Recommended

Recommended

More Related Content

Similar to BUS M02C – Managerial Accounting SLO Assessment project .docx

Similar to BUS M02C – Managerial Accounting SLO Assessment project .docx (20)

More from hartrobert670

More from hartrobert670 (20)

Recently uploaded

Recently uploaded (20)

BUS M02C – Managerial Accounting SLO Assessment project .docx

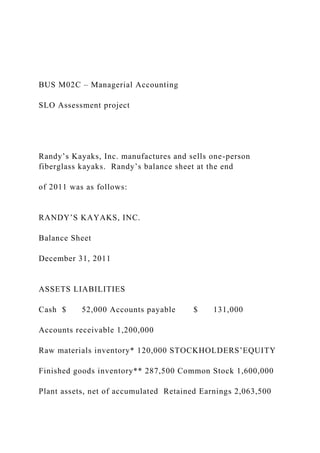

- 1. BUS M02C – Managerial Accounting SLO Assessment project Randy’s Kayaks, Inc. manufactures and sells one-person fiberglass kayaks. Randy’s balance sheet at the end of 2011 was as follows: RANDY’S KAYAKS, INC. Balance Sheet December 31, 2011 ASSETS LIABILITIES Cash $ 52,000 Accounts payable $ 131,000 Accounts receivable 1,200,000 Raw materials inventory* 120,000 STOCKHOLDERS’EQUITY Finished goods inventory** 287,500 Common Stock 1,600,000 Plant assets, net of accumulated Retained Earnings 2,063,500

- 2. Depreciation 2,135,000 Total Assets $ 3,794,500 Total Liabilities & SE $ 3,794,500 *40,000 pounds **1,000 kayaks The following additional data is available for use in preparing the budget for 2012: Cash collections (all sales are on account): Collected in the quarter of sale 40% Collected in the quarter after sale 60% (Bad debts are negligible and can be ignored) Cash disbursements for raw materials (all purchases are on account): Cash paid in the quarter of purchase 70% Cash paid in the quarter after purchase 30% Desired quarterly ending Raw materials inventory 40% of next quarter’s production needs Desired quarterly ending Finished goods inventory 10% of next quarter’s sales

- 3. Budgeted sales: 1 st quarter 2012 10,000 kayaks 2 nd quarter 2012 15,000 kayaks 3 rd quarter 2012 16,000 kayaks 4 th quarter 2012 14,000 kayaks 1 st quarter 2013 10,000 kayaks 2 nd quarter 2013 12,000 kayaks Anticipated equipment purchases: 1 st quarter 2012 $30,000

- 4. 2 nd quarter 2012 $0 3 rd quarter 2012 $0 4 th quarter 2012 $150,000 Quarterly dividends to be paid each quarter in 2012 $4,000 Expected sales price per unit $400 Standard cost data: Direct materials 10 pounds per kayak @ $3 per pound Direct labor 10 hours per kayak @ $20 per hour Variable manufacturing overhead $5 per direct labor hour Fixed manufacturing overhead (includes $9,000 depreciation) $103,125 per quarter Variable selling expenses $25 per kayak Fixed selling and administrative expenses:

- 5. Insurance $45,000 per quarter Sales salaries $30,000 per quarter Depreciation $6,000 per quarter Income tax rate 30% Estimated income tax payments planned in 2012: 1 st quarter $0 2 nd quarter $50,000 3 rd quarter $400,000 4 th quarter $500,000 Randy’s desires to have a minimum cash balance at the end of each quarter of $50,000. In order to maintain this minimum balance, Randy’s may borrow from its bank in $10,000 increments with an interest rate of 6%.

- 6. Money is borrowed at the beginning of the quarter in which a shortage is expected. Repayments of all or a portion of the principle (plus accrued interest on the amount being repaid) are made at the end of any quarter in which the cash balance exceeds the required minimum. Requirements: 1. Use the above information to prepare the following components of the master budget: a. Sales budget with a schedule of expected cash collections for each quarter and the year as a whole b. Production budget for each quarter and the year as a whole c. Direct materials purchases budget with a schedule of expected cash disbursements for materials for each quarter and the year as a whole d. Direct labor budget for each quarter and the year as a whole e. Manufacturing overhead budget with expected cash disbursements for each quarter and the year as a whole f. Ending finished goods inventory budget for the year g. Selling and administrative expense budget with expected cash disbursements for each quarter and the year as a whole h. Cash budget for each quarter and the year as a whole

- 7. i. Budgeted income statement for the year j. Budgeted balance sheet for the end of the year 2. Prepare a brief memo to management with specific comments and/or recommendations relating to the budget. Microcomputer Architecture There is a 2GHz processor with two levels of cache. L1 cache is 2KiB with a block size of 4 words. L2 cache is 4KiB with a block size of 2 words. Both L1 and L2 are direct-mapped caches. The operating system manages a page table with a 1KiB page size and a fully-associative TLB with 4 entries that are each one page in size. New entries to the page table should increment the highest used physical page. The access time for L1 and L2 are 2 clock cycles and 13 clock cycles, respectively. The TLB requires 31 clock cycles to access and the page table takes 48 clock cycles to access. Physical memory (main memory) takes 200 clock cycles to access, and accessing disk will cost 100,000 clock cycles.

- 8. The initial state of the cache, page table, and TLB are as follows. All addresses are 32 bits. L1 Cache Valid Tag Index 1 8 1 1 0 4 1 9 13 0 1 3 1 0 64 1 0 86 L2 Cache Valid Tag Index 1 0 0 1 0 255 1 9 13 1 1 3 0 1 22

- 9. 1 2 189 TLB Valid Tag Physical Page Last Access 1 0 1 1 5 10 1 1 0 1 8 6 Page Table Entry Valid Physical Page or Disk 0 1 1 1 1 0 2 1 4 3 0 Disk 4 1 12

- 10. 5 1 10 6 0 Disk 7 0 Disk 8 1 6 9 1 0 10 0 Disk 11 1 5 1. Fill in the missing information from the following tables regarding the bit fields in each level of cache. L1 cache bits Bit Field Description Number of Bits Reason Byte offset bits

- 11. Word offset bits Index bits Tag bits L2 cache bits Bit Field Description Number of Bits Reason Byte offset bits Word offset bits Index bits Tag bits 2. What is the total time the system will take to access the following virtual byte addresses? Fill in the table on the next page as well as the sentence following the table.

- 12. 0, 355, 2000, 8192, 11752, 116386 Virtual Byte Address Virtual Page Page Offset TLB Tag TLB Index TLB Hit/ Miss Time for TLB (cycles) PT Hit/Miss Time for PT (cycles) Physical Page 0 -- 355 -- 2000 -- 7168 -- 11752 -- 116386 -- Physical Byte Address

- 13. Physical Word Address L1 Block Address L1 Tag L1 Index L1 Hit/ Miss Time for L1 (cycles) L2 Block Address L2 Tag L2 Index L2 Hit/ Miss Time for L2 (cycles) Total Time (cycles) The total time to access the given virtual addresses is (fill in the blanks): ____________ clock cycles, or