Market multiple table 11.8.2021 - Kurt Altrichter

•

0 likes•2 views

Market multiple table 11.8.2021 - Kurt Altrichter

Recommended

More Related Content

Similar to Market multiple table 11.8.2021 - Kurt Altrichter

Similar to Market multiple table 11.8.2021 - Kurt Altrichter (20)

More from Kurt S. Altrichter

More from Kurt S. Altrichter (20)

Recently uploaded

Recently uploaded (20)

Market multiple table 11.8.2021 - Kurt Altrichter

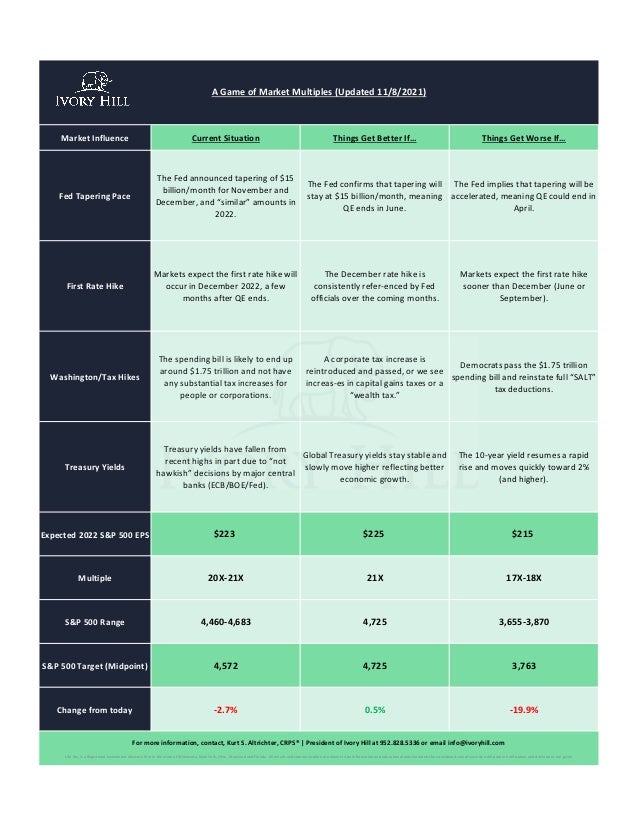

- 1. Market Influence Current Situation Things Get Better If… Things Get Worse If… Fed Tapering Pace The Fed announced tapering of $15 billion/month for November and December, and “similar” amounts in 2022. The Fed confirms that tapering will stay at $15 billion/month, meaning QE ends in June. The Fed implies that tapering will be accelerated, meaning QE could end in April. First Rate Hike Markets expect the first rate hike will occur in December 2022, a few months after QE ends. The December rate hike is consistently refer-enced by Fed officials over the coming months. Markets expect the first rate hike sooner than December (June or September). Washington/Tax Hikes The spending bill is likely to end up around $1.75 trillion and not have any substantial tax increases for people or corporations. A corporate tax increase is reintroduced and passed, or we see increas-es in capital gains taxes or a “wealth tax.” Democrats pass the $1.75 trillion spending bill and reinstate full “SALT” tax deductions. Treasury Yields Treasury yields have fallen from recent highs in part due to “not hawkish” decisions by major central banks (ECB/BOE/Fed). Global Treasury yields stay stable and slowly move higher reflecting better economic growth. The 10-year yield resumes a rapid rise and moves quickly toward 2% (and higher). Expected 2022 S&P 500 EPS $223 $225 $215 Multiple 20X-21X 21X 17X-18X S&P 500 Range 4,460-4,683 4,725 3,655-3,870 S&P 500 Target (Midpoint) 4,572 4,725 3,763 Change from today -2.7% 0.5% -19.9% A Game of Market Multiples (Updated 11/8/2021) For more information, contact, Kurt S. Altrichter, CRPS® | President of Ivory Hill at 952.828.5336 or email info@ivoryhill.com Life Inc, is a Registered Investment Advisory firm in the state of Minnesota, New York, Ohio, Maryland and Florida. All emails and communication are meant to be information and educational and should not be considered sale of security until proper notification and disclosures are given