Series A OnlyVC Method Practice Problem

Solution

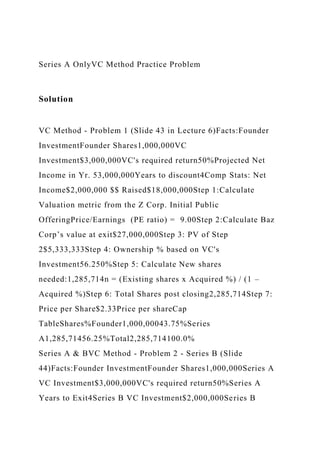

VC Method - Problem 1 (Slide 43 in Lecture 6)Facts:Founder InvestmentFounder Shares1,000,000VC Investment$3,000,000VC's required return50%Projected Net Income in Yr. 53,000,000Years to discount4Comp Stats: Net Income$2,000,000 $$ Raised$18,000,000Step 1:Calculate Valuation metric from the Z Corp. Initial Public OfferingPrice/Earnings (PE ratio) = 9.00Step 2:Calculate Baz Corp’s value at exit$27,000,000Step 3: PV of Step 2$5,333,333Step 4: Ownership % based on VC's Investment56.250%Step 5: Calculate New shares needed:1,285,714n = (Existing shares x Acquired %) / (1 – Acquired %)Step 6: Total Shares post closing2,285,714Step 7: Price per Share$2.33Price per shareCap TableShares%Founder1,000,00043.75%Series A1,285,71456.25%Total2,285,714100.0%

Series A & BVC Method - Problem 2 - Series B (Slide 44)Facts:Founder InvestmentFounder Shares1,000,000Series A VC Investment$3,000,000VC's required return50%Series A Years to Exit4Series B VC Investment$2,000,000Series B Required Return25%Series B Years to Exit2Projected Net Income in Yr. 53,000,000Comp Stats: Net Income$2,000,000 $$ Raised$18,000,000Step 1:Calculate the required Future Value of Series B VC’s investment using the 25% required rate of return: 2,000,000 x (1.25)2 3,125,000.00Step 2: Calculate Series B Required Ownership % Series B FV / Exit Valuaion from Problem 111.5741%0.562567.8241%Step 3: Calculate Required Shares to be issued to Series A VC to ensure that it owns 56.25% at exit n = (Existing shares x Acquired %) / (1 – Acquired %)2,107,914Step 4: Total Shares3,107,914Step 5: Series A Required Ownership % based on VC's Investment67.824%Step 6: Price per Share$1.42Cap TableShares%Founder1,000,00032.2%Series A2,107,91467.8%Total3,107,914100.0%

Name ;

- SECOND EXAM SPRING 2020

1. Mark Price the marketing manager for Speakers needs to find which variable most affects the demand for a line of speakers. He is uncertain whether the price of speakers of the advertising expenditures drive the sale of speakers. He plans to use the regression analysis to determine the relative impact price an advertising. He used 12 years of data which is given below. The output from his regression analysis also give:

Sales

(000)

Price Per Unit

Advertising

($000)

400

280

600

700

215

835

900

211

1100

1300

210

1400

1150

215

1200

1200

200

1300

900

225

900

1100

207

1100

980

220

700

1234

211

900

925

227

700

800

245

690

Regression Statistics

Multiple R

0.8550

R Square

0.7310

Adjusted R Square

0.6712

Standard Error

146.6234

Observations

12

ANOVA

df

SS

MS

F

Significance F

Regression

2

525718.3339

262859.1669

12.2269

0.0027

Residual

9

193485.9161

21498.4351

Total

11

719204.2500

Coefficients

Standard Error

t Stat

P-value

Lower 95%

Intercept

2191.34

826.08

2.65

0.03

322.61

Price

-6.91

2.92

-2.37

0.04

-13.51

Advertising

0.33

0.24

1.36

0.21

-0.21

a. Interpret the output from the regression analysis given above.

