Recommended

Recommended

More Related Content

Similar to Professor’s Critique of DENNISWRIGHT’s submissionExcel worksh.docx

Similar to Professor’s Critique of DENNISWRIGHT’s submissionExcel worksh.docx (20)

More from briancrawford30935

More from briancrawford30935 (20)

Recently uploaded

Recently uploaded (20)

Professor’s Critique of DENNISWRIGHT’s submissionExcel worksh.docx

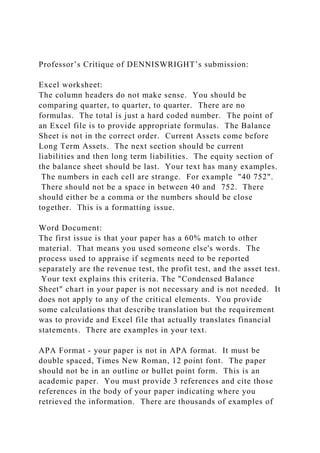

- 1. Professor’s Critique of DENNISWRIGHT’s submission: Excel worksheet: The column headers do not make sense. You should be comparing quarter, to quarter, to quarter. There are no formulas. The total is just a hard coded number. The point of an Excel file is to provide appropriate formulas. The Balance Sheet is not in the correct order. Current Assets come before Long Term Assets. The next section should be current liabilities and then long term liabilities. The equity section of the balance sheet should be last. Your text has many examples. The numbers in each cell are strange. For example "40 752". There should not be a space in between 40 and 752. There should either be a comma or the numbers should be close together. This is a formatting issue. Word Document: The first issue is that your paper has a 60% match to other material. That means you used someone else's words. The process used to appraise if segments need to be reported separately are the revenue test, the profit test, and the asset test. Your text explains this criteria. The "Condensed Balance Sheet" chart in your paper is not necessary and is not needed. It does not apply to any of the critical elements. You provide some calculations that describe translation but the requirement was to provide and Excel file that actually translates financial statements. There are examples in your text. APA Format - your paper is not in APA format. It must be double spaced, Times New Roman, 12 point font. The paper should not be in an outline or bullet point form. This is an academic paper. You must provide 3 references and cite those references in the body of your paper indicating where you retrieved the information. There are thousands of examples of

- 2. APA papers on the internet. Sheet1EARTHWAY ADInterim Financial Statements30 June 2016Interim Balance SheetNotes to the Interim Financial StatementsNotes30 June31 December30 June201620152015$’000$’000$’000AssetsNon-current assetsProperty, plant and equipment 28 96421 83819 101Investment property 1 1301 1701 214Investments in subsidiaries 388 693340 387185 909Investments in associates 45 67018 76718 052Intangible assets123247371Long-term financial assets 1 24519 51017 699Long-term receivables due from related parties 81 05272 465-Long-term receivables 13 49523 16812 674 560 372497 552255 020Current assetsInventories143155296Short-term receivables due from related parties 34 47622 74163 472Short-term financial assets 5 39411 7422 517Advance payments for purchase of financial instruments - 61 289-Loans granted 113 06276 1915 107Trade receivables 3 4604 1792 824Other receivables 24 02811 28316 104Cash and cash equivalents 85 65392 84530 455 266 216280 425120 775Total assets 826 588777 977375 795EquityShare capital150 000150 000130 000Share premium232 343232 34332 925Other reserves6 7356 8347 119Retained earnings148 70866 22565 945Net profit for the period43 34682 48341 307Total equity581 132537 885277 296LiabilitiesNon-current liabilitiesLong-term trade liabilities-8642 470Long-term bank loans--1 788Finance lease liabilities2 6993 7455 772Long-term payables due to related parties177 295178 59727 235Deferred tax liabilities--539179 994183 20637 804Current liabilitiesShort-term payables due to related parties40 75212 40535 548Short-term bank loans3 63624 6809 137Loans received4 3324 962-Trade payables7 8468 3673 102Finance lease liabilities1 4881 6202 477Tax liabilities1 9485676Payables to employees and social security

