodtherangeof eachin- put variablewas dividedat the medianinto two partsof equalprobability.Thecombinationsof rangesthusformed produced24 = 16 strataSi. Oneobservationwas obtained atrandomfromeachSi as input,andtheresultingoutputs wereusedto obtaintheestimates. ToobtaintheLatinhypercubesampletherangeof each inputvariableXi was stratifiedinto 16 intervalsof equal probability,andoneobservationwasdrawnatrandomfrom eachinterval.These16valuesforthe4 inputvariableswere matchedatrandomto form 16 inputs,andthus 16 outputs fromthecode. The entireprocessof samplingand estimatingfor the threeselectionmethodswas repeated50 timesin orderto getsomeideaof theaccuraciesandprecisionsinvolved.The total computertime spentin runningthe SOLA-PLOOP code in this studywas 7 hourson a CDC-6600.Some of the standarddeviationplotsappearto be inconsistentwith the theoreticalresults.These occasionaldiscrepanciesare believedto arisefromthenon-independenceof theestima- torsovertimeandthe smallsamplesizes. 3. ESTIMATINGTHE MEAN Thegoodnessof an unbiasedestimatorof the meancan be measuredby the size of its variance.Foreachsampling method,theestimatorof E(Y(t)) is of theform N Y(t) = (l/N) E Yi(t) i=l (3.1) where i=1,...,N. In the case of the stratifiedsample,the Xi comesfrom stratumSi, pi = 1/N and ni = 1. For the Latin hypercube sample,theXi is obtainedin themannerdescribedearlier. Each of the three estimators YR,Ys, and YLis an unbiased estimatorof E(Y(t)). The variancesof the estimatorsare givenin (3.2): Var(Y(t)) = (1/N)Var(Y(t)) N Var(Ys(t)) = Var(YR(t))- (1/N2) (pi - ,)2 i=l 56 Yi(t) = h(X),

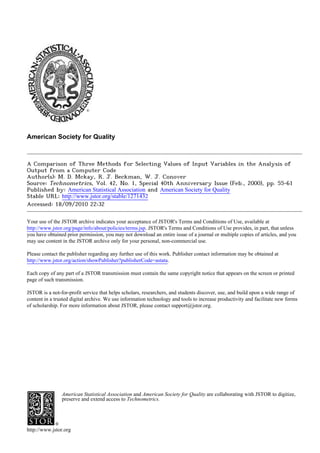

- 4. A COMPARISONOF THREE METHODS FOR SELECTINGVALUESOF INPUT 150-0 ANDOM ............ STRATI ......... LAT -- I I 0 2 I- (nV) La. z < LLJ 2~E RANDOM STRATIFIED LATIN100-0 50-0 0-0 5-0 1I0 TIME 1-02015.0 20-0 Figure 1. Estimating the Mean: The Sample Mean of YR(t), Ys(t), and YL(t). Var(YL(t))= Var(YR(t))+ ((N - 1)/N) 1/(NK(N- I)K)) E (i R - )(tj - t) (3.2) TIME Figure 3. Estimating the Variance:The Sample Mean of S2 (t), S (t), and S2 (t). YL(t) clearly demonstrates superiority as an estimator in this example, with a standarddeviationroughly one-fo[u]rth that of the random sampling estimator. where p = E(Y(t)), pi = E(Y(t)lX E Si) in the stratified sample, or Pi - E(Y(t)lX e cell i) in the Latin hypercube sample, and R means the restricted space of all pairs ,ui,/j having no cell coordinates in common. For the SOLA-PLOOP computer code the means and standarddeviations, based on 50 observations, were com- puted for the estimators just described. Comparative plots of the means are given in Figure 1. All of the plots of the means are comparable, demonstrating the unbiasedness of the estimators. Comparativeplots of the standarddeviations of the es- timators are given in Figure 2. The standarddeviation of Ys(t) is smaller than that of YR(t) as expected. However, or O0 I- 2 I- (C) Lj La. 0 0 4. ESTIMATINGTHE VARIANCE For each sampling method, the form of the estimator of the variance is N S2(t) - (1/N)Y (Y(t)- Y(t))2, i=l and its expectation is E(S2(t)) Var(Y(t)) - Var(Y(t)), (4.1) (4.2) where Y(t) is one of YR(t),Ys(t), or YL(t). In the case of the random sample, it is well known that NS2/(N- 1) is an unbiased estimator of the variance of Y(t). The bias in the case of the stratified sample is un- known. However, because Var(Ys(t)) < Var(YR(t)), (1- 1/N)Var(Y(t)) < E(S2(t)) < Var(Y(t)). (4.3) 50'0 - 2-5 - 20 - 1-5 - 1.0 - 0-5 - RANDOM . STRATFIED ---------- LATIN : '' :, i .