Measures of Central Tendency: Mean, Median and Mode

Series A OnlyVC Method Practice Problem SolutionVC Method - Proble.docx

1. Series A OnlyVC Method Practice Problem

Solution

VC Method - Problem 1 (Slide 43 in Lecture 6)Facts:Founder

InvestmentFounder Shares1,000,000VC

Investment$3,000,000VC's required return50%Projected Net

Income in Yr. 53,000,000Years to discount4Comp Stats: Net

Income$2,000,000 $$ Raised$18,000,000Step 1:Calculate

Valuation metric from the Z Corp. Initial Public

OfferingPrice/Earnings (PE ratio) = 9.00Step 2:Calculate Baz

Corp’s value at exit$27,000,000Step 3: PV of Step

2$5,333,333Step 4: Ownership % based on VC's

Investment56.250%Step 5: Calculate New shares

needed:1,285,714n = (Existing shares x Acquired %) / (1 –

Acquired %)Step 6: Total Shares post closing2,285,714Step 7:

Price per Share$2.33Price per shareCap

TableShares%Founder1,000,00043.75%Series

A1,285,71456.25%Total2,285,714100.0%

Series A & BVC Method - Problem 2 - Series B (Slide

44)Facts:Founder InvestmentFounder Shares1,000,000Series A

VC Investment$3,000,000VC's required return50%Series A

Years to Exit4Series B VC Investment$2,000,000Series B

2. Required Return25%Series B Years to Exit2Projected Net

Income in Yr. 53,000,000Comp Stats: Net Income$2,000,000 $$

Raised$18,000,000Step 1:Calculate the required Future Value of

Series B VC’s investment using the 25% required rate of

return: 2,000,000 x (1.25)2 3,125,000.00Step 2: Calculate

Series B Required Ownership % Series B FV / Exit Valuaion

from Problem 111.5741%0.562567.8241%Step 3: Calculate

Required Shares to be issued to Series A VC to ensure that it

owns 56.25% at exit n = (Existing shares x Acquired %) / (1 –

Acquired %)2,107,914Step 4: Total Shares3,107,914Step 5:

Series A Required Ownership % based on VC's

Investment67.824%Step 6: Price per Share$1.42Cap

TableShares%Founder1,000,00032.2%Series

A2,107,91467.8%Total3,107,914100.0%

Name ;

- SECOND EXAM SPRING 2020

1. Mark Price the marketing manager for Speakers needs to find

which variable most affects the demand for a line of speakers.

He is uncertain whether the price of speakers of the advertising

expenditures drive the sale of speakers. He plans to use the

regression analysis to determine the relative impact price an

3. advertising. He used 12 years of data which is given below. The

output from his regression analysis also give:

Sales

(000)

Price Per Unit

Advertising

($000)

400

280

600

700

215

835

900

211

1100

1300

210

1400

1150

215

1200

1200

200

1300

9. 2.92

-2.37

0.04

-13.51

Advertising

0.33

0.24

1.36

0.21

-0.21

a. Interpret the output from the regression analysis given above

– is this a good regression model to forecast sales

b. Evaluate the regression model. Also, comment on the sample

size (observations)

c. Write the regression equation showing the relationship

between Sales versus Advertising and Price

d. Determine whether Price or Advertising has more impact on

the forecast of Sales

e. Predict average yearly speaker sales the price was $300 per

unit and Mark is planning to spend $900 thousand in

Advertising.