- 3. institutions6158554Other liabilities5 3994 2279 87165 46256 88660 695Total liabilities245 456240 09298 499Total equity and liabilities826 588777 977375 795Executive director:__________________Date: ____________________General InformationEARTHWAY AD was registered as a joint-stock company at NewYork city court on 28 January 1999.The main activity of the Company includes as follows:Acquisition, management and sale of shares in Bulgarian and foreign companies;Financing of companies in which interest is held;Banking services, finance, insurance and life insurance, pension and health insurance; &A Page &P 1 Running Head: Milestone Two 4 Running Head: Milestone Two 1 Milestone Two Name Professor ACC November 28, 2016

- 4. B. Interim financial reports are prescribed in AS 25 and its objective is to describe the minimal requirements of interim financial reports and the principles of measurement and recognition. Interim financial reports must include the notes to accounting policies used, cash flow statements, profit and loss statement and the company's balance sheet as well as an additional explanatory materials of interest. In the notes to interim reports, the following information should be included as long as it has not been disclosed anywhere else: · material events subsequent to the end interim period · explanatory statements about the seasonality of interim operations · Issuances, repayments, buybacks and restructuring of equity, debt and any potential equity shares. · The nature and the amount of items that affect assets and the liabilities of the company as well as the net income and cash flow statements. · In addition, it should disclose the material changes in the contingent liabilities since the last time balance sheet date. Interim financial statements stipulated guidance under GAAP and IFRS · The interim report is required to be fulfilled by an officer of the company.

- 5. · The report committee should consist of up to six members, directors of the company's · Financial statements should be in compliance with the IFRS if the complete set of financial statements is published in the interim report · If the financial statements were consolidated, the statements should be Group financial statements. · Interim report must have the most recent annual financial statements C. Hypothetical financial statement Shown on the excel D) Differences between the IFRS and the GAAP GAAP GAAP views interim periods as integral part of the annual report period. The financial costs occurred in one accounting interim period and affect other accounting periods can be allocated between the affected accounting periods. GAAP requires that accounting entities should use the world wide tax rates when estimating taxes in preparing these reports. IFRS The guidance related interim reports under IFRS views each interim period as discrete in reporting with the exception of income taxes. In IFRS, if there are costs shared by more than one period, the regulations require that such costs should be defined at the end of the reporting period and deferred the subsequent reporting periods. It’s a cost, it would meet the basic definition of an asset while if liabilities, they should be able to represent current liability at the end of each reporting period. The regulations requires that tax rates used should be unique for each jurisdiction E) 1. Companies identifies the segments which can be reported after examining their structure and the systems of reporting which they employ. Segmentation is usually based on the

- 6. products and services offered by the company or the location of its assets. The reports prepared for the company's CEO and CFO should be used as a basis for determining how segmentation would be carried out. 2. Interim financial reports are supposed to reflect transparency in presenting the financial position of the company. Stakeholders must access complete financial information in order to be able to evaluate the financial position of the company and also monitor the performance of the company's management. The main objective of standards of GAAP and IFRS is to ensure that companies and other entities which are accountable to the public are able to present the fair position of the company's financial position for investors and other stakeholders to make informed decisions. In this regard, the regulations stipulates that organizations with different segments must present the financial statements for each segment separate. This is because the performance of each different business is affected by unique factors. Hence, such financial reports which segregate each segment present fair financial information can enable the users of financial reports to predict the future performance of the company accurately. 3. Corporates which have diversified interests must provide the financial information for each segment so as to enable the investors to make accurate and sound investments decisions based on the financial performance of the company as a whole. 1. Foreign exchange rates effects Basically, the performance of the company is affected in the following ways: · Exports: When a firm exports products and the sales proceeds are to be realized at a specified date in the future, increase in rates may increase the amount of proceeds while decrease would lead to lower than agreed proceeds being received. Company's tend to lock their loses through financial markets by entering into futures contracts · Exports: The prices of imports is affected significantly where