@: ,;i/ . S ., :t '~.....~- -"-- '--t-- -~....._.._ ....~` I: I- V) LA- 0 O c5 u' 40-0 - 30-0 - 20-0 - 10-0 - RANDOM STRATIFIED LATIN i'' ii I 1' 1 :, 1 1 ' 1 ' 1 't ?f? I I "r, 5-0 10-0 TIME 15-15.0 20-0 0.0 5.0 10-0 TIME 15-0 2015.0 20.0 Figure 2. Estimating the Mean: The Standard Deviation of YR(t), Ys(t), and YL(t). Figure 4. Estimating the Variance: The Standard Deviation of S2(t), Ss(t), and S2(t). TECHNOMETRICS,FEBRUARY2000, VOL.42, NO. 1 140-0 - CY O0 I- 2 V) LJ6 LA. 0 zLLJ w 120-0- 100*0- 80.0 - 60-0 - 0'0 0.0 Ai"-(n A -.I.v -V n.n ' a -1. I-,., ..- /-a 57

- 5. M. D. MCKAY,R. J. BECKMAN,AND W. J. CONOVER o- RANDOM STRATIFID .......- I LATIN -- / / Il/ // "_' ......./"" 20-0 30-0 40-0 50-0 60-0 70-0 PRESSURE 2.1, theexpectedvalueof G(y,t) underthethreesampling plansis thesame,andunderrandomsampling,theexpected value of G(y, t) is D(y, t). The variancesof the threeestimatorsaregivenin (5.2). Di againrefersto eitherstratumi orcell i, as appropriate, andR representsthesamerestrictedspaceasit didin (3.2). Var(GR(y,t)) = (1/N)D(y, t)(l - D(y, t)) Var(Gs(y, t)) = Var(GR(y,t)) N - (1/N2) (D (y, t)- D(y, t))2 t=l I80 980.0 90'0 Figure 5. Estimating the CDF: The Sample Mean of GR(Y,t), Gs(y, t), and GL(y, t) at t = 1.4. Thebiasin the Latinhypercubeplanis also unknown,but for the SOLA-PLOOPexampleit wassmall.Variancesfor theseestimatorswerenotfound. AgainusingtheSOLA-PLOOPexample,meansandstan- darddeviations(basedon 50 observations)werecomputed. The meanplots are given in Figure3. They indicatethat all threeestimatorsare in relativeagreementconcerning thequantitiestheyareestimating.Intermsof standardde- viationsof the estimators,Figure4 shows that,although stratifiedsamplingyieldsaboutthe sameprecisionas does randomsampling,Latinhypercubefurnishesa clearlybet- terestimator. 5. ESTIMATINGTHE DISTRIBUTIONFUNCTION The distribution function, D(y,t), of Y(t) = h(X) may beestimatedbytheempiricaldistributionfunction.Theem- piricaldistributionfunctioncanbe writtenas N G(y, t) = (1/N) u(y- Yi(t)), (5.1) i=-i whereu(z) = 1 for z > 0 and is zero otherwise.Since equation(5.1) is of the formof the estimatorsin Section 015 - ~~~~~~~RANDOMWY~~~~~~ . 0o .T5RA D .......... ---- < o0-0- LAW -- / I- : vG:y,-, tatt=4(:,a _ .....* : :- ^ ^ *../:- Eo , . .: . 0. 2'' 0-00 /J * I I I I 20'0 30-0 4O?0 5-0s 0'0 700 0-o0 90-0 PRESSURE Figure 6. Estimating the CDF: The Standard Deviation of GR(y, t), Gs(y, t), and GL(y, t) at t = 1.4. Var(GL(y,t)) = Var(GR(y,t)) + ((N - 1)/N. 1/NK(N - 1)K) E (Di(y,t) R - D(y, t)). (Dj(y, t) - D(y, t)). (5.2) As with the cases of the meanandvarianceestimators, thedistributionfunctionestimatorswerecomparedfor the threesamplingplans.Figures5 and6 give the meansand standarddeviationsof the estimatorsat t = 1.4 ms. This time pointwas chosento correspondto the time of max- imumvariancein the distributionof Y(t). Againthe esti- matesobtainedfroma Latinhypercubesampleappearto be moreprecisein generalthanthe othertwo typesof es- timates. 