2. Assume the network and data as follows:

10. a. Construct the network diagram

b. Indicate the critical path when normal activity times are used

c. Explain the procedure you would use to crash this project if

you had a penalty cost per week above 15 weeks as well you

had indirect costs per week

3. Ace Steel Mill estimates the Demand for steel in millions of

tons per year as follows

Millions of t tons

Probability

10

10

12

25

14

30

16

20

18

15

11. a. If capacity is set at 18 Million tons what is the capacity

cushion

b. What is the probability of Idle capacity

c. What is the average utilization of the plant at 18 million ton

capacity

d. If it costs $8 million per ton of lost business and $80 million

to build a million ton of capacity how much capacity should be

built to minimize the total cost

4. Explain the reasons for

a. Carrying large levels of inventories

b. Carrying Small Levels of Inventories

5. We discussed in class how MRP (Materials Planning System)

works we examined an example of the a Table with four legs

and a leg assembly. We discussed the following charts.

Please explain how the Bill of Materials Explosion takes place

12. in these charts

6.

7. Explain the following as discussed in class

Thompson manufacturing produces industrial scales for the

13. electronics industry. Management is considering outsourcing the

shipping operation to a logistics provider experienced in the

electronics industry.

a. Thompson’s annual fixed costs of the shipping operation are

$1,650,000, which includes costs of the equipment and

infrastructure for the operation. The estimated variable cost of

shipping the scales with the in-house operation is $4.70 per ton-

mile.

b. If Thompson outsourced the operation to Carter Trucking, the

annual fixed costs of the infrastructure and management time

needed to manage the contract would be $560,000. Carter would

charge $8.50 per ton-mile.

c. Currently Thompson shipped 255,000 ton-miles this year and

his shipments in the last five years have increased at the rate of

18,000 ton-miles a year.

What would you recommend Thompson to do and why?

2

Entrepreneurial Finance

Lecture 6

14. Valuing Entrepreneurial Ventures 2

Housekeeping:

This Tuesday we have an In-class exercise where you will apply

the valuation techniques that you are currently learning. To

complete this you will need to purchase the case. I have put

together a Course Pack at Harvard Business Publishing that has

the case you will need, and two other cases for later in the

course. The cases will cost $12.75. I have also added some

suggested reading that is optional and won't be directly tested

on. These cost an additional $32.90. The link for theses

purchases was sent by email and is posted on BlackBoard.

Cash, Build, Burn & Runway and Cash Conversion Cycle

Homework - Still waiting for one more student to submit the

assignment so I can't post the answer yet. Most of you did very

well. Here are two common errors that you should fix so that

you get it right for the test. For Cash Build, Burn and Runway,

be careful with the Cash Burn from Balance Sheet. You are

looking at the change in balances from one year to the next.

Also, review the slides on whether in increase or decrease in a

balance item is a cash inflow or outflow.

For Cash Conversion Cycle, there is no such thing a negative

15. days. Use absolute values. Also, your answer is in days, not

dollars. You are trying to understand how long it takes from the

time that you first invest in Raw Materials to make your product

to the date when you receive the cash from a completed sale.

1

2

Adjusted Present Value Example

3

APV formula steps

Estimate the value of the firm in three steps:

Calculate the value of the unlevered firm

Discount equity CF’s at unlevered re

Calculate interest tax savings generated from debt (tax shield),

if any

Tax rate x Debt

Sum up steps 1 and 2 and add back starting cash

Step 1:

Calculate the value of the unlevered firm

16. Calculate free-cash flows from operations:

FCF = EBIT (1 – t) + Depreciation – CAPEX – Δ NWC

Calculate the Terminal Value (future value of all steady state

firm cash flows):

Terminal Value = FCF (1 + g) / (re – g)

where g is the steady state (stable) growth rate of the firm, and

re is the unlevered cost of equity

Discount FCF and terminal value to present time using re

4

5

APV Method Example – Crunch Co.Facts:Crunch Co. is a start-

up fitness equipment company founded by Bob “Crunch”

Borkowski. Crunch Co. received a $300,000 investment from

Golden Venture Partners (GVP). After 3 years, Crunch Co. has

finally begun to generate positive earnings and free cash

flow.GVP is now considering its exit options and asks you to

help value Crunch Co. They have provided financial projections

and other information below. Value the company using the

Adjusted Present Value Method.Unlevered Cost of

Equity14%Perpetual Growth Rate4.50%Debt (US$

000’s)$200Cost of Debt10%Tax Rate22%

17. APV Method Example – Crunch Co.

Crunch Co. Selected Financial Projections (US$ 000’s)