- 7. the company's base currency is not to be used in transactions. If its value of base currency decreases compared to the value of currency which would be used in making settlement, the company gains while strengthening of the base currency against the foreign currency leads to higher payments that agreed being made by the company. · In addition, expenses incurred by the company which have to be settled in foreign currencies are affected in a similar manner. · Investment risk: This may occur as a result of errors made in forecasting the future technological changes and costs related to foreign investments · Default /Credit: The risk inherent to the company which may occur as a result of decreased credit ratings of entities in which the firm holds portfolio or to investors who hold portfolio in foreign entities which suffer lower credit ratings and are in high risk of default · Financial risk: This is risk inherent due to uncertainties associated with foreign currency exchange rates, liquidity positions, credit ratings and interest rates which have an impact on the financial performance of the firm. · Interest rate risk: This is the risk inherent to a company as a result of changes in interest rates. Increase in interest rates would affected the performance negatively while decrease in interest rates would have positive impact on the performance of the company. · Political risk: This is risk inherent to a company which may occur as a result of political turbulence in foreign owned segments. For instance, government revolutions and coup d’état. · Foreign exchange rates risk: This is risk of losses due to adverse movements in foreign exchange rates for all financial instruments held in foreign currencies. · Market risk: It refers to the daily fluctuations of the stock market prices which are influenced by many factors pointing to the performance of the firm as perceived by investors. 2. Translation methods · Currency rate method

- 8. This method is used when the local currency is being translated is the same as the foreign currency · Temporal rate method It is used when there the local currency is different from the foreign currency. 3. Hypothetical example: Suppose that Walmart has a subsidiary in South Africa. Walmart is an American chain stores firm and its subsidiary store in South Africa reported the following balance sheet numbers: Numbers are reported in Local currency (South African Rand) Current assets 500,000. Fixed assets = 3100000 Total assets = 3600000 Current liabilities = 200000 Long term debt = 1400000 Equity = 2000000 Total liability and equity = 3600000 Here, the USD/Rand is used to translate the items in the balance sheet to USD using the current exchange rate which is 1 South Africa rand = $0.07. However, the equity items are translated using the rates which are applicable during the time the equity was issued. Assuming at the issuance date the exchange rates were 1South African Rand = $0.06, the cumulative balances will be shown as the cumulative translation adjustment. Now, the balance sheet items in USD will be shown as: So, current assets in USD will be 500,000*0.07 = $35,000. Fixed assets = 3,100,000*0.07 = $217,000. Total assets = $252,000. Current liability 200,000*0.07 = $14,000. Long term debt = 1,400,000*0.07 = $98,000. Equity 2000, 000*0.06 = $120,000. Total liability and equity = $232,000 Difference = 252,000 - 232,000 = $20,000 (assets – liabilities) is the CTA and it’s shown as

- 9. such in the balance sheet Temporal rate of translation When using this method, the exchange rates at the time of acquisition of assets and liabilities are used. The exchange rate used is the current exchange rates for the current assets, while for fixed assets, the historical exchange rates are used. The exchange rate at the time when equity was issued is used. References Doran, D. (2012). Financial reporting standards (1st ed.). [New York, N.Y.] (222 East 46th Street, New York, NY 10017): Business Expert Press. FASB/IASB Joint Transition Resource Group for Revenue Recognition. (2016). Fasb.org. Retrieved 2 December 2016, from http://www.fasb.org/jsp/FASB/Page/LandingPage&cid=1176164 065747 IAS 25 Interim Financial Reporting. (2016). Iasplus.com. Retrieved 2 December 2016, from http://www.iasplus.com/en/standards/ias/ias34 IFRS and US GAAP: similarities and differences — 2016 edition. (2016). PwC. Retrieved 2 December 2016, from

- 10. http://www.pwc.com/us/en/cfodirect/publications/accounting- guides/ifrs-and-us-gaap-similarities-and-differences.html Saudagaran, S. (2001). International accounting (1st ed.). Cincinnati, Ohio: South-Western College Pub. . Prompt: In Milestone Two, you will submit a report as well as the necessary spreadsheets for Section II (Parts B–F) of the final project. You will discuss interim reporting requirements under generally accepted accounting principles (GAAP) and international financial reporting standards (IFRS), as well as provide an example financial statement illustrating what the interim report should entail. You will also discuss reporting requirements for business segments and discuss transparency in financial reporting. Lastly, you will consider the company’s potential international business deals, such as the impact of foreign exchange rates and the methods for translating financial statements. You will also create a hypothetical example demonstrating the translation process, using the two methods, to submit with your paper. Specifically, the following critical elements must be addressed: II. Corporation: The company is also considering structuring its business as a corporation, but is aware that there are a lot of complex issues to consider when accounting for an incorporated entity. The company is concerned about the following key areas: B. What interim reporting requirements would the company have as a corporation? Describe the guidance related to interim financial statements under GAAP and IFRS. C. Generate a hypothetical financial statement illustrating what