6. DISCUSSION AND CONCLUSIONS We havepresentedthreesamplingplansandassociated estimatorsof themean,thevariance,andthepopulationdis- tributionfunctionof the outputof a computercode when theinputsaretreatedasrandomvariables.Thefirstmethod is simplerandomsampling.The secondmethodinvolves stratifiedsamplingandimprovesuponthefirstmethod.The thirdmethodis calledhereLatinhypercubesampling.It is an extensionof quotasampling(Steinberg1963),andit is a firstcousinto the "randombalance"designdiscussedby Satterthwaite(1959),Budne(1959),Youdenet al. (1959), Anscombe(1959),andto thehighlyfractionalizedfactorial designs discussedby Enrenfeldand Zacks (1951, 1967), Dempster(1960, 1961), and Zacks (1963, 1964), and to latticesamplingas discussedby Jessen(1975).This third methodimprovesuponsimplerandomsamplingwhencer- tain monotonicityconditionshold, andit appearsto be a goodmethodto use for selectingvaluesof inputvariables. 7. ACKNOWLEDGMENTS WeextendaspecialthankstoRonaldK.Lohrding,forhis earlysuggestionsrelatedtothisworkandforhiscontinuing supportandencouragement.We also thankourcolleagues LarryBruckner,BenDuran,C.Phive,andTomBoullionfor theirdiscussionsconcerningvariousaspectsof theproblem, andDaveWhitemanfor assistancewiththecomputer. Thispaperwaspreparedunderthe supportof the Anal- ysis DevelopmentBranch,Divisionof ReactorSafetyRe- search,NuclearRegulatoryCommission. 1.0 - 0.8 - 0*6- 0-4 - 0-2 - cr 0 I-4 V) 2 L&J La. 0 z LLJ :2 0'0 TECHNOMETRICS,FEBRUARY2000, VOL.42, NO. 1 lm . . .. k- 58

- 6. A COMPARISONOF THREE METHODSFOR SELECTINGVALUESOF INPUT 8. APPENDIX In the sectionsthatfollow we presentsome generalre- sults aboutstratifiedsamplingand Latinhypercubesam- pling in orderto make comparisonswith simplerandom sampling.Wemovefromthegeneralcaseof stratifiedsam- pling to stratifiedsamplingwith proportionalallocation, andthen to proportionalallocationswith one observation perstratum.WeexamineLatinhypercubesamplingforthe equalmarginalprobabilitystratacase only. 8.1 TypeIEstimators LetX denotea K variaterandomvariablewithprobabil- ity densityfunction(pdf) f(x) for x E S. Let Y denotea univariatetransformationof X givenby Y = h(X). Inthe contextof thispaperwe assume X f(x),xeS KNOWNpdf Y = h(X) UNKNOWNbutobservable transformationof X. The class of estimatorsto be consideredare those of the form N T(Ul,..., iUN)=-(l/N) Eg (ui), (8.1) t=l where g(.) is an arbitrary,knownfunction.In particular we use g(u) = ur to estimatemoments,andg(u) = 1 for u > 0,= 0 elsewhere,to estimatethedistributionfunction. The samplingschemesdescribedin the following sec- tions will be comparedto randomsamplingwith respect to T. The symbolTR denotesT(Y1,..., YN)whenthe ar- gumentsY, ..., YNconstitutea randomsampleof Y. The meanandvarianceof TRaredenotedby r and02/N. The statisticT given by (8.1) will be evaluatedat arguments arisingfrom stratifiedsamplingto form Ts, andat argu- mentsarisingfromLatinhypercubesamplingto formTL. The associatedmeansand varianceswill be comparedto thosefor randomsampling. 