6YearActual 1 2 3 4 5Sales$220.0 $231.0 $242.6

$254.7 $267.4 $280.8 Cost of Goods Sold132.0 138.6 145.5

152.8 160.4 168.5 General & Administrative Expenses20.0 20.0

20.0 20.0 20.0 20.0 Depreciation15.0 15.0 16.0 17.0 18.0 19.0

EBIT53.0 57.4 61.0 64.9 69.0 73.3 Interest Expense20.0 20.0

20.0 20.0 20.0 20.0 Pre-tax Income33.0 37.4 41.0 44.9 49.0 53.3

Taxes7.3 8.2 9.0 9.9 10.8 11.7 Net Income$25.7 $29.2 $32.0

$35.0 $38.2 $41.6 Selected Balance Sheet Information:Cash &

Marketable Securities24.0 33.8 37.6 45.6 47.8 53.2 Gross

Property Plant and Equipment10.0 15.0 19.0 22.0 25.0 27.0 Net

Working Capital 6.0 7.0 9.0 8.0 9.0 10.0

Time 0

YearUnlevered Free Cash Flow Calculation: 1 2

3 4 5NOPLAT (EBIT x (1 - tax rate))44.8 47.6 50.6

53.8 57.2 + Depreciation15.0 16.0 17.0 18.0 19.0 - Capital

Expenditures5.0 4.0 3.0 3.0 2.0 - Change in New Working

Capital1.0 2.0 (1.0)1.0 1.0 Unlevered Free Cash Flow$53.8

$57.6 $65.6 $67.8 $73.2 Present Value @re of 14%47.2 44.3

44.3 40.1 38.0 Cumulative PV of Forecast Period$213.9

Terminal Value Calculation$805.0 Present Value of Terminal

18. Value418.1 Crunch Co. Unlevered Value $632.0

Crunch Co. APV – Calculate Unlevered Value

7

Step 1: Calculate Unlevered Value of Crunch Co.

YearUnlevered Free Cash Flow Calculation: 1 2

3 4 5NOPLAT (EBIT x (1 - tax rate))44.8 47.6 50.6

53.8 57.2 + Depreciation15.0 16.0 17.0 18.0 19.0 - Capital

Expenditures5.0 4.0 3.0 3.0 2.0 - Change in Net Working

Capital1.0 2.0 (1.0)1.0 1.0 Unlevered Free Cash Flow$53.8

$57.6 $65.6 $67.8 $73.2 Present Value @re of 14%47.2 44.3

44.3 40.1 38.0 Cumulative PV of Forecast Period$213.9

Terminal Value Calculation$805.0 Present Value of Terminal

Value418.1 Crunch Co. Unlevered Value $632.0

Crunch Co. APV – Calculate Unlevered Value

8

Step 1: Calculate Unlevered Value of Crunch Co.

NOPLAT =

EBIT x (1 – tax rate

$57.4 x (1 – .22) = $44.8

CAPEX =

Gross PPE Yr. 1 – Gross PPE Yr. 0

$15 – $10 = $5

19. Change in NWC =

NWC Year 2 – NWC Year 1

$9.0 – $7 = $2

Present Value =

CF4 / (1 + re)4

$67.8 / (1 + .14)4 = $40.1

Terminal Value =

CF5 x (1 + g) / (r – g)

$73.2 x (1 + .045) / (.14 - .045) = $805.0

Present Value =

TV / (1 + re)5

$805.0 / (1 + .14)5 = $418.1

Keep this slide handy for the exam.

8

Crunch Co. APV – Interest Tax Shield

9

Interest Tax Shield Formula:Tax Rate x Debt