- 11. that interim reporting entails. Ensure all information is entered accurately. D. Determine if the interim reporting requirements are the same under GAAP and IFRS. Provide an example to support your response. E. The company also heard that they may have to report some of their business segments separately if they opt to incorporate. 1. Appraise one of the processes used to identify which segments would have to be reported separately. Provide examples to support your response. 2. How is this process effective in supporting transparency in financial reporting? Defend your response. 3. Provide suggestions to improve this process in an effort to sustain transparency. Defend your rationale. F. When incorporating, it is important to consider whether or not the company’s business deals internationally. 1. Summarize the impact of foreign exchange rates on the company’s financial statements. What risks do foreign exchange rates pose? 2. What are the two methods used to translate financial statements and how does the functional currency play a role in determining which method is used? 3. Compose a hypothetical example to demonstrate the translation process using thetwo methods. Ensure all information is entered accurately. Guidelines for Submission: Your report must be submitted as a 2- to 3-page Microsoft Word document with double spacing, 12- point Times New Roman font, one-inch margins, and at least two sources (in addition to your textbook) cited in APA format. Your accompanying spreadsheets must be submitted as Microsoft Excel files. Critical Elements

- 12. Proficient (100%) Needs Improvement (75%) Not Evident (0%) Value Corporation: Interim Reporting Describes the interim reporting requirements the company would have as a corporation and the guidance related to interim financial statements under GAAP and IFRS Describes the interim reporting requirements the company would have as a corporation but does not describe the guidance related to interim financial statements under GAAP and IFRS, or description is cursory or has inaccuracies Does not describe the interim reporting requirements 10 Corporation: Financial Statement Generates a hypothetical financial statement illustrating what the interim reporting entails and ensures all information is entered accurately Generates a hypothetical financial statement illustrating what the interim reporting entails, but there are inaccuracies Does not generate a hypothetical financial statement 10 Corporation: GAAP and IFRS Determines if the interim reporting requirements are the same under GAAP and IFRS and provides an example to support response Determines if the interim reporting requirements are the same under GAAP and IFRS but example provided does not support response, or does not provide an example Does not determine if the interim reporting requirements are the same under GAAP and IFRS 10 Corporation: Segments Appraises one of the processes used to identify which segments

- 13. would have to be reported separately and provides examples to support response Appraises one of the processes used to identify which segments would have to be reported separately but does not provide examples to support response, or appraisal is cursory or has inaccuracies Does not appraise one of the processes 10 Corporation: Transparency Evaluates the effectiveness of the process in supporting transparency in financial reporting and defends response Evaluates the effectiveness of the process in supporting transparency in financial reporting but does not defend response, or defense is weak or illogical Does not evaluate the effectiveness of the process in supporting transparency in financial reporting 10 Corporation: Suggestions to Improve Provides suggestions to improve the process and defends rationale Provides suggestions to improve the process but does not defend rationale, or defense is weak or illogical Does not provide suggestions to improve the process 10 Corporation: Impact Summarizes the impact of foreign exchange rates on the financial statements and determines the risks they pose Summarizes the impact of foreign exchange rates on the financial statements but does not determine the risks they pose, or summary is cursory or has inaccuracies Does not summarize the impact of foreign exchange rates on the financial statements 10 Corporation: Two Methods

- 14. Describes the two methods used to translate financial statements and how the functional currency plays a role in determining which is used Describes the two methods used to translate financial statements but does not describe how the functional currency plays a role in determining which is used, or description is cursory or has inaccuracies Does not describe the two methods of translation 10 Corporation: Translation Process Composes a hypothetical example demonstrating the translation process using the two methods and ensures all information is entered accurately Composes a hypothetical example demonstrating the translation process using the two methods but example contains inaccuracies Does not compose a hypothetical example 10 Articulation of Response Submission has no major errors related to citations, grammar, spelling, syntax, or organization Submission has major errors related to citations, grammar, spelling, syntax, or organization that negatively impact readability and articulation of main ideas Submission has critical errors related to citations, grammar, spelling, syntax, or organization that prevent understanding of ideas 10 Total 100%