8.2 StratifiedSampling Lettherangespace,S, of X bepartitionedintoI disjoint subsetsSi of size pi = P(X c Si), with I 5Pi 1. i=l Let Xij,j = 1,., ni, be a randomsamplefrom stratum Si. Thatis, let Xij iid f(x)/pi,j = 1,..., ni, forx ESi, butwithzerodensityelsewhere.Thecorrespondingvalues of Y aredenotedby Yij= h(Xij), andthestratameansand variancesof g(Y) aredenotedby i = E(g(Yij))- j g(y)(l/pi)f(x) dx Si a-2 - Var(g(Yj)) = S (g(y) - )2(1/pi)f(x)dx.i I s Itis easyto seethatif weusethegeneralform I ni Ts = (pi/ni) E g(Yij), i=l j=l thatTs is an unbiasedestimatorof r with variancegiven by (8.2)Var(Ts) = (p2/ni)o2. i=l Thefollowingresultscanbe foundin Tocher(1963). StratifiedSampling with Proportional Allocation. If the probabilitysizes, pi, of the strataand the samplesizes, ni, are chosen so that ni = piN, proportional allocation is achieved.Inthiscase (8.2)becomes I Var(Ts) = Var(TR)- (I/N) EPi(iii - r)2. i=l (8.3) Thus,we see thatstratifiedsamplingwithproportionalal- locationoffersanimprovementoverrandomsampling,and thatthe variancereductionis a functionof the differences betweenthe stratameans,i andtheoverallmeanr. Proportional Allocation with One Sample per Stratum. Any stratifiedplan which employssubsampling,ni > 1, canbe improvedby furtherstratification.Whenall ni = 1, (8.3)becomes N Var(Ts) = Var(TR) - (1/N2) E (i - r)2. i=l (8.4) 8.3 LatinHypercube Sampling In stratifiedsamplingthe range space S of X can be arbitrarilypartitionedto form strata.In Latinhypercube samplingthepartitionsareconstructedina specificmanner usingpartitionsof therangesof eachcomponentof X. We will onlyconsiderthecasewherethecomponentsof X are independent. Let the rangesof each of the K componentsof X be partitionedinto N intervalsof probabilitysize 1/N. The Cartesianproductof these intervalspartitionsS into NK cellseachof probabilitysizeN-K. Eachcellcanbelabeled by a set of K cell coordinates mi = (mil, i2,..., iK) wheremij is the intervalnumberof componentXj repre- sentedin cell i. A Latinhypercubesampleof size N is ob- tained from a randomselection N of the cells ml,..., mN, withtheconditionthatforeachj theset {mij}N is a per- mutationof theintegers1,..., N. Onerandomobservation is madein eachcell. Thedensityfunctionof X givenX c cell i is NKf(x) if x E cell i, zero otherwise. The marginal (unconditional)distributionof Yi(t)is easilyseento be the sameas thatfor a randomlydrawnX as follows: P(Y < y) = P(Yi < ylX E cell q)P(X c cell q) all cells q = E ll N K(x)dx(1/NK) h(x)<y -Jh(x)<y f(x) dx. TECHNOMETRICS,FEBRUARY2000, VOL.42, NO. 1 59

- 7. M. D. MCKAY,R. J. BECKMAN,AND W.J. CONOVER From this we have TL as an unbiased estimator of T. To arrive at a form for the variance of TL we introduce indicator variables wt, with f 1 if cell i is in the sample Wi- l 0 if not. The estimator can now be written as NK TL = (1/N) z wig(Yi), i=l1 (8.5) where Yi = h(Xi) and Xi c cell i. The variance of TL is given by NK Var(TL)= (1/N2) Var(wig(Yi)) i=l NK NK + (1/N2) 5 Cov(wig(Yi), Wjg(Yj)). (8.6) i=l j=l jii The following results about the wi are immediate: 1. P (wi = 1) = (1/NK-1) = E(wi) = E(w2) Var(wi) (1/NK-1)(1- 1INK-1). 2. If wi and wj correspond to cells having no cell coor- dinates in common, then E(wiwj) = E(wiw lwwj= O)P(wj = 0) + E(wiwjlwj = 1)P(wj = 1) = 1/(N(N- 1))K-1 3. If wi and wj correspond to cells having at least one common cell coordinate, then E(iwjw) =0. Now Var(wig(Yi)) = E(w2)Var g(Yi) + E2(g(Yi))Var(wt) (8.7) so that NK E Var(wig(Yi)) i=l NK N-K+l E E(g(Yi) i=l i)2 NK + (N-K+I1 N-2K+2) E 2 (8.8) ='-1 where ui = E{g(Y))X e cell i}. Since E(g(Y)- i)2 -- NK (g(y) - 7)2f(x) dx + (i - wcelli we have 5 Var(wig(Yi)) i N Var(Y)- N-K+1 E (i i + (N-K+1 _ N-2K+2) E Furthermore NK NK E Z Cov(wig(Yi),wjg(Yj)) i=1 j=1 i#j - EZ E ijE{wiwj} - N-2K+2 ZE ipj (8.11) i#j i?j which combines with (8.10) to give Var(TL) = (1/N)Var(Y) - N-K-1 (t _ )2 i + (N-K-1 N-2NK)- 2 + (N - 1)-K+1NK-1 R -N -2K E ij-^ EE^.~~., (8.12) where R means the restricted space of NK(N - 1)K pairs ([i, ,j) correspondingto cells having no cell coordinates in common. After some algebra, and with K ui = NKT, the final form for Var(TL)becomes Var(TL) = Var(TR) + (N - 1)/N[N-K(N - 1)-K *E (pi- T)(pu- T)]. (8.13) R Note that Var(TL)< Var(TR)if and only if N -K(N - 1)-K (/i - )(1jt - T) < 0, (8.14) R which is equivalent to saying that the covariance between cells having no cell coordinates in common is negative. A sufficient condition for (8.14) to hold is given by the fol- lowing theorem. Theorem. If Y = h(X1,..., XK) is monotonic in each of its arguments,and if g(Y) is a monotonic function of Y, then Var(TL)< Var(TR). Proof The proof employs a theorem by Lehmann (1966). Two functions r(x1,..., XK) and s(y1,..., YK) are said to be concordant in each argument if r and s either increase or decrease together as a function of xi - yi, with all xj,j 7 i and yj,j - i held fixed, for each i. Also, )2 (8.9) a pair of random variables (X, Y) are said to be nega- tively quadrant dependent if P(X < x, Y < y) < P(X < x)P(Y < y) for all x,y. Lehmann's theorem states that _ T)2 if (i) (X1, Y1),(X2, Y2),... (XK, YK) are independent, (ii) (Xi, Y,) is negatively quadrantdependent for all i, and (iii) X = r(X1,...,XK) and Y = s(Y1,...,YK) are concor- 2. (8.10) dant in each argument,then (X, Y) is negatively quadrant dependent. TECHNOMETRICS,FEBRUARY2000, VOL.42, NO. 1 60

- 8. A COMPARISONOF THREE METHODSFOR SELECTINGVALUESOF INPUT We earlierdescribeda stage-wiseprocessfor selecting cellsforaLatinhypercubesample,whereacell waslabeled by cell coordinates mi,..., miK. Two cells (I1,..., IK) and (ml,..., mK) with no coordinates in common may be se- lectedas follows.Randomlyselecttwo integers(R11,R21) withoutreplacementfromthefirstN integers1,..., N. Let 11 = R11 and m1 = R21. Repeat the procedure to obtain (R12,R22), (R13,R23), . .,(R1K, R2K) and let lk = RIk and mk = R2k. Thus two cells are randomly selected and lk 7 mk for k = 1,..., K. Note thatthe pairs (Rlk, R2k), k = 1,..., K, aremutually independent. Also note that because P(Rlk < x, R2k < y) = [xy - min(x,y)]/(n(n - 1)) < P(Rlk < x)P(R2k < y), where[.] representsthe"greatestinteger"function,each pair (Rlk, R2k) is negatively quadrantdependent. Let /ul be the expectedvalue of g(Y) withinthe cell designated by (I1,..., 1K), and let /2 be similarly defined for (ml,... ,mK). Then /1 = ii(R11,R12,... ,R1K) and A12 -= I(R21, R22, ..., R2K) are concordant in each argu- ment underthe assumptionsof the theorem.Lehmann's theorem then yields that 1iand /2 are negatively quadrant dependent.Therefore, P(PI1< X, l2 < y) < P(li1 < x)P(i2 < y). UsingHoeffding'sequation Cov(X, Y) = 1+oo r+00 [P(X < x, Y < y) - P(X < x)P(Y < y)] dx dy, (seeLehmann(1966)foraproof),wehaveCov(/Al,/2) < 0. Since Var(TL) = Var(TR)+ (N - 1)/N Cov(i,Lu2), the theoremis proved. Sinceg(t) asusedin bothSections3 and5 is anincreas- ing functionof t, we cansay thatif Y = h(X) is a mono- tonic functionof each of its arguments,Latinhypercube samplingis betterthanrandomsamplingforestimatingthe meanandthepopulationdistributionfunction. [Received January 1977. Revised May 1978.] REFERENCES Anscombe,F. J. (1959),"QuickAnalysisMethodsfor RandomBalance ScreeningExperiments,"Technometrics,1, 195-209. Budne,T.A. (1959),"TheApplicationof RandomBalanceDesigns,Tech- nometrics, 1, 139-155. Dempster,A.P.(1960),"RandomAllocationDesignsI:OnGeneralClasses of EstimationMethods,"TheAnnals of MathematicalStatistics, 31, 885- 905. (1961),"RandomAllocationDesignsII:ApproximateTheoryfor Simple Random Allocation," TheAnnals of Mathematical Statistics, 32, 387-405. Ehrenfeld,S., andZacks,S. (1951),"RandomizationandFactorialExper- iments,"TheAnnals of Mathematical Statistics, 32, 270-297. (1967), "TestingHypothesesin RandomizedFactorialExperi- ments,"TheAnnals of Mathematical Statistics, 38, 1494-1507. Hirt,C.W.,Nichols,B.D.,andRomero,N.C.(1975),"SOLA-A Numeri- calSolutionAlgorithmforTransientFluidFlows,"ScientificLaboratory ReportLA-5852,LosAlamosNationalLaboratory,NM. Hirt,C.W.,andRomero,N. C.(1975),"Applicationof aDrift-FluxModel to Flashingin StraightPipes,"ScientificLaboratoryReportLA-6005- MS,LosAlamosNationalLaboratory,NM. Jessen,RaymondJ.(1975),"SquareandCubicLatticeSampling,"Biomet- rics,31,449-471. Lehmann,E. L. (1966),"SomeConceptsof Dependence,"TheAnnalsof Mathematical Statistics, 35, 1137-1153. Raj,Des. (1968),SamplingTheory,New York:McGraw-Hill. Satterthwaite,F.E. (1959),"RandomBalanceExperimentation,"Techno- metrics, 1, 111-137. Steinberg,H. A. (1963),"GeneralizedQuotaSampling,"NuclearScience and Engineering, 15, 142-145. Tocher,K.D. (1963),TheArtofSimulation,Princeton,NJ:VanNostrand. Youden,W.J., Kempthorne,O.,Tukey,J. W.,Box, G. E. P.,andHunter, J. S. (1959), Discussionof the papersof Messrs.Satterthwaiteand Budne, Technometrics,1, 157-193. Zacks,S. (1963),"Ona CompleteClassof LinearUnbiasedEstimators for RandomizedFactorialExperiments,"TheAnnalsof Mathematical Statistics, 34, 769-779. (1964), "GeneralizedLeastSquaresEstimatorsfor Randomized FractionalReplication Designs," TheAnnals of Mathematical Statistics, 35, 696-704. TECHNOMETRICS,FEBRUARY2000, VOL.42, NO. 1 61